Download

1 / 28

280 likes | 402 Views

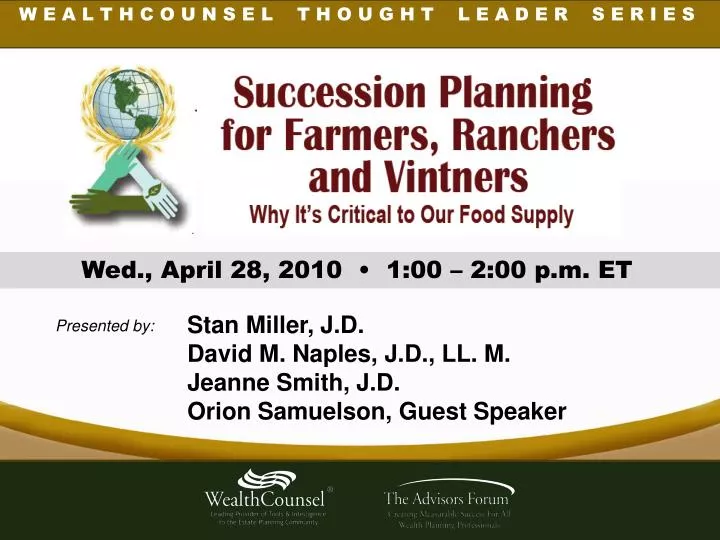

W E A L T H C O U N S E L T H O U G H T L E A D E R S E R I E S. Wed., April 28, 2010 • 1:00 – 2:00 p.m. ET. Stan Miller, J.D. David M. Naples, J.D., LL. M. Jeanne Smith, J.D. Orion Samuelson, Guest Speaker. Presented by:. HOUSEKEEPING.

E N D

W E A L T H C O U N S E L T H O U G H T L E A D E R S E R I E S Wed., April 28, 2010 • 1:00 – 2:00 p.m. ET Stan Miller, J.D. David M. Naples, J.D., LL. M. Jeanne Smith, J.D. Orion Samuelson, Guest Speaker Presented by:

HOUSEKEEPING Submit Questions via Console Chat Feature • At the end of the webcast: • Download CE Form • Download Speaker Bios NOTE: Slides and course materials may be downloaded from www.wealthcounsel.com/Webcast3.aspx

HOUSEKEEPING At the conclusion of today’s webcast, please take a moment to complete our short Feedback Poll & Survey.

David M. Naples, J.D., LL.M. • Shareholder, Leonard, Street & DeinardMankato, MN • Member, American Bar Association, Taxation Section, and Real Property, Trust and Estate Law Section • Current Chair, Estate Planning and Administration for Business Owners, Farmers and Ranchers Group

Jeanne Smith, J.D. • Principal, Jeanne Smith & Assoc.,PCCorvallis, OR • Member, WealthCounsel • Member, The Advisors Forum • Member, Oregon State Bar

Stan Miller, J.D.Moderator • Founder & Principal, WealthCounsel • Founder & Principal, Advisors Forum • Principal, Miller & Schrader, PALittle Rock, AR

Special Guest SpeakerOrion SamuelsonAgricultural Journalist, Chicago, IL • Broadcast Journalist, WGN Radio 720, Chicago • Host, National Farm Report Radio Program • Host, Samuelson Sez Radio Program • TV Co-Anchor, “This Week in Agribusiness” • Inductee, National Radio Hall of Fame

Farm Families Come From 4 Quadrants Passive Ownership of Land Active Farm Operation Higher Net Worth >$3.5 mil. Stan Miller J. D. Lower Net Worth <$3.5 mil.

Impact of Estate Tax Repeal on Farmers, Ranchers, and Vintners • Formula Gifts – issues on death of first spouse of 2010. • Types • Concerns • Property does not pass as intended • Liquidity issues • Basis issues David NaplesJ.D., LL.M.

