Download

1 / 13

130 likes | 472 Views

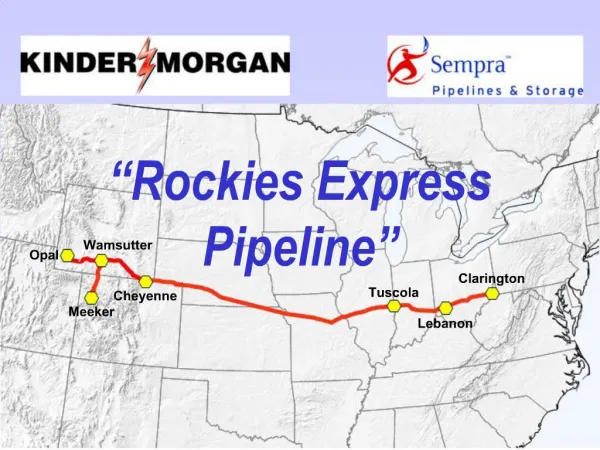

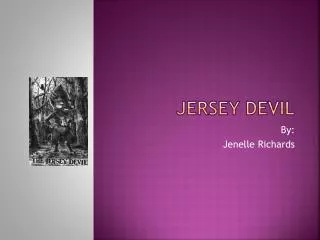

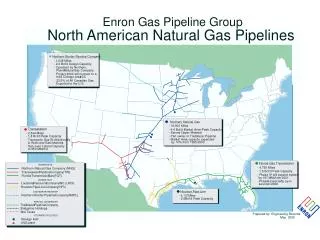

Transwestern Pipeline Company Status of San Juan Expansion & Sun Devil Lateral February 2004 www.crosscountryenergy.com. Nevada. Colorado. Utah. ROCKIES. Supply Basins. Rate Areas. California. Ignacio. SAN JUAN. Blanco Hub. San Juan. Area. ANADARKO. Needles. Phoenix. Topock.

E N D

Transwestern Pipeline CompanyStatus of San Juan Expansion&Sun Devil LateralFebruary 2004www.crosscountryenergy.com

Nevada Colorado Utah ROCKIES Supply Basins Rate Areas California Ignacio SAN JUAN Blanco Hub San Juan Area ANADARKO Needles • Phoenix Topock Thoreau Oklahoma East of Station Panhandle North West of Thoreau Thoreau 9 Area Area Arizona New Mexico PERMIAN Texas West Texas North Available Capacity to Serve AZ • Mainline West Capacity of 1,210 MMcf/d. 700 MMcf/day of Mainline West capacity and 350 MMcf/day of San Juan capacity available, subject to ROFR in 2005-2006 • Current Expansions: TW preparing FERC certificate application to expand San Juan capacity by 375 MMcf/day with a mid-2005 in-service date. • Proposed Expansion: TW is planning a 170 mile lateral from its mainline near Flagstaff to the Phoenix market, capable of flowing 500+ MMcf/day without compression and up to 1.2 Bcf/d with compression.

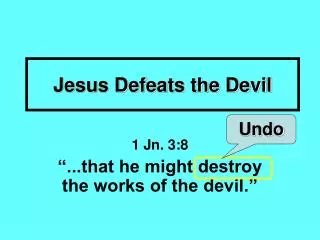

Transwestern Supply Basin Analysis 120 Permian Reserves San Juan Reserves Rocky Mountain Reserves Mid-Continent Reserves 100 80 Trillion Cubic Feet 60 40 20 0 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 Source: Lippman Consulting Gas Supply Access • Since 1998, total reserves in the four major supply basins served by TW have risen dramatically.

25 25x San Juan Basin Reserves San Juan Basin Year-End Reserves Reserve Life Index 20 20x 15 15x Year End Reserves TCF Reserve Life Index 10 10x 5 5x 0 0x 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 Source: Lippman Consulting San Juan Basin - Reliable Resource Base • San Juan basin is one of the largest natural gas basins in the United States. • San Juan total reserves and reserve life (15 years) continue to increase. • Most active producers include: Devon, BP, Burlington, ConocoPhillips, & XTO

