Download

1 / 16

160 likes | 257 Views

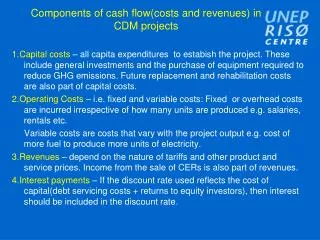

Practical issues in identification and development of CDM projects. AIT, Bangkok, October 20, 2005 Soeren Varming Senior Consultant, Climate Change sva@econdenmark.dk. ”Arch type” CDM versus reality.

E N D

Practical issues in identification and development of CDM projects AIT, Bangkok, October 20, 2005 Soeren Varming Senior Consultant, Climate Change sva@econdenmark.dk

”Arch type” CDM versus reality • “Arch type – CDM”: A collaboration between two private entities sharing technology and financial risk • “Reality”: Governments or carbon funds with no other involvement in the underlying project - only buying CERs • Why this change in concept?

Private sector IS active! • FDI in Malaysia in 2003 was 15 billion RM (4 billion USD) • Annual income from sale of CERs in 2010 could amount to 190 million RM (50 million USD) or 1,3% of annual FDI • The private sector IS active • But can private sector take interest in CDM?

Case study 1 – Impact of CDM for biogas from Palm Oil Mill Effluent • Mill with capacity of 40 ton of Fresh Fruit Bunches per hour • Power generated will be connected to the grid • Contribution CDM is 6-10 sen/ KWh • Impact of CDM is different per technology used

Case study 2 – Impact CDM on CHP project • CHP technology used at a palm oil mill • Power generated will be connected to the grid and partly used for on site consumption • Project displaces power from grid connected fuel plants and biomass used for heat generation (e.g. no CERs related to heat) • Contribution CDM is 1.1 sen/ KWh

Issues for private sector in Annex B countries • Companies covered by EU’s Emission Trading Scheme tend to focus on core business • Utility companies tend to focus on regional markets • Costs of carbon credits not enough to invest outside core business • Tendency to ”sit on the fence” – or go for a fund • Technology providers are getting alert • But are (most often) neither investors nor CER buyers • Multi national companies within high emission industries and with emission reduction commitments pioneers • Cement

Issues in host countries – CDM related • CDM is still a new concept • Will anybody really pay for CERs? • Bad experiences with national and international approval processes • Complicated and long procedures • This IS changing! • Timing in project cycle • CDM does solve all problems for all projects • Lack of clear government policies on CDM

Issues in host countries – non-CDM related • Still a lot of barriers for CDM project implementation • Power purchase agreements for small RE projects • General grid connection conditions • Subsidies for fossil fuels • Financing • Inertia in decision processes in large companies

CDM – increasing security • 46 methods approved by CDM EB • 25 large scale methods • 15 small scale methods • 6 consolidated methodologies • Increasing number of projects registered • First CERs due soon • National approval processed being streamlined

CDM: From buyers to seller market? • Lack of projects to meet Annex B demands for credits • More buyers engaging…. • In the early phases: WB and CERUPT • Now many governments and funds • … lead to competition in terms • Covering upfront cost • Providing technology - good or bad? • Price - increasing

Host country governments:Don’t kill the baby by too much attention • Host country approval: Be aware of the roles • Confirmation of Sustainable Development • OE will handle additionality • Private investor will handle technical and financial feasibility • Approval procedures must become simpler and faster • Coordination with other policy instruments • Ambivalence towards multinational companies limiting partnerships

Annex B governments:Integration with other development activities • CDM is run within special routines and with focus on low prices • CDM is a necessary element in a post-2012 climate - regime • CDM could be seen as final stage of ODA • Market penetration of technologies • Provide funds and incentive for O&M • Controversial – ODA diversion • Facilitation of private partnerships

Private companies in Annex B countries:Plan for the future • CERs prices will most likely be determining for compliance costs • And projects does not come by them selves – There is no domestic market in host countries • Develop internal tools for carbon assets and liabilities • Consider CDM in relation to foreign investments • CDM as part of Corporate Social Responsibility ?!

Project developers in developing countries:Seize the opportunities • Be aware of opportunities • Methane reductions • Direct saving/replacement of coal • Industrial gasses (HFC, N2O, SF6) • Screen project portfolio • Include CDM early in project cycle • Get help for the paper work • Royal Danish Embassy in Bangkok, Jakarta, Kuala Lumpur • Private consultants

Thank you ! Soeren Varming Senior Consultant, Climate Change sva@econdenmark.dk + 601 9256 7970