Download

1 / 8

80 likes | 99 Views

Explore alternative funding sources for single-family programs without bonds, addressing challenges and risks, with a focus on mortgage origination structures. Learn about non-bond mortgage origination programs and various risk structures.

E N D

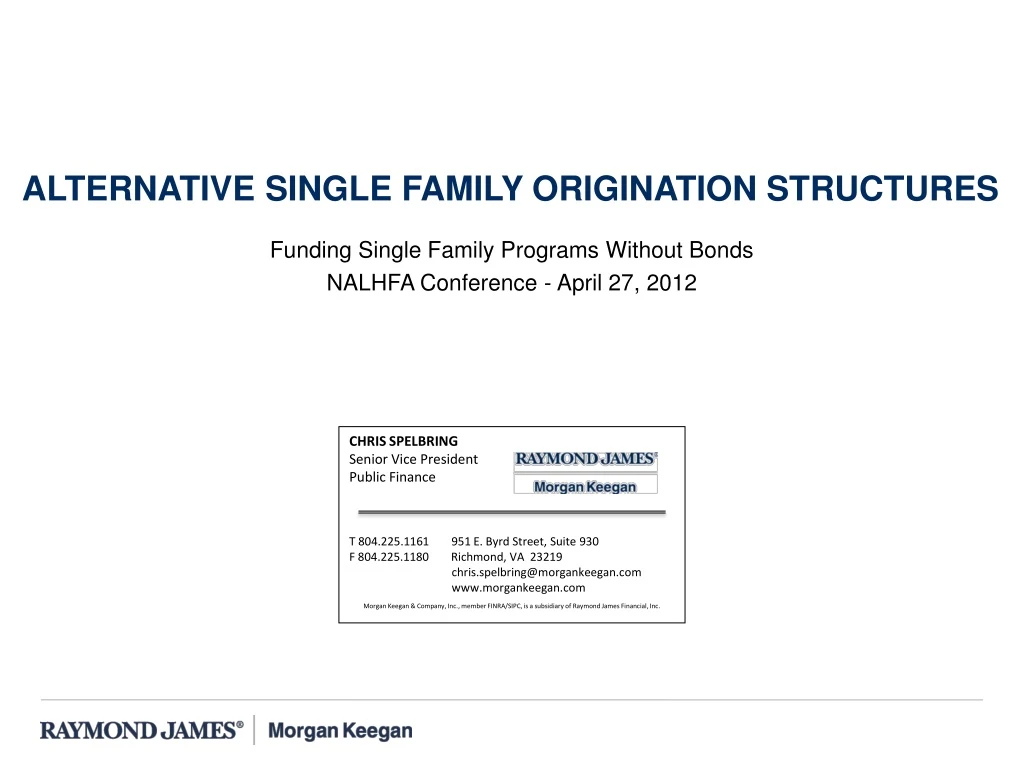

Funding Single Family Programs Without Bonds NALHFA Conference - April 27, 2012 Alternative single family origination structures CHRIS SPELBRING Senior Vice President Public Finance T 804.225.1161 951 E. Byrd Street, Suite 930 F 804.225.1180 Richmond, VA 23219 chris.spelbring@morgankeegan.com www.morgankeegan.com Morgan Keegan & Company, Inc., member FINRA/SIPC, is a subsidiary of Raymond James Financial, Inc.

NALHFA Conference – April 27, 2012 THE current environment Challenging Single Family Tax-Exempt Bond Structuring Market Still Exists • The tax-exempt housing bond market is healthier than a few years ago, but a number of market challenges that existed prior to implementation of NIBP continue to exist. • Challenging interest rate environment – tax-exempt bonds vs. taxable mortgage market. • Investor risk aversion continues to create high demand for U.S. Treasury Bonds and mortgage-backed securities (“MBS”) including GNMAs. • No or limited access to NIBP due to utilization of issuing authority. Marginalized benefits of any remaining NIBP funding. • Steep yield curve pressures housing bond transactions with negative arbitrage. • Need for a more competitive alternative funding source to tax-exempt bonds in order to implement a mortgage program.

