Download

1 / 4

40 likes | 41 Views

Applicant's age should be 21 to 55 years to avail Pradhan Mantri Awas Yojna benefits. However, if the age of the head of the family or the applicant is more than 50 years, then his principal legal heir will be included in the home loan.

E N D

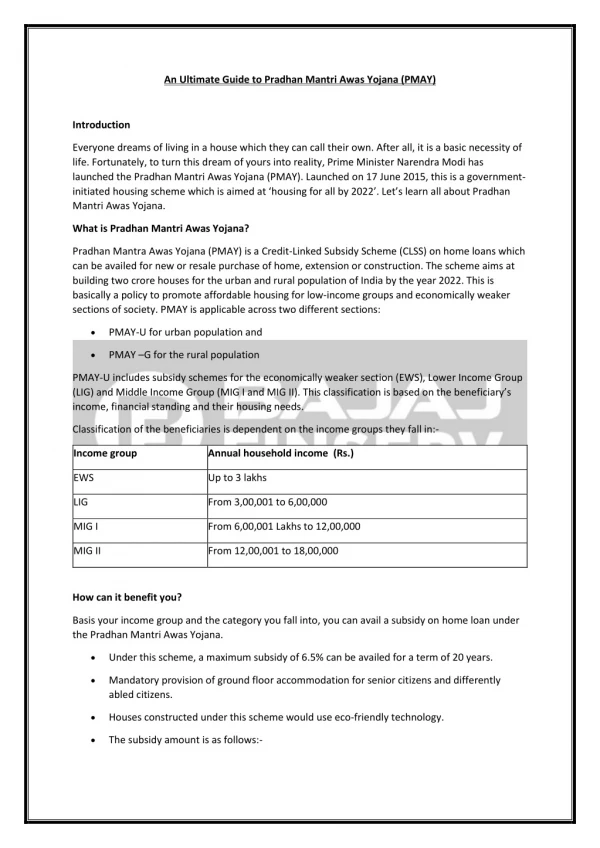

Everything about the Pradhan Mantri Awas Yojana There is no denying that there is a housing scarcity in India. Many individuals are unable to purchase their own homes since there is so much demand. The government has responded to the issue by establishing the Pradhan Mantri Awas Yojana, a national affordable housing program for low-income families in India. But how does it work? What exactly is PMAY and what can you anticipate if you meet the criteria? And, more importantly, how does it work? We’ve compiled some basic information about PMAY in this blog article to assist you to understand.

