Download

1 / 28

280 likes | 297 Views

This latest issue on Transactions Advisory by EY India focuses on the main drivers for M&A in 2018 and what to expect in 2019.The report also sheds light on topics like fast changing E-commerce and consumer internet. Download pdf now to read on other topics as well in detail. Visit website to know more about M&A Consulting Services by EY India.

E N D

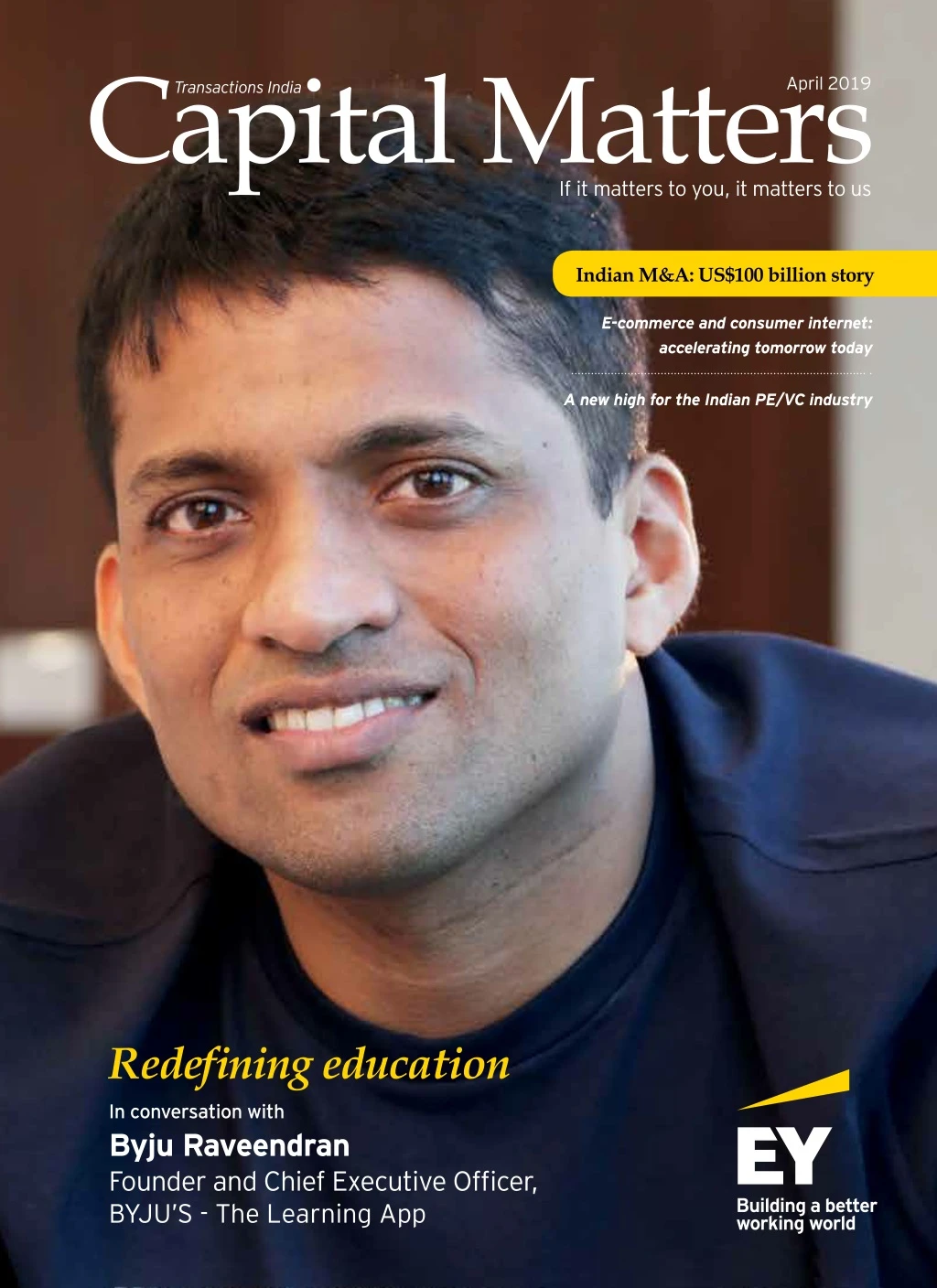

Capital Matters April 2019 Transactions India If it matters to you, it matters to us Indian M&A: US$100 billion story E-commerce and consumer internet: accelerating tomorrow today A new high for the Indian PE/VC industry Redefining education In conversation with Byju Raveendran Founder and Chief Executive Officer, BYJU’S - The Learning App

In this issue Write to us with feedback/suggestions and contributions at transactions.ey@in.ey.com Editorial Himanshu Goyal Pooja Bhalla Mathur Mansi Gupta Ashish George Kuttickal Pranjal Bhatnagar Dhriti Gandhi Inbound and domestic M&A drive India’s US$100 billion story Page 04 Highlighting the key drivers for M&A in 2018 and what to watch out for in 2019 Leading the way to redefine the traditional education sector Page 12 In conversation with Byju Raveendran, Founder and Chief Executive Officer, Byju’s - The Learning App Page E-commerce and consumer internet: accelerating tomorow today 18 Diving deep in the e-commerce and consumer internet sector and analyzing the key segments Page A new high for the Indian PE/VC industry in 2018 22 Understanding what drove the headline numbers for PE/VC Page What is driving the continued interest in Indian consumer companies? 26 Highlighting the growth of the sector and why global companies prefer the brownfield route in India

W with a view to share insights on a broad range of subjects which are pivotal to driving the capital agenda of corporate organizations and it features themes which are very pertinent in today’s context and will assist in providing a wider perspective to business and industry leaders. Foreword e are delighted to share the second edition of Capital Matters, the magazine from the EY transactions team in India. The magazine has been developed In this edition, we feature an exclusive discussion with Byju Raveendran, Founder and CEO, Byju’s. As part of the conversation, Bjyu shares his views and insights on how they are trying to transform the traditional educational sector in India, his plans to expand internationally and his vision for the next few years. This edition of the magazine revolves around the India growth story and features annual round-ups on Indian M&A, where the M&A deal value touched the aspirational US$100 billion for the first time and the record high achieved in the PE sector. The magazine also features articles by our colleagues, which talk about the drivers of inbound M&A deals highlighting the role of family- owned businesses, the ever-growing unicorn club in the e-commerce and the consumer internet sector and the heightened level of interest in Indian consumer companies by global majors. The blockbuster year for M&A and PE in 2018 was driven by a combination of several factors, including an unprecedented number of mega deals. Some of these large deals were concentrated in the consumer and e-commerce sectors, including the US$16 billion Flipkart-Walmart deal and US$7 billion in PE investments in the consumer internet sector. The sector has seen continued interest and activity lately, driven by stimuli like increased consumer demand, higher disposal incomes and internet penetration among others. I hope you enjoy this issue of the magazine and welcome your feedback. Should you have any questions or wish to discuss any of the topics raised in the magazine, please do contact me at amit.khandelwal@in.ey.com. Amit Khandelwal Managing Partner, Transaction Advisory Services, EY