NALHFA Conference – April 27, 2012 Alternative mortgage program Basics of a Non-Bond Mortgage Origination Program • HFAs can structure a market driven mortgage program that is very similar to mortgage programs funded by tax-exempt bonds with regard to the lender network, requirements to deliver mortgage loans to a mortgage servicer and the loan pooling process. • Until the MBS are pooled and set for delivery, the process is virtually identical to that of a typical single family bond program. The process includes: • Develop program guidelines • Secure a master servicer • Solicit and form a lender network • Select a mortgage rate and make it available to lenders/homebuyers • Lenders make mortgage loans to qualifying borrowers • Master servicer purchases loans from lenders and pools them into MBS • The primary difference between a bond funded structure and a market driven solution occurs when the MBS are ultimately delivered. Instead of being sold to a bond trustee and held as security for a bond transaction they are instead sold to a third party. The MBS sale can be (1) to settle a to-be-announced (“TBA”) contract used to hedge interest rate risk, (2) according to the predetermined terms of a contract with a third party or (3) to a third party in an open market transaction at the time of MBS delivery.

NALHFA Conference – April 27, 2012 Alternative Mortgage program Risks The Fundamental Risk of A Market Driven Program is Mortgage Loan/MBS Pricing • A bond program provides a committed level of funding at a cost of funds that is established at pricing. Effectively, an HFA has a perfect hedge for 100% of its mortgage production up the par amount of the bonds with the bond investor taking interest rate risk. • After structuring/pricing of a bond issue, an HFA knows that it will have a certain amount of funding to purchase MBS. Pricing is locked-in with a program mortgage rate in excess of the funding cost. • Unless an HFA implements the least risky strategy detailed herein, a non-bond funded mortgage program does not have committed funding. An HFA will be subject to adverse price movement on the mortgage loans that it has committed to purchase until the MBS are sold. • Risk related to a market driven mortgage program is simply the ability to generate sufficient proceeds from the sale of the MBS to fully reimburse the master servicer the agreed upon price for the MBS. • The risk is a product of the amount of time and pricing volatility that exists between the date that a mortgage loan reservation is made and when it is delivered to the HFA as part of an MBS (potentially months). • A loss will occur if the HFA sells the MBS at a price less than the purchase price of the MBS from the master servicer.

NALHFA Conference – April 27, 2012 alternative mortgage program structures Potential Structures Covering Spectrum of Risk • An HFA can choose to structure a non-bond funded mortgage program based on the level or risk that it is comfortable undertaking. Detailed below are three structuring variants that address different risk levels: • High Risk – HFA sets the mortgage rate and sells the MBS at the market price available when the MBS are delivered by the master servicer. Conceptually, an HFA can use NIBP and/or tax-exempt bond issuance authority as a hedge against severe adverse MBS pricing movement. Also, an HFA could set the mortgage rate extremely high to build in a cushion against adverse MBS pricing movement. • Moderate Risk – HFA secures a hedging consultant and a broker dealer to provide access to the TBA market. TBAs will be used to hedge against adverse MBS price movement. The TBA market allows the HFA to sell an unknown or to-be-announced MBS for delivery at a future date. TBAs eliminate interest rate risk but pipeline pullthrough and fallout risks remain. • Low (No) Risk – HFA enters into a contract with a third party who will purchase the MBS at predetermined prices. This option gives the HFA the ability to lock-in pricing. In this case, virtually all mortgage loan pipeline and MBS pricing risk is shifted to a third party. Raymond James | Morgan Keegan is one of a small number of firms to recently begin offering this “Turnkey” solution to state and local HFAs.

NALHFA Conference – April 27, 2012 alternative mortgage program Considerations What In-House Resources and Expertise are Available? • There are a number of questions that an HFA needs to address before determining if and which non-bond mortgage program should be implemented. Those questions include: • Am I willing to expose the HFA to the risk of financial loss? • Do I have the staff to implement and to monitor the program? • Do I have in-house interest rate/TBA hedging expertise? • Do I have relationships established with a master servicer, hedging consultant or a broker dealer? • Am I willing to forgo some level of profitability so that programmatic risks can be outsourced to another party?

