Download

1 / 11

110 likes | 206 Views

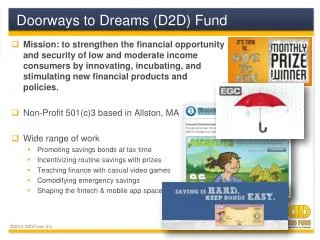

Using Financial Innovation to Support Savers: From Coercion to Excitement FDIC Committee on Economic Inclusion March 19, 2008. Peter Tufano Harvard Business School, D2D Fund, and NBER. Why this discussion?.

E N D

Using Financial Innovation to Support Savers: From Coercion to ExcitementFDIC Committee on Economic InclusionMarch 19, 2008 Peter TufanoHarvard Business School, D2D Fund, and NBER

Why this discussion? • Savings is important for families, both to achieve long-run goals and to withstand short-term shocks • A large fraction of households are asset-poor • People differ and no one solution will fit all • Array the full range of ways to support savings for low to moderate Americans

The continuum of programs Force Make Hard Make Easy Bribe Social Make Fun to Save Not to Save to Save to Save Support & Exciting

Force Make Hard Make Easy Bribe Social Make Fun to Save Not to Save to Save to Save Support & Exciting Force to Save

Force Make Hard Make Easy Bribe Social Make Fun to Save Not to Save to Save to Save Support & Exciting Make it hard NOT to save

Force Make Hard Make Easy Bribe Social Make Fun to Save Not to Save to Save to Save Support & Exciting Make it easier to save

Force Make Hard Make Easy Bribe Social Make Fun to Save Not to Save to Save to Save Support & Exciting Bribe to save

Force Make Hard Make Easy Bribe Social Make Fun to Save Not to Save to Save to Save Support & Exciting Support social savings

Force Make Hard Make Easy Bribe Social Make Fun to Save Not to Save to Save to Save Support & Exciting Make Savings Fun

Defaults: Auto-savings Bundling: Plus-savings Lowering barriers – tax refunds and nearly-auto save Lowering barriers—supporting “buying” savings with simpler retail processes and KYC rules Train to save—kid’s programs Social networks—gifting and supporting informal savings Exciting—prize based Encourage auto-save pilots Study and encourage broader use Help banks with split-refund IRA work; support indirect savings, support savings bonds Study modifications to KYC rules (e.g., two step process); help banks support non-bank programs Convening to focus attention Paradigm shifts: We vs. I savings; savings as gifts Study; explore how to make prize linked permissible What are promising low-cost opportunities? What can the FDIC do? OPPORTUNITY FDIC STEPS