April 2019 Inbound and domestic M&A drive India’s US$100 billion story F cost competitive manufacturing and a consistently high GDP growth, have now made it imperative for every major global MNC to have a substantial India presence. Thus, despite global headwinds such as trade tensions, tepid growth, currency and commodity price volatility, inbound M&A was more than US$70 billion cumulatively during the period 2015-2018, more than 50% higher On the sector front, consumer products leads the charts over the last four years in terms of inbound deal value, owing to the Walmart- Flipkart deal worth US$16 billion. In addition to traditional sectors that have witnessed some big-ticket inbound deal activity (such as manufacturing, metals and mining), the constantly evolving technological ecosystem and increasing smartphone adoption has fostered multiple homegrown enterprise technology and consumer internet companies. These start-ups have proved their mettle against global giants and have attracted high foreign investor interest, thus providing a new dimension to the India story. than the 2011-14 period (approx. US$47 billion). In 2018 alone, inbound M&A touched US$37 billion, a five-fold increase from US$6.5 billion in calendar 2017. ueled by factors like robust domestic demand, a young population (half of the country is <25 years of age), skilled labor force, stable government, well-established The government continues to push the reform agenda and this has also played an integral part with decisive liberalization, opening key sectors such as defence, construction, civil aviation, pharmaceutical and media to FDI and bringing clarity in important sectors like retail and infrastructure. All these factors have enabled India to move ahead of China for the first time in 20 years in inbound M&A in 2018. Ajay Arora Partner and National Leader, Investment Banking Advisory, Transaction Advisory Services, EY Himanshu Goyal Associate Partner, Investment Banking Advisory, Transaction Advisory Services, EY 4 Capital Matters

Issue 2 Indian M&A - US$100 billion: key highlights 2018 was a milestone year for M&A activity in India, setting new records by reaching the US$100 billion mark for the first time ever. While the quantum of deals was more than 10% higher than that of 2017, the total disclosed deal value more than doubled from US$46.8 billion in 2017 to US$99.8 billion in 2018. Indian M&A activity snapshot 99.8 Deal value US$ billion 49.7 46.8 Grand total Domestic 37.9 36.5 6.5 13.5 Inbound Outbound 2.3 2017 2018 Deal count 1125 1022 Grand total 726 Domestic 682 252 Inbound 203 147 137 Outbound 2017 2018 EY analysis of various transaction databases; excludes bank recapitalizations, share repurchases and buyouts by PE funds Capital Matters 5

April 2019 Key deal trends of 2018 2018 broke all records in terms of M&A deal value. The steep rise in value can be attributed to several factors including an unprecedented appetite for mega deals (US$1 billion and above). There were 19 M&A deals that breached the US$1 billion mark in 2018, Of which, five were in the US$5 billion plus range, highest ever in this segment in the last five years. This points to a paradigm shift towards large deal-making in the Indian M&A market. Top five M&A deals of 2018 Geography Target Target Country India Acquirer Acquirer Country United States Value (US$m) 16,000 Target Sector Inbound Flipkart Group Essar Steel India Ltd Walmart Inc. Retail and consumer products Metals and mining Luxembourg, Japan 6,829 Inbound* India ArcelorMittal and Nippon Steel and Sumitomo Metal Corp Oil & Natural Gas Corp Ltd India India 5,784 Oil and gas Domestic Hindustan Petroleum Corp Ltd Indus Towers Ltd Bhushan Steel Ltd Domestic India Bharti Infratel Ltd India 5,359 Telecommunications Domestic India Tata Steel Ltd India 5,216 Metals and mining * Announced to exit, primarily driven by succession issues as well the opportunity to encash and secure family wealth. Another trend seen in the year that drove deal value as mentioned earlier in the article, was the resurgence in inbound deals. It bounced back very strongly compared to 2017, more than doubled in deal value even if the Flipkart- Walmart deal of US$16 billion was excluded. This implies continued high levels of confidence and interest from global firms in the India story. Macroeconomic factors including a sustained GDP growth, range-bound inflation and interest rates, and increased consumer demand, have given a positive push to deal activity. This was further accentuated by the Indian promoters’ willingness to explore the potential While consolidation across sectors, anchored on portfolio optimization and increased focus on core businesses, remained a prominent theme in the domestic arena, several big-ticket deals stemmed from the resolution of the Insolvency and Bankruptcy Code (IBC) referred cases. It was a milestone year for the regulatory reform, especially in the steel sector and provided a fillip to the deal value. Some of the key deals included Bhushan Steel’s acquisition by Tata Steel (US$5.2 billion) and Binani Cement’s acquisition by UltraTech Cement (US$1.1 billion). Sector-wise M&A deal value (US$ million) 22,745 17,436 This year also saw an increased level of buy-out deals by tier-1 PE funds. Some examples include Blackstone buying majority stake in Comstar Automotive Technologies as well as Sona BLW and Advent’s acquisition of Manjushree Technopack. This trend has acted as a catalyst for M&A deals in the year and is expected to drive more activity in the future, thereby reinforcing the high level of confidence in the Indian market. 8,595 7,065 6,823 4,799 4,721 4,319 3,904 3,849 3,038 2,961 2,486 2,354 1,904 1,682 1,102 Retail and consumer products Metals and mining FS Oil and gas Telecommun- ications Technology Chemicals Power Diversified industrial products Cement and building products Media and entertainment Pharmaceuticals Real estate Services Healthcare Automotives Others 6 Capital Matters