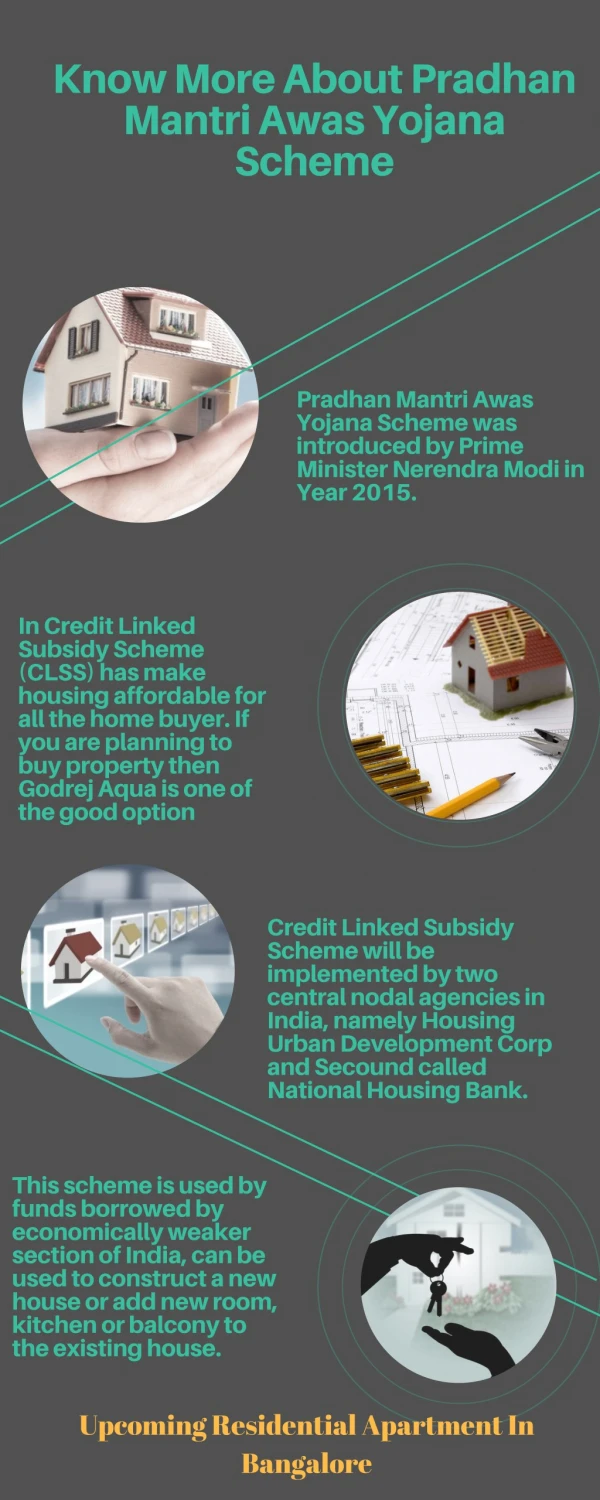

What is Pradhan Mantri Awas Yojana The Pradhan Mantri Awas Yojana is a government program that was created by India’s Prime Minister, Narendra Modi. The government has planned to provide accommodation for all Indians by 2022. In April of the year 2015, Narendra Modi launched a housing assistance program called PMAY-CLSS. It is designed to provide affordable housing to all Indians, particularly those who live below the poverty line. Depending on your state of residence and your income range, the PMAY-CLSS program has varying eligibility criteria. The banks provide loans at a significantly reduced interest rate due to the fact that the government pays the rest on behalf of the applicant. This is a type of government loan that helps low-income families purchase a home.

Eligibility Criteria for PMAY Every applicant must satisfy the PMAY committee’s eligibility standards in order to obtain a home or financial aid from the government. They are categorized into six categories, as follows: Economically Weaker Section (EWS): Those who come under the category of EWS have a yearly income of less than Rs.3 lakh. However, to confirm their claims, the government requires proof from an applicant claiming to be from EWS. Light Income Group (LIG): Those who make up the LIG group have a yearly household income of Rs.3 lakh to Rs.6 lakh. They must also submit sufficient evidence to support their financial condition in order to be considered. Medium Income Group (MIG1): Individuals with a yearly household income of less than Rs.12 lakhs are eligible for the MIG1 program. Loans of up to Rs.9 lakh are available for the construction of a house for these individuals. Women: Women who fall into one of the EWS/LIG categories will be eligible for the PMAY scheme. A few more basic criteria are supposed to be achieved. For instance, a husband, wife, and unmarried children must all be included in the case of a beneficiary who is a family. Also, no family member should have a home in his or her name. Eligibility Criteria for Beneficiaries: 1. A husband, wife, and unmarried children will all be part of the beneficiary family. A single adult earning member of a household (regardless of marital status) can be considered as a separate family. 2. In the event of a married couple, only one spouse or both together in joint ownership may receive a single house, dependent on their income. 3. The unit should be named after the woman head of the family or in their joint name if the male head of the house and his wife are involved. If there is no adult female family member, the home may be named after the male resident. 4. The recipient family should not own a well-built house in any part of India, either in their own name or that of another member of the household. 1. The applicant should not have received government aid for housing under any housing program in India.

Some additional points to know If you are the recipient, your family should not own a concrete residence in your name or that of any member of your family in any state of the country. A single government tax incentive is available to married couples, regardless of whether one spouse or both spouses are involved. In order for this scheme to be effective, the beneficiary household must not have received central assistance under any housing program from the Government of India or any benefit under any PMAY.