Download

1 / 15

150 likes | 387 Views

China Banking Regulatory System And Sustainable Business Development Of Foreign Banks In China. WANG YAN XIU Deputy Director-General Banking Supervision Department III China Banking Regulatory Commission May, 2005. Outline of CBRC. Why CBRC

E N D

China Banking Regulatory System And Sustainable Business Development Of Foreign Banks In China WANG YAN XIU Deputy Director-General Banking Supervision Department III China Banking Regulatory Commission May, 2005

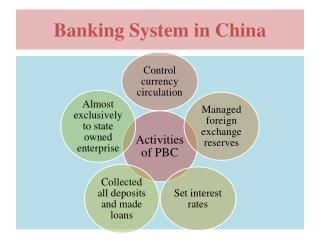

Outline of CBRC Why CBRC • Separate banking supervision function from the PBC, to enable the PBC focus on monetary policy & its implementation; • Enhance independence, specialization, effectiveness and authority of banking supervision • Establish a comprehensive mechanism among CBRC, CSRC and CIRC to form a teamwork to prevent financial risks.

Outline of CBRC Objectives • Protect the interests of depositors and consumers through prudential and effective supervision; • Maintain market confidence in China’s financial system through prudential and effective supervision; • Promote public awareness and understanding of modern finance through customer education and information disclosure; and • Reduce financial crime and maintain financial stability.

the major responsibilities of CBRC • formulate supervisory rules and guideline for banking institutions • authorize and terminate business of banking institutions • conduct fit and proper tests for banking directors • conduct off-site surveillance and on-site examinations of banking institutions • perform other duties assigned by the State Council.

Legislation of CBRC • Law of PRC on banking regulation and supervision • Administrative rule governing the financial licence • Administrative rule governing the Auto financing Company • Provisional rule on the pricing of Services by Commercial Banks

China’s banking sector At the end of 2004, China’s banking sector comprised • four wholly State-owned commercial banks • three policy banks, • eleven joint-stock commercial banks • four asset management companies • 112 city commercial banks • 723 urban credit cooperatives • 34,577 rural credit cooperatives • 30 thousand postal saving institutions.

Foreign Bank Operation in Chinaby the end of 2004 • Foreign banks branches and sub-branches 186 • Wholly foreign owned bank and sub-branches 16 • Joint venture banks 5 • Foreign finance company 4 • Total operational entities 211 • Representative office 220

Licensing Standards: Representative Offices • Sound home supervision • Licensed financial institutions by home financial authorities • Good performance • sound management • compliance

Licensing Standards: Branches • Sound home supervision • Approval by home supervisor • Total assets no less than US$ 20 billion • Capital Adequacy Ratio no less than 8% • Representative offices established in China for more than 2 years

Business: Foreign Banks • Deposits • Loans and advances • Bills acceptance and discounting • Trading in government bonds, financial bonds, and other non-equity securities in foreign exchange • Letter of credit and guarantee • Domestic and international settlement • Trading in foreign exchange as principle and broker • Exchange in foreign currency • Inter-bank borrowing and lending • Bank cards • Safekeeping service • Credit investigation and consultancy • Other businesses approved by CBRC

Eligibility of Senior Management Essential requirements for Subsidiary: Chairman, Vice Chairman, CEO, Branch: General Manager, Deputy General Manager • Compliance • Competence: expertise and management experience • Good track record

Further Opening-up Under the WTO • Open 18 cities for foreign banks to conduct renminbi business • Allow eligible foreign banks to provide RMB services for Chinese enterprises • Increase the single foreign equity holding in Chinese financial institutions to 20 per cent from 15 per cent, and set the maximum foreign equity holding at 24.99 per cent • Lower the operating capital requirement on foreign banks • Provide time limits for review and approval

further Opening-up Under the WTO • Issue regulation on credit card business to facilitate foreign involvement • Open the Chinese auto financing market and approve the preparation of three foreign auto financing companies • Allow the foreign banks to provide over 100 types of business in12 lines, including, QFII custodian, on-line banking, T-bond underwriting, cash management and pooling, financial derivatives, wealth management

Measures to improve supervision of foreign banks Establish risk rating for foreign bank supervision • Foreign banks branches subject to SOSA ranking (Strength-of-Support Assessment) & ROCA rating (Risk management, Operational control, Compliance, Asset quality) • Foreign bank subsidiaries and Sino-foreign joint-venture banks subject to CAMELs • Supervise Foreign banks by consolidated base