$6.50 Monthly Gas Index Prices Since the Kern River Expansion San Juan Permian Rockies Malin Henry Hub $6.00 $5.50 Dollar per MMbtu $5.00 $4.50 $4.00 $3.50 May-03 Jun-03 Jul-03 Aug-03 Sep-03 Oct-03 Nov-03 Dec-03 San Juan Basin – Economically Attractive • San Juan gas has been the most economical source of major natural gas supplies for Southwest markets. • The San Juan gas price has remained more competitive vs. Permian & Rockies despite the Kern River expansion. • Approximately 61% of gas shipped by TW in 2003 was from the San Juan Basin. “Rockies" = Inside FERC Northwest Pipeline Rocky Mountain First of the Month Index (FOM Index), "San Juan" = Inside FERC San Juan FOM Index, "Permian" = Inside FERC Permian FOM Index, "Henry Hub" = Settlement Price on Last Day of trading for that month's NYMEX futures contract, "Malin" = Natural Gas Intelligence Malin FOM Index.

5,000 Total Regional Export Capacity Actual Export Export Capacity 4,500 4,000 3,500 3,000 MMcf per day 2,500 2,000 1,500 TRANSWESTERN SAN JUAN EXPORTS 1,000 500 0 Jul-01 Jul-02 Jul-03 Apr-01 Apr-02 Apr-03 Oct-01 Oct-02 Oct-03 Jun-01 Jan-02 Jun-02 Jan-03 Jun-03 Aug-01 Feb-02 Aug-02 Feb-03 Aug-03 Jan-01 Nov-01 Nov-02 Mar-01 Sep-01 Dec-01 Mar-02 Sep-02 Dec-02 Mar-03 Sep-03 Feb-01 May-02 May-03 May-01 San Juan Basin - High Utilization • All pipeline capacity for the San Juan Basin is fully contracted. • TW’s San Juan lateral is 100% utilized. Source: Lippman Consulting

MMCF/D 4,500 Capacity = 3,960 MMcf/d Capacity = 4,050 MMcf/d 4,000 3,500 3,000 2,500 2,000 1,500 1,000 500 0 2000 2001 2002 2003 2004 2005 2006 2007 Impact of Rockies Imports + San Juan Production Growth on Export Capacity Assumptions: Rockies imports, plus Bondad expansion, plus 1% San Juan production increase Source: Lippman Consulting

TW San Juan Expansion is the Best Way to Relieve the Constraint at Blanco • Existing infrastructure allows lower scale expansion (375 MMcf/d). • Least cost expansion alternative. • Can easily be scaled up to handle more volumes in the future by adding HP. • Low execution risk: • Experienced project manager. • Certificate is ready for filing at FERC. • Tentative Navajo ROW arrangements. • Market flexibility – East and West markets.

Proposed San Juan Expansion Bloomfield CS 15,000 Hp Add 72 miles Of 36” loop Bisti CS 1,500 Hp Add

Existing TW system Sun Devil Lateral San Juan Expansion El Paso Natural Gas Sun Devil Lateral San Juan Ignacio Blanco Anadarko Thoreau California TW Sun Devil Lateral - 500+ MMcf/d - 170 miles of 36” line, no compression - Deliveries to industrials, power generators, LDC’s and El Paso south system Phoenix Permian

Comparative Total Delivered Gas Cost 1) 1) Gas Costs based on 1/28/2004 quotes from trader/major customer.

TW Sun Devil Lateral is the Best Wayto Achieve Gas-on-Gas Competition for Phoenix • Lowest Capital cost requirements • $250mm vs $750mm for Kinder-Morgan • 170 miles vs 455 miles • Lower project cost = lower execution risk = lower cost to AZ ratepayers • Leveraging existing infrastructure allows smaller scale expansion to get started (500 MMcf/d). • No compression initially required. • Able to utilize existing unsubscribed mainline capacity. • TW’s Sun Devil Lateral provides to Phoenix: • Experienced, safe, reliable pipeline alternative • Competitive pricing • Access to multiple gas supply sources • Promotes gas-on-gas competition

ACC Action Items • Support the efforts of your customer base to access lower cost gas supplies • Arizona electric utilities • Arizona gas utilities • Large industrial users • Merchant power generation model is dead • TECO / Gila Bend • Promote development of utility infrastructure corridors using existing highway, railroad, and power line ROW • Minimizes environmental damage • Minimizes private landowner involvement • Promote and support ROW Quick-take legislation • Iowa • Utility establishes eminent domain condemnation rights via court petition, posts bond • Judge appoints 3-person independent commission to hear case • Right-of-way costs established and landowner compensated within 30 days • Provides surety of construction timeline and avoids litigation delays