Download

1 / 5

50 likes | 177 Views

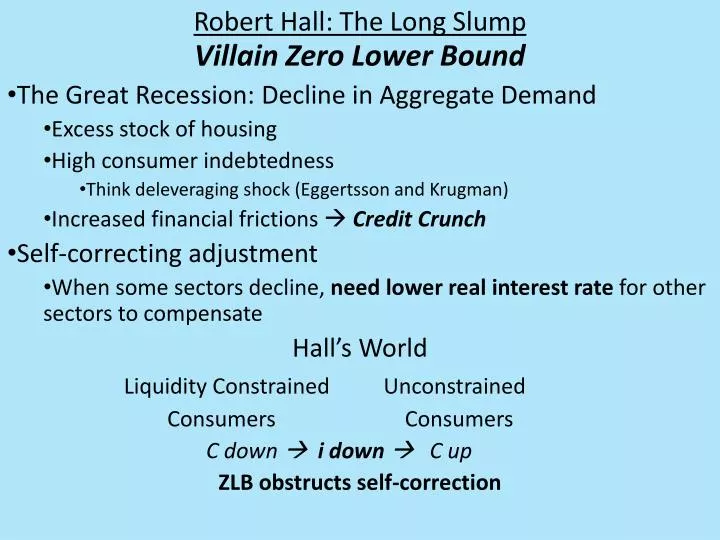

Robert Hall: The Long Slump. Villain Zero Lower Bound The Great Recession: Decline in Aggregate Demand Excess stock of housing High consumer indebtedness Think deleveraging shock ( Eggertsson and Krugman ) Increased financial frictions Credit Crunch Self-correcting adjustment

E N D

Robert Hall: The Long Slump Villain Zero Lower Bound The Great Recession: Decline in Aggregate Demand Excess stock of housing High consumer indebtedness Think deleveraging shock (Eggertsson and Krugman) Increased financial frictions Credit Crunch Self-correcting adjustment When some sectors decline, need lower real interest rate for other sectors to compensate Hall’s World Liquidity Constrained Unconstrained Consumers Consumers C down i down C up ZLB obstructs self-correction

ZLB A Long Slump Real interest rate = Nominal Rate – Expected Inflation • Wither Inflation? • NAIRU is failure … forget about a “natural rate” of unemployment • Inflation responds to u – ulowest in 11 mos • The good news: after 11 months of slump, no pressure for a drop in inflation rate…we’re not headed for deflation • The bad news: with unemployment where it is, can’t expect inflation to increase • Inflation won’t produce a low enough real rate

Hall’s DSGE Model • Cobb-Douglas production function • Cobb-Douglas utility functions: • Liquidity Constrained Consumers • Unconstrained Consumers • Search and match job market (DMP) • Worker “pays” for her job • If PV(job) falls, unemployment increases • Financial sector with zero lower bound • Cost of capital and financial frictions • Spread that intermediaries earn keeps them from absconding • When intermediary net worth down, it takes a bigger spread friction • Bigger spread heightened threat of borrower default increased cost of intermediation increased credit rationing CREDIT CRUNCH Results • In absence of ZLB, economy operates at full employment • BUT, ZLB and low inflation “Pinned” real rate Sustained Slump

Lessons from Our Lessons • Romer on Great Depression: Descent and Recovery (cited by Hall) • Gold standard mindset cruelly high real interest rate • Gold constraint reflation and recovery • Reflation driven by gold inflows, not policy (per Romer) • The German Inflation • Fixed discount rate (5%) and high inflation Negative real interest rate High employment

Hall on Policy • Fiscal Stimulus? • It is not that government purchases are ineffective but that government is incapable of executing a rapid and large increase in purchases • Price level targeting • If inflation lags target, public would expect high inflation as Central Bank tries to catch up to price target: πeupireal down • Phased in Value Added Tax (VAT) buy now! • Currency depreciation buy now! • Subsidize consumption until slump ends…then tax • Summers (in context of DMP labor market): Payroll tax cut small reduction in wage cost big increase in profit margin HIRING