Download

1 / 0

40 likes | 725 Views

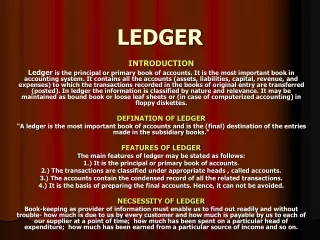

LEDGER. JOURNAL-LEDGER. Journal is a book of records where daily monetary transactions of a business is posted. Though it brings all the transactions together, it creates confusion between small and important expenses.

E N D