Issue 2 Deal drivers for 2019 Looking forward to another good year 2019 deal activity is likely to be driven by domestic consolidation and inbound interest pending the much-awaited election results in May. There will be an interesting mix of factors that will unfold before us where some are bound to give an upswing to M&A while the others might make companies tread cautiously. such as availability of liquidity which continues to remain a scarce commodity given the situation in the banking sector and capital market fund-raising options are also expected to stay limited. Hence, companies would be looking at alternative sources of capital or divestment/carve-out of non-core assets to generate additional capital for growth and expansion. Consolidation, anchored on portfolio optimization and increased focus on core businesses 1 Corporate restructuring to deleverage the balance sheets as well as distressed asset resolution under and outside IBC will continue At a macro level, the outlook is expected to remain positive. Latest estimates on GDP growth rate indicate a 7% plus growth. The sharp jump in India’s Ease-of-Doing- Business ranking from 134 to 77 over four years, coupled with strong Purchasing Managers Index readings, for both manufacturing and services sectors, and low inflation indicate a healthy business environment. On the regulatory front, the successful implementation and increasing clarity around IBC is likely to drive more distressed assets resolutions. 2 On the cross-border front, while we expect inbound deals to have another strong year, global markets are bound to have their impact on the deal activity. India’s increasing cooperation with countries like Japan and Russia are welcome steps in strengthening the deal markets. However, there could be some slowdown in deal closures given the rising trade tensions between the US and China, the Brexit situation and volatility in crude oil prices. Inbound deals expected to increase basis stable macro- economic factors and openness of Indian promotors to deal-making 3 Sector-convergence to drive disruptive deals in sectors like retail and consumer products, technology, financial services and M&E While more clarity is expected post elections, some factors may continue to give a cause of concern 4 Reforms such as GST and IBC to continue to spur growth, coupled with better monitoring from Competition Commission of India India has moved from #134 to #77 in World Bank’s Ease-of-Doing- Business ranking index GDP growth rate expected to be in ~7% + range Easing of FDI limits 1 2 3 4 Positive factors Factors impacting deal activity Factors to watch out for 1 2 3 Liquidity concerns in the market Upcoming general elections Volatility and slowdown of global markets and political uncertainty Capital Matters 7

April 2019 Promising sectors for 2019 The overarching themes around consolidation, deleveraging, distressed assets resolution and sector convergence, continue to be the driving factors for deal-making across sectors. However, the following sectors are likely to witness heightened activity. Technology Financial services Geographical expansion in e-commerce: Select players will expand their geographical footprints to EMEA, APAC, ANZ regions in order to increase addressable market while deriving cost benefits of offshore servicing and development centres. Bridging gaps in digital capabilities around machine learning, AI and Blockchain, to drive deals. Likely to continue to witness intense deal activity across various sub-sectors, despite the perceived liquidity crisis plaguing the NBFC sector. Indian consumer technology market has become a battleground for global players with a series of transactions in the segment. Infrastructure Themes continue to be PE fund raises in the NBFC and the fintech spaces, and consolidation and buy-out transactions in the insurance space. M&A will be led by acquirers looking to aggregate the yield- generating assets. However, the deal drivers will differ among the various sub-sectors. While conventional power transactions will be largely led by distressed deals, trades in renewables space will be driven by consolidation and the requirement of sellers for expansion capital. Mobile data penetration attracting attention of bigger consumer technology players looking to expand user base in tier-2 and tier-3 cities as well as rural India. Areas like asset management and financial services distribution players are also likely to see deal activity including PE deals and pure play M&A. Retail and consumer products E-commerce Consolidation in sectors – expected in mature segments of travel, hospitality, ride sharing and by category leaders- albeit more sharply defined on capturing the value chain, enhancing customer experience (personalization, vernacular interfaces etc) and building the supporting infrastructure/ enablers of e-commerce (payments systems, logistics, order fulfilment, etc). Going forward, Invits will be a preferred firm of value creation for both and investors and sponsors. Convergence of pure play online or offline players and emergence of hybrid through either organic or inorganic route. Monetization of highways will see traction, both on private M&A side and by the government (NHAI’s toll operate transfer program). However, the active buyer universe could be limited. Food and beverage segment likely to see maximum action, driven by factors like rising per capita income, consumer expenditure, changing lifestyles and evolving food habits of the Indian consumers. There is a marked preference shift towards organic/natural products, coupled with an increasing focus on fitness and well-being which is likely to steer deal activity in this niche segment. Overall, we expect 2019 to be another good year for M&A in India, riding on the back of a strong appetite and sound fundamentals. ‘Niche’ is the new mass – The new themes around hyperlocal, B2B commerce, building online brands, social commerce, etc. are likely to witness interest from the early stage investors. 8 Capital Matters

Issue 2 What is driving inbound M&A, especially in family owned businesses? Indian family owned businesses (FOBs) are increasingly considering the idea of strategic transactions to effectively manage transition and compete better in the marketplace. Key drivers for M&A in FOBs FOBs contribute 60%-70% of India’s organized sector GDP and hence, form an integral part of the Indian economy. They have successfully navigated increased competition from global MNCs post liberalization, integrated technology with their core business models, brought in skilled professional talent at senior-most positions, raised PE funding and nimbly de-risked themselves through product and geographical diversification. This has resulted in FOBs gaining scale and becoming global at a fast pace over the last 10-15 years, which has in turn generated increasing interest both from global strategic as well as financial investors. Succession planning is an important part of FOB’s future growth strategy and this continues to be the primary driver influencing the promoter’s decision to exit the business completely or partially. In such cases, families are exploring options to sell businesses as it helps them in creating family wealth – this being the first opportunity to monetize since most of them are first generation entrepreneurs who had set-up these businesses 20-30 years ago. This may be also followed by investment in a sunrise sector which the next generation is keen to pursue. Family member disputes and splits also influence the exit decision in some cases. In India, there is a huge emotional connect with businesses and hence, traditionally Indian families were not willing to talk about a potential sale. We see that changing significantly in this decade with “selling out” no longer considered as a taboo subject. In fact, such transactions have at times set a positive precedent in closely knit business communities, further acting as a catalyst for future deals. Promoters have become mindful of how certain Indian and global event-based disruptions over the last decade have contributed to increasing volatility in the business cycles and hence, partnering with a global strategic player helps them in not just securing family wealth, but also to create incremental shareholder value in the mid to long-term. Capital Matters 9

