Download

1 / 28

280 likes | 392 Views

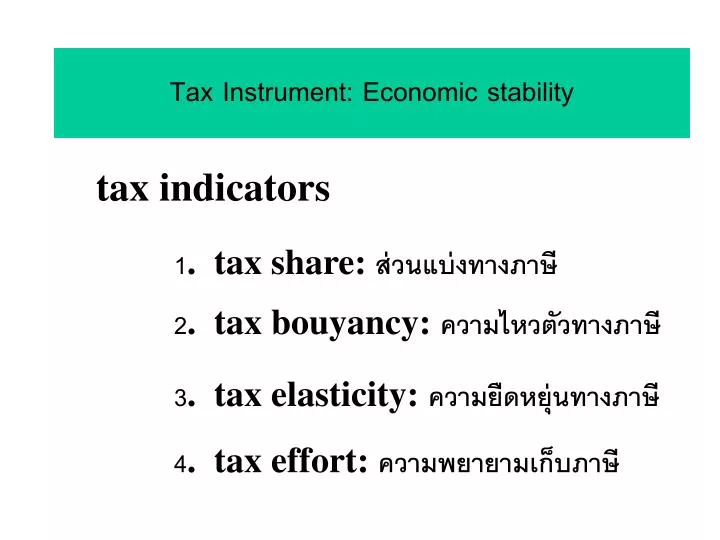

Tax Instrument: Economic stability. tax indicators. 1. tax share: ส่วนแบ่งทางภาษี. 2. tax bouyancy: ความไหวตัวทางภาษี. 3. tax elasticity: ความยืดหยุ่นทางภาษี. 4. tax effort: ความพยายามเก็บภาษี. วัตถุประสงค์ของการเก็บภาษีของรัฐบาล. เพื่อหารายได้. เพื่อลดปัญหา bad externalities.

E N D

Tax Instrument: Economic stability tax indicators 1. tax share: ส่วนแบ่งทางภาษี 2. tax bouyancy: ความไหวตัวทางภาษี 3. tax elasticity: ความยืดหยุ่นทางภาษี 4. tax effort: ความพยายามเก็บภาษี

วัตถุประสงค์ของการเก็บภาษีของรัฐบาลวัตถุประสงค์ของการเก็บภาษีของรัฐบาล เพื่อหารายได้ เพื่อลดปัญหา bad externalities เพื่อสนับสนุนการส่งออกและการเติบโต เพื่อป้องกันอุตสาหกรรมภายในประเทศ เพื่อการกระจายรายได้ให้เท่าเทียมกัน เพื่อรักษาสิ่งแวดล้อมและคุณภาพชีวิต เพื่อรักษาเสถียรภาพของระบบเศรษฐกิจ

ประวัติการเก็บภาษีและประเภทภาษีที่ควรพิจารณาประวัติการเก็บภาษีและประเภทภาษีที่ควรพิจารณา • ภาษีรักชาติ เงินช่วยชาติ • ภาษีประชาธิปไตย ภาษีเดินทางไปต่างประเทศ • ภาษีการศึกษา • แสตมป์เพื่อการศึกษาและการสาธาณสุข • ภาษีมรดก • ภาษีชายโสด

ส่วนแบ่งภาษี (Tax Share) Tax Ratio = tax revenue GDP Tax ratio ในปี 2540 = [757,400 / 4,732,600 ] x 100 = 16.00 %

การวัดขนาดของภาครัฐ 1. tax share 2. government expenditure share

สัดส่วนของภาษี รายจ่ายรัฐบาลต่อ GDPของประเทศไทย ปี 2531 - 2540 ปี พ.ศ. GDP Tax G T/GDP G/GDP

สัดส่วนของภาษี รายจ่ายรัฐบาลต่อ GDPของประเทศไทย ปี 2541 - 2544 ปี พ.ศ. GDP Tax G T/GDP G/GDP

Automatic Tax Stabilizers 1. tax buoyancy 2. tax elasticity

ส่วนประกอบของรายรับจากภาษีส่วนประกอบของรายรับจากภาษี ส่วนที่ 1: เกิดจากการเปลี่ยนแปลงโดยตัวมันเอง (autonomous tax revenues) ส่วนที่ 2: เกิดจากการเปลี่ยนแปลงของระบบภาษี (discretionary tax revenues) อัตราภาษี หรือ ฐานภาษี

การไหวตัวของภาษี (Tax Buoyancy) tb = %การเปลี่ยนแปลงของรายรับจากภาษี % การเปลี่ยนแปลงฐานภาษี (GDP) tb > 1 มีการไหวตัวมาก stability tb < 1 มีการไหวตัวน้อย

ความยืดหยุ่นทางภาษี (Tax Elasticity) te = %การเปลี่ยนแปลงของรายรับจากภาษีของตัวมันเอง % การเปลี่ยนแปลงฐานภาษี ( GDP) te > 1 มีการไหวตัวมาก stability te < 1 มีการไหวตัวน้อย

การคำนวณ tax function TRt = f ( GDPt, ut) TRt = a + b GDPt, + u lnTRt = a + blnGDPt, + u

การแยกภาษีอันเนื่องมาจากมาตรการทางภาษีการแยกภาษีอันเนื่องมาจากมาตรการทางภาษี TR = TA + TD total revenue autonomous revenue discrete revenue

รูปสมการภาษี 1. Traditional tax to income buoyancy and elasticity 2. Partition tax to income buoyancy and elasticity

Traditional Tax to Income Buoyancy and Elasticity Tax buoyancy: ln T = ln a + b ln GDP Tax elasticity: ln TA = ln c + d ln GDP

Partition Tax to Income Buoyancy and Elasticity Tax buoyancy: ln T = ln a + b ln B Tax elasticity: ln B = ln c + d ln GDP Tax buoyancy = (b) (d)

การขจัดผลทางภาษีอันเนื่องมาจากมาตรการทางภาษีการขจัดผลทางภาษีอันเนื่องมาจากมาตรการทางภาษี 1. Proportional Adjustment Method 2. Constant Rate Structure Method 3. Dummy Variable Method