Download

1 / 15

150 likes | 305 Views

5. Monetaristic Theories and the Phillips Curve. Exogenous shocks (mainly from Keynesian policy) Monetary amplifiers (v) Rules instead of discretion Flourished in 1970s and 1980s Today merged with new classical and Keynesian models.

E N D

5. Monetaristic Theories and the Phillips Curve • Exogenous shocks (mainly from Keynesian policy) • Monetary amplifiers (v) • Rules instead of discretion • Flourished in 1970s and 1980s • Today merged with new classical and Keynesian models Konjunktur und Beschäftigung U. van Suntum KuB 5.2 1 U van Suntum, Vorlesung KuB 1

A simple model following Friedman • Milton Friedman • 1912 - 2006 • Nobelprice 1976 Konjunktur und Beschäftigung U. van Suntum KuB 5.2 2 U van Suntum, Vorlesung KuB 2

Numerical example Shock in t1: M1 = M2...= Mn = 808 ... Konjunktur und Beschäftigung U. van Suntum KuB 5.2 3 U van Suntum, Vorlesung KuB 3

Graphical exposition of Friedman example Ynom (left hand scale) Price level p (right hand scale) P Konjunktur und Beschäftigung U. van Suntum KuB 5.2 4 U van Suntum, Vorlesung KuB 4

Graphical exposition of Friedman example (II) Inflation rate (righthandscale) Velocityofmoneycirculation v (lefthandscale) Konjunktur und Beschäftigung U. van Suntum KuB 5.2 5 U van Suntum, Vorlesung KuB 5

Criticism • real income fixed (missing equation) • constant Yreal empirically false • far too simple • but makes Hawtrey-effect more explicit • can serve as basis for more sophisticated models Konjunktur und Beschäftigung U. van Suntum KuB 5.2 6 U van Suntum, Vorlesung KuB 6

The model by Laidler (1973) Konjunktur und Beschäftigung U. van Suntum KuB 5.2 7 U van Suntum, Vorlesung KuB 7

Numerical example(a = 0,9 b = 0,4 Ymax = 100 CU* = 80%) Monetary shock in t =1 P CU Konjunktur und Beschäftigung U. van Suntum KuB 5.2 8 U van Suntum, Vorlesung KuB 8

Graficalexpositionoftheexample (curvesaresmoothed) ..\..\Makro\Vorlesung Makro WS 2009\monetaristisches Konj-Modell.xls Yreal (left hand scale) Price level p (right hand scale) P Konjunktur und Beschäftigung U. van Suntum KuB 5.2 9 U van Suntum, Vorlesung KuB 9

Graficalexpositionoftheexample (II) (curvesaresmoothed) Growth of Yreal Inflation rate Konjunktur und Beschäftigung U. van Suntum KuB 5.2 10 U van Suntum, Vorlesung KuB 10

Graficalexpositionoftheexample (III) (curves not smoothed) Capacity utilization CU Velocity of money circulation v Konjunktur und Beschäftigung U. van Suntum KuB 5.2 11 U van Suntum, Vorlesung KuB 11

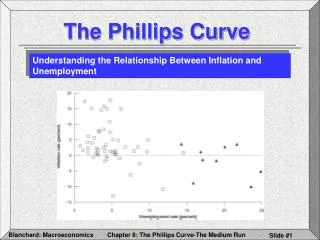

Phillipscurve in Laidler-model (I) Inflation rate 1 - CU Konjunktur und Beschäftigung U. van Suntum KuB 5.2 12 U van Suntum, Vorlesung KuB 12

Phillipscurve in Laidler-model (II) Inflation rate 1 - CU Konjunktur und Beschäftigung U. van Suntum KuB 5.2 13 U van Suntum, Vorlesung KuB 13

Strengths: Can explain short term impact of monetary policy Damped fluctuations in line with reality Can explain the short term Phillipscurve Clear policy recommendations Weaknesses: One sided Quantity of money exogenous? Missing equation in Friedman´s model Mechanistic behavior of P und Yreal in Laidler`s model Criticism of monetaristic models Konjunktur und Beschäftigung U. van Suntum KuB 5.2 14 U van Suntum, Vorlesung KuB 14

Lerning goals/questions • What are the key cycle drivers in monetaristic models? • How do these models explain the turning points? • How do the short run effects differ from the long run results? • How is the Phillips curve explained by monetaristic models? • What are the main policy recommendations from monetaristic models? Konjunktur und Beschäftigung U van Suntum, Vorlesung KuB 15