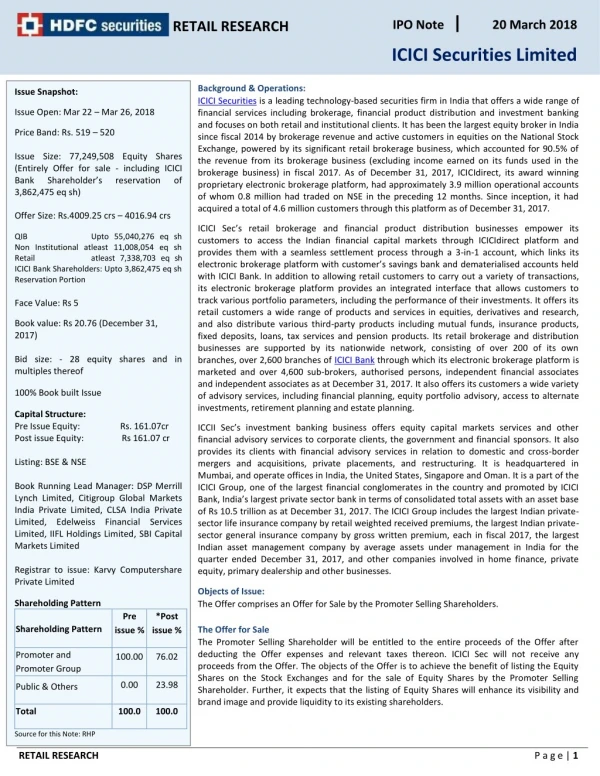

Download

1 / 29

290 likes | 420 Views

United Breweries Limited ICICI Investors Conference Singapore. March 2007. India and the Beer Industry. Indian Economy. The current year growth rate is 9% The growth is largely propelled by local consumption hence lesser prone to global changes.

E N D

United Breweries LimitedICICI Investors ConferenceSingapore March 2007

Indian Economy • The current year growth rate is 9% • The growth is largely propelled by local consumption hence lesser prone to global changes. • Inflation currently at 6% giving impetus to growth • Substantial increase in the disposable income in the age group of 20 to 30 years

Indian Demographics – favorable to growth in beer consumption Current population 1.1 billion Over 50% of the population is below the age of 25 years The demographics to remain almost unchanged till the year 2020 Core target market is 18-30 year olds As initiation to alcohol consumption is through low alcohol beverages like beer – excellent opportunity for growth in beer consumption over the next decade and half.

Beer Industry in India • Policies & Regulations are driven by State Government • Highly regulated with restriction in movement between states • 65% of the Indian market is state controlled – Distribution by Govt. Corporations, implications upon pricing • Advertising strictly prohibited, advantage for existing players, major barrier to entry

Beer Industry in India contd. • State governments like Punjab, Rajasthan, Haryana & Chandigarh have in recent past made substantial changes in the previous distribution methods making beer more affordable as well as profitable. • Government corporations are now approachable and not averse to make changes • There have been recent recommendations by some governing bodies to de link beer from spirit and have a common national duty structure much lower than the current duty levels

AFFORDABILITY Duty not set according to alcohol content Highest duty in the world Expensive alcoholic beverage AVAILABILITY 55,000 licensed outlets across the country 1 per 20,000 people In UK 1 per 350 people Beer Industry in India contd Beer is not the alcoholic beverage of the common man

Alcohol Consumption <0.5% Wine 5% Spirits/ Liquor 8% 78% 21.5% Beer 87% Emerging Markets India

Consumption Per Capita 83 litres 23 litres 24 litres 12 litres 0.7 litres India China World Average USA Indonesia

Industry Growth 30% 25% 20% 15% 10% 5% 5 Year CAGR 2005 2007 2006

Beer Segmentation +23.1% +35.4% Dec 05 Dec 06 Dec 05 Dec 06 MILD STRONG

Market Consolidation UBL Circa 83% of market SAB Miller Mohan Meakins MSIL Others Recent new Entrants: APB A – B Carslberg

Key Brands 22m 20m 3m 1.8m 1.8m 1.5m Kingfisher Sandpiper UB Export Kingfisher Zingaro Bullet Strong Mild Kingfisher Mild = No 1 top selling mild beer Kingfisher Strong = No 1 top selling strong beer Kingfisher Strong = No 1 top selling beer in India

Market Share Mild Beer 66% Strong Beer 38%

Market position by state: UBL is No.1 in 8 out of the top 10 state markets UBL Position % India Val. No.1 No.1 No.2 No.1 No.1 No.1 No.2 No.1 No.1 No.1 Maharashtra Tamil Nadu Andra Pradesh Karnataka Mumbai Rajasthan Uttar Pradesh Delhi Madhya Pradesh Kerala 16 13 13 10 8 7 6 5 3 2

Shareholder Return Share price Rs.323 to Rs.1495 462% 05/06 Share price Rs.149.5 to Rs.268.5 76% 06/07* * TSR to date, March 07

S&N UBHL Public 37.5% 37.5% 25.0% UBL 50% 50% Millennium Alcobev Ltd Legal Structure UBL & MAL Separate Legal entities UBL subsidiaries – KBDL and its 2 subsidiaries which would merge into UBL effective 1st Apr’06 UBL & MAL Separate Legal entities UBL subsidiaries – KBDL and its 2 subsidiaries which would merge into UBL effective 1st Apr’06 MAL has 3 Subsidiaries namely – MBIL, Empee and UMBL

Board Of Directors • 2 x UB Group (VJM Chairman) • 2 x S & N • 2 x Executive Directors (CEO & CFO) • 3 x Independent Directors

Latest financials December 2006

# Dec 06 results include ABDL + MBDL Comparative results for Dec 05 Income Rs. 453.8Cr EBITDA Rs. 88.57 Cr.

Outlook • GDP growing at healthier rate • Continued growth in disposable income • Encouraging demographics for over a decade • Anticipated liberalization of policies & duty structures • Industry consolidated with high entry barrier • UBL is in advantageous position to capitalize on opportunities