Download

1 / 20

200 likes | 328 Views

XXVII Meeting of the Latin American Network of Central Banks and Finance Ministers. Creeping Inflation: How much of a concern? What should the Response be?. Paul Castillo Central Reserve Bank of Peru. InterAmerican Development Bank ,Washington DC, May 2008. Outline.

E N D

XXVII Meeting of the Latin American Network of Central Banks and Finance Ministers Creeping Inflation: How much of a concern? What should the Response be? Paul Castillo Central Reserve Bank of Peru InterAmerican Development Bank ,Washington DC, May 2008

Outline • Where is inflation comming from? • Should central Banks respond? • How the Central Bank of Peru is responding? • Final remarks

Where is inflation coming from? • In most countries inflation is coming from high food prices, triggered by the the sharp increase in commodities prices, such us oil, corn, wheat, and rice. • Changes in food prices seem to reflect a permanent relative price realigments. • Increasing demand from China and other fast-growing economies in Asia is an important factor behind the boom in commodity prices.

Should Central Banks Respond? • According to the literature, when inflation is generated by changes in relative prices of goods whose prices are not too sticky, like food, central banks should not respond, Aoki (2001). • In this case, the welfare cost of relative price realigments is relatively small but the cost of stabilization policy is much larger. • Therefore, central banks do better focusing on inflation of those goods whose prices are more sticky, like core inflation excluding food and energy.

Should Central Banks Respond? • No response at all, however, could trigger higher inflation expectations, particularly when there exist imperfect knowledge about the source of the shock. • Sargent et. at (2003) show how uncertainty on the costs of stabilizing inflation can lead to higher inflation if this type of uncertainty delays the response of the central bank. • The high inflation period of the 70’s is illustrative to this respect.

Should Central Banks Respond? • In the 70’s the FED did not increased the interest rate strongly enough to keep inflation expectations anchored, • Inflation expectations deviated and inflation increased above 15 %, • Then, a more restrictive monetary policy was requiered to put inflation back on track. • This policy was finally put in place by the administration of Paul Volcker.

Should Central Banks Respond? • On the other hand, a strong response to higher food prices doesn´t seems a good idea either, • It implies a costly adjustment in terms of output to induce a deflation on the other prices of the CPI.

What to do then? • The answer seems to be on a middle point, • Increase interest rates to prevent deviations on inflation expectations, • But not too much that could damage output growth rates and employment creation.

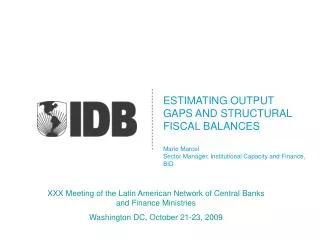

Central Banks have moved interest rates considering these two factors

What to do then? • Some of then, such as Bank of Canada, for instance, cut interest rates considering that the Subprime crisis in U.S.A, could damage output growth. • Others, like the Central Bank of Peru have raised interest rates considering that inflationary riks were higher and that the impact of subprime crisis on the Peruvian economy was not going to be to large.

In Peru, as in most countries inflation is explained by imported Inflation Domestic CPI Imported CPI CPI

However, it is accompanied by strong domestic demand March % January

In response, the central bank has increased its interest rate four times since July 2007ntación Discount rate Reference rate Deposit rate

This response aims at: • Keep inflation expectations anchored to the central bank inflation target. • Bring output growth down to its potential level to reduce upside inflation risks. • Aminorate the impact of food prices on other components of CPI inflation.

Somevulnerabilities, however, remainsuch as dollarization, but are beingreduced, Financial Dollarization Liabilities dollarization Asset dollarization

On average, however, inflation has been one of the lowest in Latin America(Average 2002-2007 Annual Variation %)

Final remarks • Relative price realigments seem to requiere some reacction from central banks, • This reaction should be strong enough to guide expectations, but not to large to generate a large cost in terms of output and unemployment.