Download

1 / 39

390 likes | 527 Views

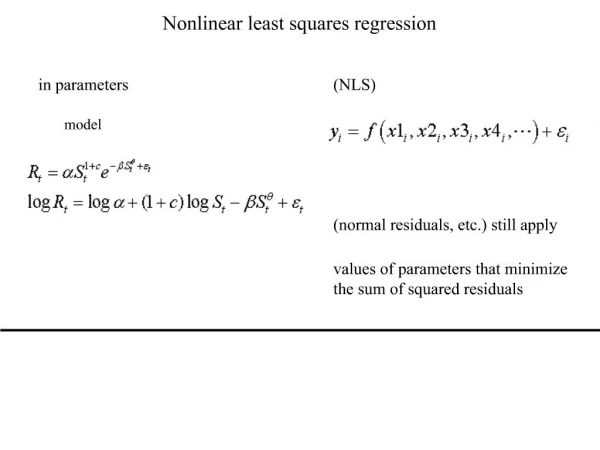

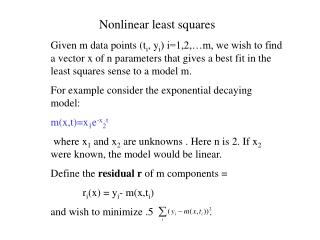

Methods For Nonlinear Least-Square Problems . Jinxiang Chai. Applications. Inverse kinematics Physically-based animation Data-driven motion synthesis Many other problems in graphics, vision, machine learning, robotics, etc. Where , i=1,…,m are given functions, and m>=n .

E N D

Methods For Nonlinear Least-Square Problems Jinxiang Chai

Applications • Inverse kinematics • Physically-based animation • Data-driven motion synthesis • Many other problems in graphics, vision, machine learning, robotics, etc.

Where , i=1,…,m are given functions, and m>=n Problem Definition Most optimization problem can be formulated as a nonlinear least squares problem

Base Inverse Kinematics Find the joint angles θ that minimizes the distance between the character position and user specified position θ2 θ2 l2 l1 θ1 C=(c1,c2) (0,0)

Global Minimum vs. Local Minimum • Finding the global minimum for nonlinear functions is very hard • Finding the local minimum is much easier

Assumptions • The cost function F is differentiable and so smooth that the following Taylor expansion is valid,

Gradient Descent Objective function: Which direction is optimal?

Gradient Descent Which direction is optimal?

Gradient Descent A first-order optimization algorithm. To find a local minimum of a function using gradient descent, one takes steps proportional to the negative of the gradient of the function at the current point.

Gradient Descent • Initialize k=0, choose x0 • While k<kmax

Newton’s Method • Quadratic approximation • What’s the minimum solution of the quadratic approximation

Newton’s Method • High dimensional case: • What’s the optimal direction?

Newton’s Method • Initialize k=0, choose x0 • While k<kmax

Newton’s Method • Finding the inverse of the Hessian matrix is often expensive • Approximation methods are often used - conjugate gradient method - quasi-newton method

Comparison • Newton’s method vs. Gradient descent

Gauss-Newton Methods • Often used to solve non-linear least squares problems. Define We have

Gauss-Newton Method • In general, we want to minimize a sum of squared function values

Gauss-Newton Method • In general, we want to minimize a sum of squared function values • Unlike Newton’s method, second derivatives are not required.

Gauss-Newton Method • In general, we want to minimize a sum of squared function values

Gauss-Newton Method • In general, we want to minimize a sum of squared function values Quadratic function

Gauss-Newton Method • In general, we want to minimize a sum of squared function values Quadratic function

Gauss-Newton Method • In general, we want to minimize a sum of squared function values Quadratic function

Gauss-Newton Method • In general, we want to minimize a sum of squared function values Quadratic function

Gauss-Newton Method • Initialize k=0, choose x0 • While k<kmax

Gauss-Newton Method • In general, we want to minimize a sum of squared function values Any Problem? Quadratic function

Gauss-Newton Method • In general, we want to minimize a sum of squared function values Any Problem? Quadratic function

Gauss-Newton Method • In general, we want to minimize a sum of squared function values Any Problem? Quadratic function Solution might not be unique!

Gauss-Newton Method • In general, we want to minimize a sum of squared function values Any Problem? Quadratic function Add regularization term!

Levenberg-Marquardt Method • In general, we want to minimize a sum of squared function values Any Problem?

Levenberg-Marquardt Method • In general, we want to minimize a sum of squared function values Any Problem? Quadratic function Add regularization term!

Levenberg-Marquardt Method • In general, we want to minimize a sum of squared function values Any Problem? Quadratic function Add regularization term!

Levenberg-Marquardt Method • Initialize k=0, choose x0 • While k<kmax

Stopping Criteria • Criterion 1: reach the number of iteration specified by the user K>kmax

Stopping Criteria • Criterion 1: reach the number of iteration specified by the user • Criterion 2: when the current function value is smaller than a user-specified threshold K>kmax F(xk)<σuser

Stopping Criteria • Criterion 1: reach the number of iteration specified by the user • Criterion 2: when the current function value is smaller than a user-specified threshold • Criterion 3: when the change of function value is smaller than a user specified threshold K>kmax F(xk)<σuser ||F(xk)-F(xk-1)||<εuser

Levmar Library • Implementation of the Levenberg-Marquardt algorithm • http://www.ics.forth.gr/~lourakis/levmar/

Constrained Nonlinear Optimization • Finding the minimum value while satisfying some constraints