April 2019 Emergence of PEs as strategic investors in India FOBs In the last couple of years, high leverage at the company level or at the promoter holding company level is also driving exit decisions in FOBs. As conglomerates continue to deconsolidate and focus on core businesses, we will continue to see increased inbound activity driven by such carve-out opportunities to generate cash and deleverage as well as to reorganize business portfolios. While these carve-outs help unlock value for corporates/ families, it also helps in retaining businesses for families which they can continue to own and manage in the mid to long-term. Large global PE funds and or even mid-sized domestic funds are increasingly seeking to take control of companies and this trend is expected to grow exponentially over the coming years. 2018 saw a significant increase in PE buy-outs at US$9.8 billion, which is equal to the value of buy-outs from 2015-17 combined. As Indian companies warm up to the idea of giving up control over businesses, PE funds are increasingly going in for buy-outs. Buy-out deals typically enable PE funds not only to have greater control over the operations of the company but also greater flexibility in structuring the mode and the timing of the exit. India is emerging as one of the key investment destinations for international companies due to the robust growth outlook coupled with long-term stability. CXOs of global corporations are now visiting India on a regular basis during which they are seen engaging with Indian business houses to explore joint ventures/ partnerships as well as proactively talk to families about potential buy-outs. Some of these conversations also act as inputs to decision-making in case families are still fence-sitters and have not yet taken the final exit decision. Despite the recent slowdown in the Indian economy and high degree of leverage in the corporate sector, positive sentiments because of the pro-development agenda of the government, implementation of key structural reforms over the last couple of years, high growth outlook, strong legal and jurisdiction framework and most importantly, India being one of the “largest consuming markets”, will continue to drive inbound M&A in the country. Increasing interest from both strategic and financial investors to acquire businesses in India, coupled with Indian families becoming more amenable to the idea of exits, the FOB space will continue to see heightened deal activity. Increasingly, global buyers from US, Europe and Japan are paying attention to the aspirations of Indian families and are therefore willing to explore deal structures which can help bridge valuation gaps as well as ensure involvement of the key family members in the business post closure of the transaction. Consequently, likelihood of deal closures in the FOB space has increased over the recent past. Succession planning is an important part of FOB’s future growth strategy and this continues to be the primary driver influencing the promoter’s decision to exit the business completely or partially. 10 Capital Matters

Issue 2 Inclusive growth. How do we make disruptive innovation friend, not foe? © 2019 EYLLP. All Rights Reserved. ED None. In this Transformative Age, the opportunities that emerge from disruption are ready to be seized. ey.com/betterworkingworld #BetterQuestions Capital Matters 11

April 2019 Capital MattersRedefining education K-12 education system | edtech sector | 33m downloads | 2.2m paid users | ~64 Minutes of average engagement time In conversation with Byju Raveendran Founder and Chief Executive Officer, BYJU’S - The Learning App 12

Issue 2 to raising funds.“ L being funded to expand services, operations, etc. What according to you is attracting such money in this sector? ast year was particularly interesting for the edtech sector, with companies place in technologies, processes, approaches, etc. However, adapting to the changing content at regular intervals is a challenge. In comparison, in K-12 education systems, the universe is known, the curriculum does not undergo drastic changes regularly and the content lifespan could be for the next four to five years. However, this may not be the case for professional upskilling programs. Everything we learnt was first hand – from business model tinkering, expansion, There is no denying that the underlying factor of the need to improve education delivery mechanism and introduce good quality education for students, given that India has the largest school-going population, is due to a significant demand that is present in the market. It is also important to understand, in India, the value for education is quite deep-routed. Aspirational people recognize it as a crucial component for their upliftment and parents spend a disproportionate amount of their income on education of their children. Investors are excited, given the scope of impact that the sector has, along with recognizing the need and demand for such services. Also, this is a very scalable and profitable business, if implemented well, which can be expanded rapidly with minimal investment as the major cost is to build content, once more users onboard these services the return on investment becomes quite high. Companies in the space are still scratching the surface and catering to multiple audiences with an attempt to fill in the learning gap. The segment is still in its nascent phase and it has a long journey ahead making it all the more exiting for investors. Our approach from a content creation perspective has always been to focus on engagement and effectiveness i.e., if it will be useful to students and it will be used by students. We approach subjects by first identifying concepts and curriculum that need to be covered and then identifying the best mode to teach these concepts be it though video, gamification or interactive media. The ultimate aim is to help students gain interest in subjects so that we can instill greater self-learning capabilities. There are many different audiences that need to be catered to in terms of education - B2C, B2B, reskilling/upskilling programs, etc. Apart from the K-12 segment, which is our primary focus area, upskilling and reskilling are also important education segments that need to be catered to with fast-paced changes taking There is no real playbook for success here and our approach has been based on first principles especially since this was a relatively non-existent segment a couple of years ago. Everything we learnt was first hand – from business model tinkering, expansion, to raising funds. G unicorns, what according to you sets Byju’s apart from its competitors? What is your business strategy to keep up the momentum? rowing at 100% for last three years, over 2 million annual subscribers, 4th most valued company in India, the most valued edtech company in the world, and one of the rare profitable With over 33m downloads, 2.2m paid users, and average engagement time ~64 minutes, our approach, both in terms of engagement and effectiveness, has been received positively by students, parents and education providers which is helping propel our growth. We have been fortunate to reach scale relatively quickly due to our student and learning focused approach and are increasing year-on-year which is helping us achieve progressively higher earnings enabling us to invest more organically in improving engagement and effectiveness in the product. At Byju’s we understood the challenges the ecosystem faces and one of the key challenges we could address immediately and effectively is the method with which students consume knowledge and information and are working hard towards bringing changes to the system. We began the journey with conviction and understood the potential to bring in transformational change with respect to the format for interaction and learning. The core challenges in traditional education formats face are (a) good teachers are hard to find at scale (b) ability for personalization is limited (c) format of learning (rote memorization vs. wanting to learn). Capital Matters 13

