Download

1 / 1

50 likes | 443 Views

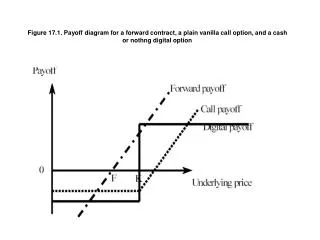

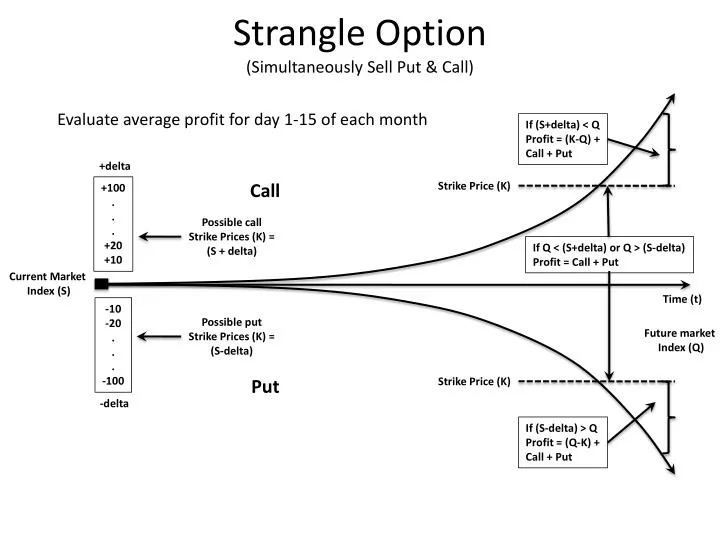

Strangle Option (Simultaneously Sell Put & Call). Evaluate average profit for day 1-15 of each month. If ( S+delta ) < Q Profit = (K-Q) + Call + Put. +delta. Strike Price (K). Call. +100 . . . +20 +10. Possible call Strike Prices (K) = (S + delta).

E N D

Strangle Option(Simultaneously Sell Put & Call) Evaluate average profit for day 1-15 of eachmonth If (S+delta) < Q Profit = (K-Q) + Call + Put +delta Strike Price (K) Call +100 . . . +20 +10 Possible call Strike Prices (K) = (S + delta) If Q < (S+delta) or Q > (S-delta) Profit = Call + Put Current Market Index (S) Time (t) -10 -20 . . . -100 Possible put Strike Prices (K) = (S-delta) Future market Index (Q) Put Strike Price (K) -delta If (S-delta) > Q Profit = (Q-K) + Call + Put