NALHFA Conference – April 27, 2012 Programmatic flexibility More Flexible Eligibility Guidelines May Be Available • The program may allow for less restrictive first-time homebuyer, income and purchase price requirements given that these mortgage loans would not be financed with the proceeds of tax-exempt bonds. • HFAs will likely incorporate some homebuyer eligibility requirements in order to meet the goals of their organization even in the case of a non-bond funded mortgage lending program. There is added flexibility to expand the eligible homebuyer pool if the HFA incorporates less restrictive eligibility criteria than those funded by tax-exempt bonds. • Lenders will be ecstatic if the broader eligibility definitions reduce or eliminate the need for the compliance review and/or the related affidavits required under tax-exempt bond programs. • HFAs can allow homebuyers access to MCCs in conjunction with a non-bond funded mortgage platform. MCCs are not allowed in conjunction with a tax-exempt bond program.

disclaimer The information contained herein is solely intended to facilitate discussion of potentially applicable financing applications and is not intended to be a specific buy/sell recommendation, nor is it an official confirmation of terms. Any terms discussed herein are preliminary until confirmed in a definitive written agreement. While we believe that the outlined financial structure or marketing strategy is the best approach under the current market conditions, the market conditions at the time any proposed transaction is structured or sold may be different, which may require a different approach. The analysis or information presented herein is based upon hypothetical projections and/or past performance that have certain limitations. No representation is made that it is accurate or complete or that any results indicated will be achieved. In no way is past performance indicative of future results. Changes to any prices, levels, or assumptions contained herein may have a material impact on results. Any estimates or assumptions contained herein represent our best judgment as of the date indicated and are subject to change without notice. Examples are merely representative and are not meant to be all-inclusive. Raymond James | Morgan Keegan shall have no liability, contingent or otherwise, to the recipient hereof or to any third party, or any responsibility whatsoever, for the accuracy, correctness, timeliness, reliability or completeness of the data or formulae provided herein or for the performance of or any other aspect of the materials, structures and strategies presented herein. Raymond James | Morgan Keegan is neither acting as your financial advisor nor Municipal Advisor (as defined in Section 15B of the Exchange Act of 1934, as amended), and expressly disclaims any fiduciary duty to you in connection with the subject matter of this Presentation. Raymond James | Morgan Keegan does not provide accounting, tax or legal advice; however, you should be aware that any proposed transaction could have accounting, tax, legal or other implications that should be discussed with your advisors and/or legal counsel. Raymond James | Morgan Keegan and affiliates, and officers, directors and employees thereof, including individuals who may be involved in the preparation or presentation of this material, may from time to time have positions in, and buy or sell, the securities, derivatives (including options) or other financial products of entities mentioned herein. In addition, Raymond James | Morgan Keegan or affiliates thereof may have served as an underwriter or placement agent with respect to a public or private offering of securities by one or more of the entities referenced herein. This Presentation is not a binding commitment, obligation, or undertaking of Raymond James | Morgan Keegan. No obligation or liability with respect to any issuance or purchase of any Bonds or other securities described herein shall exist, nor shall any representations be deemed made, nor any reliance on any communications regarding the subject matter hereof be reasonable or justified unless and until (1) all necessary Raymond James | Morgan Keegan, rating agency or other third party approvals, as applicable, shall have been obtained, including, without limitation, any required Raymond James | Morgan Keegan senior management and credit committee approvals, (2) all of the terms and conditions of the documents pertaining to the subject transaction are agreed to by the parties thereto as evidenced by the execution and delivery of all such documents by all such parties, and (3) all conditions hereafter established by Raymond James | Morgan Keegan for closing of the transaction have been satisfied in our sole discretion. Until execution and delivery of all such definitive agreements, all parties shall have the absolute right to amend this Presentation and/or terminate all negotiations for any reason without liability therefor.