April 2019 T and the education sector is no exception. Do you think tech will bring down the cost of delivering and accessing quality education, and create an equitable education system? What other investments are you making in technology that can be integrated and leveraged in your platform? “ hand gestures, drawings, etc. It is a real game changer in the edtech space and will further help in personalizing learning experience. Integrating this on our existing platform creates a unique learning experience for students and enhances their real- time learning capabilities. ech-led innovation has disrupted every industry that we can think of today availability of internet, technology has the ability to play a great equalizer in the space. Technology is also a great enabler in integrating multiple formats of learning quickly and efficiently such as creating movies, graphics, etc. that makes for a more engaging learning experience. Our underlying consideration for investments in technology such as Artificial Intelligence (AI), Machine Learning (ML), Analytics, etc. is how to better personalize learning and help better gauge engagement levels. Deployment of these technologies will help with improve recommendations, predictions and problem solving capabilities. At Byju’s, thanks to our “brain trust” gained basis various student profiles, we have and will continue to help students with specific learning gaps, pace and needs to provide the right content in the right format. Osmo has advanced capabilities of identifying If you notice, while content consumption habits have changed across many segments (news, entertainment, etc.) in the last decade, education is one of the few fundamental segments where technology has not been able to significantly disrupt the space until recently. As recently as three years ago, if we looked at market studies on edtech space, there was very limited information available given that the relative size was small. With improved Y how do you plan to integrate this into your current offerings and what does it bring to the table? ou recently acquired Osmo to add to your portfolio of services and capabilities, of paper and pencil, which a majority of the student use and where learning happens and we were keen to bridge this gap and capture what students were doing offline to help better their education online. Osmo is a mixed-reality offering, where the integrated software will be efficiently used to capture offline learning and provide real-time course correction and guidance to help students unlock the right answer. The service has advanced capabilities of identifying hand gestures, drawings, etc. It is a real game changer in the edtech space and will further help in personalizing learning experience. Integrating this on our existing platform creates a unique learning experience for students and enhances their real-time learning capabilities. Osmo has been one of our biggest acquisitions till date. The primary reason for this acquisition was to bring in another dimension to learning in terms of integrating offline and online learning. Till this acquisition, we primarily had videos and games to engage students, however, a significant part of learning also happens offline. Traditionally, offline to online input formats have been limited to keyboards, mouse and touchscreens which still leaves a big gap in the most basic input methods 14 Capital Matters

Issue 2 Y ou have done a few acquisitions in the past including Osmo. Are there further acquisitions in the pipeline? How have your past acquisitions and international collaborations with key global brands helped? Our focus on acquisitions is similar to our approach i.e., it will it be useful to students and will it be used by students and we apply the same first principles in our acquisition evaluation process. engagement hook though content and interaction assures attention from students and is inbuilt into our core loop of learning. Our acquisitions, both big and small, have been focused on catering to our believes in providing the best learning tools for children. Our brand association internationally will bring onto our platform characters that have a deep association with children, especially who belong to the K-3 segment, which will further their association with both the brands. In the past, we have acquired companies like Tutorvista, Maths Adventure and Vidhyartha with Osmo being the most recent and significant one. The focus of our acquisitions and collaborations have been to gain content and improve engagement for students. There is a difference between being on the platform and engaging on the platform. And our focus has always been on the latter. Creating an In relation to further acquisitions, they will happen only if they complement our core offerings. Partnerships have helped create better offerings, this has helped us greatly in the past and will continue to play a key role in the future as well. W hat has motivated you to eye international expansion? What are the key factors that you are keeping in mind in narrowing down on the regions that you would want to foray in? The key challenge will be to generate segment and brand awareness in these new markets, since we are first movers in this space, we are building a strong strategy and are focused on the return on spends in these markets to enable success. We intend to focus on the quality of growth more than quantity and will pace our expansions, testing markets and aligning our business strategies accordingly. There is a need in the space to create a global brand to bring in standardization in education which can only come with scale. This is extremely difficult in the offline space as it requires significant capital infusion. We have the ability and capability to contribute to the process. Since we have a strong profitable primary market in India and a compelling product, we decided to take our offerings overseas. This is still in early stages as there are a varying number of factors to consider in each geography, and our agility in these markets will play a key role in our success. We have already built the bandwidth and are collaborating with influential online teachers for more specific markets to be able to deliver our content. While this is a more inorganic approach, it will enable us to bring our platform knowledge and content together with passionate educators to improve the quality of learning in those markets. Another important enabler to consider is the cost of private tutors that is very expensive overseas, and bringing to fore our technology will help students get the required help and build learning capabilities. Our international expansion will focus on early-grade learning ( those between three to nine years of age) and primarily in English speaking (the UK, Australia and the US)/ English as a second language (Latin America and Europe) markets. The main reasons for this approach are: (a) availability of content which can be easily be tweaked to localized specification (b) parental involvement level in this age group is fairly similar across the globe which makes it easier for an uptake on the platform. Besides this, higher grade learning offerings are also in the pipeline. Capital Matters 15

April 2019 16 “ There is a difference between being on the platform and engaging on the platform. Our focus has always been on the latter. Capital Matters

Issue 2 G approach? W oing wide versus going deep is a decision that companies tend to struggle with. With that context, what do you believe is the right hat initiatives should the government take in order to bridge the learning gap in the country? The government spends considerable resources to build and further education requirements for children. However, there are several challenges that the broader education sector in India face today. These include infrastructure, lack of good quality teachers at scale and difficulty in attracting talent, etc., Since our population is growing unlike other developed economies, deployment of resources is a big challenge. While our focus is to expand to international markets to help achieve scale and build a global brand, we are also working on creating learning programs in vernacular languages to provide access to quality content and teachers to the students even in the remotest parts of the country. For our international expansion, we are looking for the right partnerships that will help us scale and expand globally. Currently almost 75% of our users come outside metros, which makes for a compelling case to expand our offerings in local languages. We have recently launched language switch option in Hindi, that will not only help in onboarding the platform but also help gain a better foothold in English. We are also working on providing content in other regional languages to help students meet their aspirational goals. I come from a public-school background and have seen first-hand challenges that the education system faces especially in tier 2 cities and beyond. No single institution – government or private - can solve these issues single handedly. I believe a public-private partnership may help address some of these challenges especially at scale. We would be happy to support the government in some of these initiatives and help encourage learning across India. B investments. What are some of the underlying factors in choosing investors present in your cap table? yju’s has been successful in raising multiple rounds from some very renowned investors hailing from different geographies and industry W hat is the vision for Byju’s? Where do you see the company 5-10 years from now? Majority of our investments have been towards building scale and technology capabilities. Our investors have been great partners in our growth story. They have not only helped with capital requirements for expansion but also provided the necessary connects and deep understanding across geographies to help our expansion plans. We have also focused on working with the right set of investors and have evaluated aspects outside of the color of money, we are fortunate to have such impactful group of investors. Our vision is to be one of the largest education provider brands in the world. While starting a mission company is easy, sustaining a mission-led organization is challenging. As I stated previously, the market needs standardized education and new methodologies/formats to be introduced so as to engage students. To move from the traditional classroom system where teaching is one-way traffic to the one where teachers are facilitators of learning and also, mentors for discussions in classrooms is essential. At Byju’s, we have made small strides in this direction and with increased traction we believe this is possible in the near future. Our partnership with investors has been very satisfying as they come with experience of broad business segments that help with strategy and understanding of various markets across the globe. And as we work towards being a global brand, these partnerships will help immensely. We continue to garner interest from several marquee investors, and as we further our international expansion, we will raise funds when required. But the goal beyond numbers, is to continue our focus on enjoying education and making students across the world fall in love with learning. Capital Matters 17