Pecuniary Marital Deduction Formulas • Inadvertent disinheritance of surviving spouse • Estate tax from overfunded credit shelter trust • Fail to fully use basis step-up for Qualified Spousal Property

Pecuniary Credit Shelter Formulas • Overfund surviving spouse’s estate • May disinherit descendants • QTIP trust taxable if no “state-only” QTIP election

Potential Remedies • Define Code as it existed on December 31, 2009 • If no “state-only” QTIP election, consider outright marital gift with disclaimer • If have “state-only” QTIP election, consider all to QTIP trust

Annual Exclusion Gifts of Interests in Closely-Held Businesses • IRC 2503(b) • Must be “present interest” gift • “An unrestricted right to immediate use, possession or enjoyment of property or income from property …” Treas. Reg. § 25.2503-3(b)

Cases – Addressing Gifts of Business Interests • Hackl v. Commissioner, 118 T.C. 279 (2002), aff’d, 335 F.3d 664 (7th Cir. 2003) • Price v. Commissioner, T.C. Memo. 2010-2 (January 4, 2010) • Fisher v. U.S., 105 AFTR 2d 2010-1347 (DC IN) (March 11, 2010)

General Rule – Hackl Test • Donee right to immediate use, possession or enjoyment of property or income therefrom • That provides substantial economic benefit • Facts and circumstances • Governing documents critical

Right to Use Transferred Property • Outright ownership, alone, not present interest • Must essentially be able to convert to liquid asset

Right to Receive Income • Hackl test • Company generates income near time of gift • Portion flows steadily to donee • Income flow readily ascertainable

Take Aways • Review governing documents • Tie restrictions to strategy • Consider filing gift tax returns to report annual exclusion gifts

Challenges Unique to Farmers • Love of the Land • “Never sell the farm!!” • Equal is not Fair • Equity vs. Control • Communication among family members • Don’t assume all the kids want the farm or any part of it Jeanne SmithJ.D.

Challenges Unique to Vintners • ATF regulations on transfer of interests • Value of vines increases over time • May be more goodwill in valuation • Initially capital intense • Ancillary revenue sources and businesses

Equalizing Gifts Among Heirs • Separate the land and operations. 1. Create two classes of ownership • The class received by the active children would have managerial duties and would receive both a salary and a distribution from profits. • The other class would not have managerial duties and would not receive a salary, but would still receive a distribution from profits • 2. Create two LLC’s • The Farm Operations LLC will be distributed to the active farming children • The other LLC would own the farmland and lease it on a long term lease to the Farm Operations LLC

Techniques for Minimizing Disputes • In all cases prepare a Buy-Sell Agreement requiring the active children to buy out the passive children and vice-versa. • Puts and Calls • Long term buyouts to not jeopardize liquidity • Valuation with or without minority discounts

Techniques for Funding Estates Taxes • Irrevocable Life Insurance Trust • May be useful for meeting the estate tax burden of an estate composed of illiquid assets • May provide liquidity for buyouts

Techniques for Minimizing Estate Taxes • Conservation Easements • Allows land to be preserved, and provides an income tax deduction and estate tax reduction • Lifetime or testamentary

Team Approach for Planning • Attorneys for parents and children • CPA • Insurance Professional • Investment Advisor • Banker (lines of credit) • Experts

RESOURCES • Extension Service • University and College Family Business Programs (106) • Land Grant Schools • www.familybusinessonline.org – Austin Family Business Program at Oregon State University • Checklists • Ties to the Land • USDA (www.usda.gov)

CONTACT INFO Stan Miller: smiller@aristotle.net David Naples: david.naples@leonard.com Jeanne Smith: jsmith@smithlaworegon.com Orion Samuelson: bigosam@aol.com

THANK YOU! • Please rate today’s webcast and participatein a short survey. • Don’t forget to download materials immediately following this webcast, as live console access will end shortly. • The archived version of this webcast will be available on the WealthCounsel website within 24 hours.