Download

1 / 11

120 likes | 359 Views

Interest Rate SWAP. Ch9. Why Use Interest Rate SWAP. Reduce interest rate risk RSA (rate-sensitive asset) not equal to RSL (rate-sensitive liability) If RSA >RSL, then increase RSA (from fixed-rate to floating-rate) or/and decrease RSL (from floating-rate to fixed-rate) Reduce borrowing cost.

E N D

Why Use Interest Rate SWAP • Reduce interest rate risk • RSA (rate-sensitive asset) not equal to RSL (rate-sensitive liability) • If RSA >RSL, then increase RSA (from fixed-rate to floating-rate) or/and decrease RSL (from floating-rate to fixed-rate) • Reduce borrowing cost

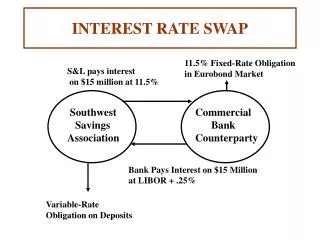

利率交換系指債信評等不同的募款人,立約交換相同期限、相同金額債務之利息費用,以共同節省債息的規避利率風險行為。利率交換系指債信評等不同的募款人,立約交換相同期限、相同金額債務之利息費用,以共同節省債息的規避利率風險行為。 • 典型的利率交換合約,一般為固定利率與浮動利率的交換,例如:甲公司想以6%的固定利率發行一筆2000萬美元的3年期公司債,但以該公司的信用等級,只能以6.5%的利率發行,惟若向銀行借款,則因該公司與銀行往來關係良好,可以6個月LIBOR(London Inter Bank Offered Rate)加碼0.5個百分點的浮動利率借到資金。此時,恰好乙公司也需要一筆2000萬美元3年期的資金,該公司雖偏好以浮動利率的方式借入,惟卻必須負擔6個月期LIBOR加碼1個百分點;至若發行公司債,因為乙公司在國際債券市場上有良好的知名度,故可以6%的固定利率發行。從而,甲公司與乙公司可各自發揮在浮動利率市場及固定利率市場的價格優勢,進行利率交換合約。透過利率交換,雙方皆可節省利息成本。

LIBOR係London Inter Bank Offered Rate)的簡稱,它是倫敦國際銀行同業間從事歐洲美元資金拆放的利率,拆放期限可從短期僅隔夜至長達5年,較常見的為3個月期或6個月期。 • 大多數主要金融中心都有類似LIBOR的利率,例如:荷蘭阿姆斯特丹的AIBOR、德國法蘭克福的FIBOR、以及法國巴黎的PIBOR。美國並無直接對應LIBOR的利率。美國的銀行間市場是聯邦基金市場,而貸款契約的基礎是基本利率(Prime Rate),此利率適用於信用等級最佳的借款者。LIBOR直接由市場供需決定,因此不斷變化;Prime Rate由銀行訂定,較不經常變動。

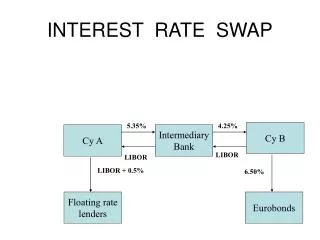

Interest-Rate Swap Contract(利率交換合約) • 1. Notional principle of $1 million • 2. Term of 10 years • 3. Midwest SB swaps 7% payment for T-bill + 1% from Friendly Finance Co.

Interest-Rate Swaps • Reduce interest-rate risk for both parties • Midwest (Friendly) converts $1m of fixed rate assets (rate-sensitive) to rate-sensitive (fixed) assets • Advantages of swaps • Reduce risk, no change in balance-sheet • Longer term than futures or options(20年) • Disadvantages of swaps • 1.Lack of liquidity • 2.Subject to default risk

Borrowing costs • Big Boy: • T-bill+2% for debt with floating rate and 7% for debt with fixed rate • Would like to borrow the money with floating rate • Little Guy: • T-bill+2.5% for debt with floating rate and 9% for debt with fixed rate • Would like to borrow the money with fixed rate • The borrowing costs of Big Boy are smaller than Little guy regardless of fixed or floating rate

No need to SWAP? • Comparative advantage versus Absolute advantage

For Big Boy • if he borrows the debt with fixed rate, then he can add a benefit of 2% • if he borrows the debt with floating rate, then he can add a benefit of 0.5% only • For Little Guy, • if he borrows the debt with fixed rate, then he can add a benefit of -2% • if he borrows the debt with floating rate, then he can add a benefit of -0.5% only

If Big Boy borrows the debt with fixed rate and Little Guy borrows the debt with floating rate, then the benefit for the whole system is? • How to allocate the benefit? • How to decide the swap contract?