E-commerce and consumer internet: accelerating tomorrow today In 2018, e-commerce and consumer internet companies raised over US$7 billion in PE/VC capital (including venture debt) across approximately 200 deals. About US$6 billion of this was early-stage capital and US$1 billion was invested as expansion/growth capital. The year also saw seven e-commerce and consumer internet companies join the unicorn club, becoming one of the most active years in terms of activity for the sector. Ankur Pahwa Partner and National Leader, E-commerce and consumer internet, EY 18 Capital Matters

Issue 2 Investment trends B Segments like hyperlocal, travel and hospitality, B2C, EdTech and wallets and payments were key areas of investment. Start-ups like OYO, Swiggy, Byju’s, PayTm Mall, Pine Labs, Zomato, Udaan, PolicyBazaar and CureFit collectively raised a lion’s share of the US$4.6 billion of investments in 2018. A majority of the funds raised last year were towards building supply chain, expanding to new locations including global markets, developing and bringing new and innovative product offerings to the market. Alibaba’s investment in BigBasket and PayTm, Tencent’s investment in Dream11 and Naspers investment in Byju’s and Swiggy have shown that the Indian start-up ecosystem is thriving and poised for growth. ig-ticket investments and differentiated segments have witnessed an uptake: Sector trends in the start-up ecosystem in India. Inorganic growth has been a quick way for companies to gain market and wallet share of the customer. This is not only limited to buying competitors, it is also gaining ground into potential expansion areas. Walmart’s acquisition of Flipkart has certainly been the headline that grabbed attention from an exits perspective. There have, however, been other acquisitions/consolidation deals such as Reliance’s acquisition of Saavan (music) and Embibe (EdTech), Zomato’s - TongueStun, Amazon’s - Tapzo, Ola’s – Ridlr and Foodpanda, Paytm’s acquisition of TicketNew and Nightstay and BigBasket’s acquisition of Kwik24, RainCan and Morning Cart. Players, both large and small, are entering this space to address the Hyperlocal 2018 also saw a reasonable broadening of sector investments, in 2017, 75% of capital was invested in B2C, mobility and wallets in comparison to only 26% in 2018. Even in B2C, it was largely in B2C- horizontals as compared to 2018 where the investments have largely been in B2C-vertical players. micro-location, on-demand delivery opportunity. The industry is barely scratching the surface and there are a lot of opportunities ahead in the food ordering, e-pharmacies, groceries and foods, concierge and household services. Investment in 2018: US$1.6 billion There has also been a rise in the new class of investors. Overseas funds are looking to invest in the space, in addition to the angel investor funds who have seen the success of the Flipkart exit and are more bullish in the Indian market. I at substantial gains recorded by the investors in the recent past have also proved that trust is well placed by the PE/VC community EdTech is gaining traction and is disrupting a long overdue space, as it has immense potential to help students and adults educate and upskill themselves. It continues to focus on better modes of delivery by providing students and parents a more intuitive experience, simulations, gamification, data analytics, real- time feedback and customized and conceptual learning. Investment in 2018: US$742 million EdTech ncreased investor confidence and segment consolidation driving investments: Exits Capital Matters 19

April 2019 “ companies are also addressing problems through innovation and technology in many other segments such as mobility, healthcare, logistics, gaming and classifieds which have combined raised US$1 billion in investment capital. Maintaining a category focus, better assortment planning, distributed supply chain and logistics, expanding rural reach and enhancing customer experience through data driven personalization are some areas of focus for this segment. Investment in 2018: US$1 billion. Social: Social commerce is bringing to fore the mix of commerce and influencers resulting in a more collaborative and personalized recommendation of products to a specified social group. With social media platforms witnessing exponential growth in India, the amount of time spent using these platforms provides greater opportunities for product discovery and personalized experiences. While this kind of community commerce is in its nascent stages, there is certainly a need and demand that will have greater influence in the e-commerce ecosystem going forward. Investment in 2018: US$200 million. Social B2C E-commerce and consumer internet Globally as well as in India, B2B e-commerce is growing at a much faster rate than the B2C e-commerce market. While this segment is dominated by consumer durables, mobile accessories, apparels and home furnishings, we are now seeing increasing buyers in the construction and industrial supplies as well as FMCG products, where digital is now supplementing traditional distribution. Investment in 2018: US$540 million. B2B Fintech and payment companies are transforming the financial services industry in India by providing a wide range of differentiated services. These platforms are simple, integrate digital transactional flow and leverage user Fintech and payments The millennial traveler looks for good, affordable and experimental travel options that have a data as a surrogate to provide services to first time or non-traditional consumers. Services such as peer-to-peer lending, digital transactions, wealth management services, etc. have seen increasing consumer interest and adoption giving competition to traditional incumbents. As per reports, the Fintech industry is expected to touch US$8 billion by 2020. Investment in 2018: US$912 million. Hospitality and travel strong tie-in with social media. The rise of the popularity of social media influencers has fueled the growth of companies catering to these needs. Adoption of new age technology solutions such as big data analytics, IoT, AI/ML for predictive pattern recognition, chatbots, AR/VR, etc. have helped provide a convenient, hassle-free and one-stop shop experience to customers. Investment in 2018: US$1 billion. In addition to the above, e-commerce and consumer internet companies are also addressing problems through innovation and technology in many other segments such as mobility, healthcare, logistics, gaming and classifieds which have combined raised US$1 billion in investment capital. These sectors have the capability to disrupt their respective segments allowing for greater access to products and services with the consumer being the ultimate winner. 20 Capital Matters

Issue 2 Rural market Vernacular language Challenges and opportunities The reasons for growth are manifold including sustained growth in the disposable income over the last decade, availability of affordable smartphones and data tariffs, continued support and stimulus provided by the government through programs like Start Up India, Stand Up India, Make in India, etc. creation of digital payment acceptance infrastructure. Global expansion Digital infrastructure Cash burn Logistics and distributed infrastructure • Rural market provides for a sizeable opportunity for online retail companies. With rural internet users expected to increase by 2.5 times, in comparison to 1.1 times for urban internet users, an impetus is in place for the next big wave of growth. • Digital infrastructure still requires greater focus to support the growth anticipated with the sector. With upcoming requirements such as data localization as part of the data privacy policy under discussion, it is important that both public and private players proactively start building digital infrastructure to the required scale. Opportunities Challenges • ● Vernacular language content is another key growth driver in the Indian digital journey. 88% of the Indian population is non- English speaking, hence it is critical that this gap is addressed. This will also provide for easier adoption of digitally available services, information sharing and the creation of a much larger customer base, thus increasing traffic and sales. • ● Conversion of social media interacting users to e-commerce transacting users is another key challenge. • ● Players will need to manage their cash burn better and improve unit economics across segments to be competitive. There needs to be an increased focus on profitability to sustain growth and market share. • ● Logistics and distributed infrastructure will play a core role in the last-mile delivery of products and services. Telematics, route optimization and IoT will need to be better leveraged to improve efficiency and reduce costs. • ● Global expansion of homegrown services has already seen initial success and should play out in the future. With many geographies facing similar issues and use cases already in place, many countries are ripe for disruption and are natural homes to certain products/ services. • ● Clear and consistent policies and regulations from the government will help not only companies but investors as well. The government has taken some proactive measures to ensure appropriate consultation with stakeholders, which will certainly help with robust and comprehensive policy-making. Capital Matters 21

A new high for the Indian PE/VC industry in 2018 Vivek Soni Partner and National Leader, Private Equity, Transaction Advisory Services, EY “ five years can be the Golden Age for Indian PE/VC industry. Policy and political stability permitting, annual Indian PE/VC investments could potentially exceed $65 billion by 2025. PE/ VC investments trends to watch out for in 2019 include the rising traction in distressed debt investing and change in ownership of passive infrastructure (roads, pipelines, telecom infrastructure) and commercial real estate portfolio’s from government / private sector hands to that of alternative investment managers. Acceptance of REIT’s and Invit’s amongst investors is expected to influence this trend in a material way. In 2018, PE/VC investments and exits in India reached a total of US$61 billion from US$200 million in 20 years, a CAGR of almost 33%! Thanks to strong exits over the past three years and compelling growth potential, India now ranks amongst the most attractive emerging markets for LP investors. The next 49 Buy-outs (worth US$9.9b) 35.8b 26b 11 PE-backed IPOs US$16b Largest exit (Walmart-Flipkart US$ US$ Investments Exits 8 6.4b Investment in start-ups US$4b Secondary deals (41 transactions) US$ US$1b+ deals 22 Capital Matters

Key highlights * PE/VC exits at all-time high of US$26 billion in 2018 PE/VC investments at an all-time high of US$35.8 billion in 2018 • Compared to 2017, investments increased by 37% in value terms, while deal volume increased by 29% • Exits increased by almost 100% compared to 2017 and are almost equal to the value of exits in the previous three years combined Deals are getting larger and more complex Volatility in markets dampen open-market and IPO exits • Entry of LPs as direct investors and global buy-out funds making large India allocations is changing the deal landscape 78 deals>US$100 million accounting for 73% of PE/VC investments in 2018. Eight US$1 billion plus deals • At US$1.7 billion, open market exits declined sharply to less than a third of the values recorded last year both in terms of value and volume. Open markets exits accounted for 80% of deal value in 2017 and the same dropped to 6.5% in 2018 Exit via IPOs recorded a decline of more than 50% (both value and volume) as market conditions no longer remained conducive for IPOs • • Buy-outs are becoming more prominent • In 2018 there were 49 buy-outs aggregating to US$9.9 billion, surpassing all the previous year highs and almost equal to the value of buy-outs in the previous three years combined Secondary and strategic exits gain prominence • As buy-outs become more prevalent, strategic sale is emerging as a strong option with global corporates like Walmart, Teleperformance S.A., Arrow Electronics Inc., Ebix etc. hungry to get a foothold in the Indian market, are willing to give good valuations for quality businesses With record levels of dry powder, PE funds are keen to take-up quality assets from early investors and are also ready to provide capital for the next level of growth to these companies Start-up funding on an uptrend • On a y-o-y basis, investment in start-ups increased 84% to US$6.4 billion compared to US$3.5 billion in 2017, surpassing the US$4.8 billion high of 2015 Walmart-Flipkart deal has revived confidence and large venture capital investors like SoftBank, Tencent and Naspers are deploying significant amounts of capital • • Total PE/VC investments trend (US$ billion) Investments (US$ billion) Number of deals 1,000 40 770 767 800 595 588 30 469 600 20 400 10 200 11.7 19.6 16.2 26.1 35.8 0 0 2014 2015 2016 2017 2018 Investment value (US$ billion) Number of deals Total PE/VC exits trend (US$ billion) Investments (US$ billion) 30 300 254 260 Number of deals 25 250 211 166 174 20 200 15 150 10 100 5 50 13.0 26.0 6.7 6.5 3.4 0 0 2014 2015 2016 2017 2018 Investment value (US$ billion) Number of deals Capital Matters 23

Top PE/VC sectors for investment US$7.9b 144 deals US$2.2b 72 deals Life Sciences • High latent demand, government initiatives and successful IPOs keep interest in the sector high • Domestic consolidation continues through acquisition and platform deals Financial Services • Top sector for PE/VC investments despite recent headwinds • Fin-tech continues to attract investors US$6.3b 57 deals US$2.1b 18 deals Infrastructure and Real Estate • Sovereign wealth funds and pension funds most active • Yield generating commercial real estate and logistic parks preferred investments • Retail assets witness renewed interest Power and Utilites • Clean energy dominates deal activity • Government policy support and incentive schemes drive investments • Significant investment into capacity building via investment platforms US$1.7b 35 deals US$4.6b 91 deals E-commerce • Rising activity in hyperlocal, edtech and healthtech space • Mega deals by venture investors like SoftBank, Tencent and Naspers • Market leaders emerging in each sub-segment Retail and Consumer Products • Consolidation/rationalization driven by synergy around distribution • Online/offline sector convergence • Large deals in modern retail format Disclaimer: For the purpose of this analysis we have included deals that have a significant e-commerce and consumer internet component in their business model but are otherwise included in the core sector they belong to, for example, Paytm from Financial Services. Top PE/VC investments in 2018 Deal type Target Acquirer(s) Deal Value (US$m) Stake % PIPE Buy-out Start-up Growth HDFC Select NHAI road assets Bundl Technologies (Swiggy) Airtel Africa GIC, KKR, PremjIinvest, OMERS and others MAIF2 Tencent, Naspers, DST Global and others Warburg Pincus, Temasek, SingTel Innov8, SoftBank ADIA, TPG 1,731 1,462 1,000 1,250 4 100 NA 28 Growth UPL Corporation 1,200 NA Top PE/VC exits in 2018 Deal type Target Seller(s) Acquirer(s) Deal Value (US$m) Stake % Strategic Flipkart SoftBank, Naspers, Tiger Global and others Blackstone Walmart Inc. 16,000 77 Strategic Intelenet Global Services Vishal Megamart Teleperfor-mance S.A. 1,000 100 Secondary TPG, Airplaza Retail Holdings Partners Group, Kedaara Capital Madison, Westbridge, Rakesh Jhunjhunwala ReNew Power 769 100 Secondary Star Health and Allied Insurance Ostro Energy ICICI Ventures, TATA Capital and others Actis 745 70 Strategic 692 100 * Source: EY analysis of VCCEdge data 24 Capital Matters

© 2019 EYLLP. All Rights Reserved. ED none. How soon after acquisition should you begin planning the exit? EY helps clients begin with the end in mind to help investors improve their return. ey.com/privateequity #BetterQuestions

April 2019 What is driving the continued interest in Indian consumer companies? Nitin Gupta Partner, Investment Banking Advisory, Transaction Advisory Services, EY I on an opportunity to scale, explore untapped pockets for deeper ndia is a classic example of a quintessential growth story - a story anchored penetration and increased levels of spending capacity. These factors have also helped India emerge as a major contributor to the global economy. Final consumption expenditure (in US$ trillion) CAGR: 25.4% 3.6 1.82 2017 2020E Source: IBEF FMCG Report_November 2018 26 Capital Matters

Issue 2 value in 2018. Some of the recent marquee M&A deals in this sector are: (1) Unilever’s acquisition of health food drinks portfolio of GSK in India; (2) Zydus Wellness’s (an arm of Cadila Healthcare) acquisition of malted food drink Complan, Glucon-D energy drink, Nycil talcum powder and Sampriti ghee business of Kraft Heinz India; (3) Samara and Amazon’s acquisition of More retail chain from Aditya Birla Group; (4) Walmart’s acquisition of Flipkart. The consumer sector in India is poised to witness strong growth basis several factors like rising per capita income, existing low penetration levels, favorable demographics and urbanization among others. The final consumption expenditure is expected to increase at a CAGR of c.25% and reach nearly US$3.6 trillion by 2020 from US$1.82 trillion in 2017, thereby putting India on the path to become the third largest consumer market. Global businesses that are experiencing relatively slower growth in other geographies are actively looking at the Indian market to bolster their businesses. While these companies always have the possibility of entering India via the greenfield route, an acquisition (or alliance) is preferred and more beneficial in most cases. The key motivation for this is the sheer diversity in a country like India - be it of people, geography, language and government policies. It is thus often more time-consuming and challenging to attempt to establish a strong consumer brand from the ground up and easier to find the right partner to get a head-start. An important stimulus which is expected to provide a further boost to the sector is the unprecedented internet penetration. The number of online users is expected to more than double to 200 million in 2020 from 90 million in 2017, with the online FMCG market increasing from US$20 billion in 2017 to US$45 billion in 2020. Sustained interest from global players The consumer sector in India is one of the major sectors that has continued to witness significant interest from global companies in the recent years. One of the key reasons for this traction is the stagnation of the middle class in some of the leading and developed economies, which is in sharp contrast with the middle-class in India. While the middle-class is shrinking in some key European and North-American countries, it continues to grow at a high rate in India, which provides a big opportunity for increased consumption to the global investor. IKEA, Netflix, Harley Davidson, Walmart and Amazon are examples of large global companies that India’s growing middle-class has attracted. Also, consumer preferences are fast-changing towards quality and branded products, which is expected to lead to the organized sector’s growth at an even faster rate and increased spend on consumer goods. The key pillar for success for any consumer company is access to a strong distribution network. With modern retail accounting for only c.11% of the overall retail in India, establishing a strong distribution network across the innumerable mom and pop stores is not only challenging but also time and resource consuming. Land acquisition is another big hurdle faced by foreign companies. Thus, acquisitions have emerged as an attractive option for global players to enter the India market. Recent transactions in the food and beverage and dairy space are good examples of companies acquiring a well-established brand as well as a distribution network to penetrate in the growing Indian market. The long-term outlook for the sector continues to be vibrant as the attractiveness of the sector will continue to drive interest from global foreign players to pursue Indian businesses in the lookout for established consumer bases and distribution networks. The attractiveness of this sector is further reinforced by the fact that this was the most active sector by deal Indian households, by income (millions) Annual Gross Household Income (INR Lacs) 2025 2005 2016 15.8 (5.2%) 6.5 (2.4%) 3.1 (1.5%) Elite (>20) 33 7 17 Affluent 10–20) (3.3%) (6.4%) (10.8%) 17 40 61 Aspirers (5–10) (20.0%) (8.1%) (15.0%) 89 121 (45.4%) 140 (45.9%) Next Billion (1.5 to 5) (42.6%) 93 82 55 Strugglers (> 1.5) (44.5%) (30.8%) (18.0%) Source: BCG CCI Proprietary Income database, BCG analysis Capital Matters 27

Ernst & Young LLP EY | Assurance | Tax | Transactions | Advisory About EY EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities. EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com. Ernst & Young LLP is one of the Indian client serving member firms of EYGM Limited. For more information about our organization, please visit www.ey.com/in. Ernst & Young LLP is a Limited Liability Partnership, registered under the Limited Liability Partnership Act, 2008 in India, having its registered office at 22 Camac Street, 3rd Floor, Block C, Kolkata - 700016 © 2019 Ernst & Young LLP. Published in India. All Rights Reserved. EYIN1905-001 ED None This publication contains information in summary form and is therefore intended for general guidance only. It is not intended to be a substitute for detailed research or the exercise of professional judgment. Neither Ernst & Young LLP nor any other member of the global Ernst & Young organization can accept any responsibility for loss occasioned to any person acting or refraining from action as a result of any material in this publication. On any specific matter, reference should be made to the appropriate advisor. AGK ey.com/in EY EY Careers India @EY_India EY India @ey_indiacareers