Download

1 / 18

190 likes | 388 Views

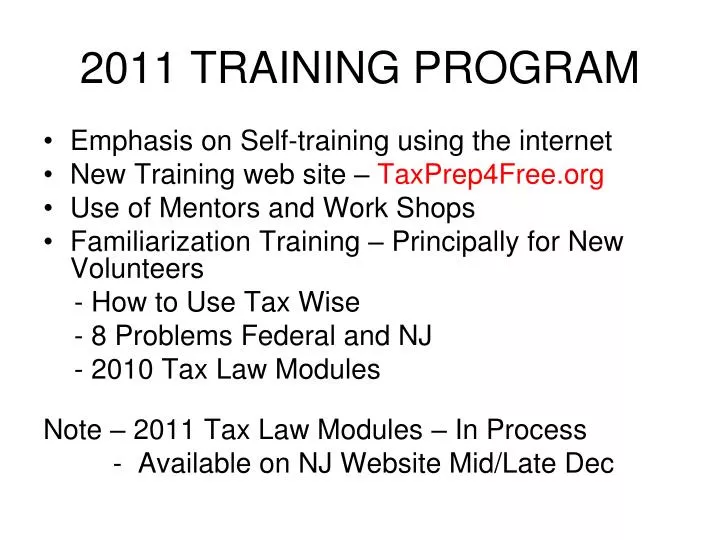

2011 TRAINING PROGRAM. Emphasis on Self-training using the internet New Training web site – TaxPrep4Free.org Use of Mentors and Work Shops Familiarization Training – Principally for New Volunteers - How to Use Tax Wise - 8 Problems Federal and NJ - 2010 Tax Law Modules

E N D

2011 TRAINING PROGRAM • Emphasis on Self-training using the internet • New Training web site – TaxPrep4Free.org • Use of Mentors and Work Shops • Familiarization Training – Principally for New Volunteers - How to Use Tax Wise - 8 Problems Federal and NJ - 2010 Tax Law Modules Note – 2011 Tax Law Modules – In Process - Available on NJ Website Mid/Late Dec

JANUARY, 2012 TRAINING TOPICS • What’s New, 2011 Tax Law and Tax Wise • Administrative topics • NJ Proficiency Problem – Review of Completed Problem • NJ Division of Taxation & IRS Presentations • Site Assignments

CERTIFICATION REQUIREMENTS (1) Four 4491-W Problems Complete and Review by Assigned Mentor by end of December New Volunteers – 2010 Problems with Refund Monitors Moore, Baylor, Fleming, Sterling TaxPrep4Free.org Training Proficiency

CERTIFICATION REQUIREMENTS Returning Volunteers 2011 Problems (from 2011 Pub 4491-W): Moore, Fleming, Sterling & Kent Refund monitors for Moore, Fleming, Sterling TaxPrep4Free.org Training What’s New for 2011 TY 2011 4491-W Refund Monitors Mentors will be assigned at this meeting

CERTIFICATION REQUIREMENTS (Cont’d) • 2011 IRS Test - Complete by Jan 12 • Includes Standards of Conduct test (New) for All Volunteers • Counselors must complete Basic, Intermediate and Advanced tests • Complete the test questions in Pub 6744 (some require preparation of a tax return) • Submit your answers • Enter your answers on-line (preferred) which will give you immediate feedback on your score. [On-line questions may be worded differently than Pub 6744]. Print your certificates. • Or, complete the answer sheet in Pub 6744 and give to Joe McFadden

CERTIFICATION REQUIREMENTS (Cont’d) • NJ Proficiency Exercise Problem Available on NJ Web Site by End of Dec. Complete Using NJ 2011 Software Available Early Jan. Due Date TBD To Be Reviewed/Discussed at Jan Meeting and/or Jan Work Shops

New Topics on IRS Test • Sale of securities (new form required) • Lump sum Social Security payments • Repayment of first-time homebuyers credit • Penalty on early withdrawal from retirement plans

SALE OF SECURITIES – 1099B • Revised 1099-B in 2011 • Brokers Must Report Cost, Date ofAcquisition, Long or Short Term for Covered Securities OR Indicate if Security is Uncovered Security • The only Covered Security for 2011 is Stock Acquired in 2011 (But Not Stock Acquired as Part of a DRIP) • But Brokers May Report Cost, etc for Sales of Stock Acquired before 2011 If Info is Available • Reporting of Cost, etc. for Uncovered Securities, Mutual Funds, Bonds, etc., Will Be Phased In Over Next 2 Years

CAPITAL GAINS WORKSHEET • The worksheet will populate Form 8949 Pg 1 (short term) and Pg 2 (long term): (A) Cost Basis Shown on 1099-B (Box 3) (B) Cost Basis Not Shown on 1099-B (C) No 1099-B Rec’d For Sale (Rare) • Sch D is populated with the totals

ADJUSTMENTS TO GAIN/LOSS • New Worksheet Also Provides For Adjusting Reported Gain/Loss On Sale • Column (b) - Insert Code to Indicate Type of Adj. Such As Exclude Gain on Home Sale or Incorrect 1099-B • Column (g) – Amount of Adj. to Reported Gain/Loss • NOTE – Codes for Types of Adj. are in Pub 4012, Tab 2, page 2-16

LUMP SUM SOCIAL SECURITY PAYMENTS • 2011 portion of lump sum goes on the bottom part of Social Security worksheet:

LUMP SUM SOCIAL SECURITY PAYMENTS (continued) • For the portions of lump sum from prior years, link to Lump-Sum Worksheet from “Amounts taxable from previous years” • See example in • TaxPrep4Free Training What’s New for 2011 Lump Sum Payments (in right margin)

REPAYMENT OF FIRST-TIME HOMEBUYERS CREDIT • Taxpayers who received First Time Homebuyers Credit in 2008 ($7,500) must repay Over 15 Years beginning in 2010.| - Another payment is due in 2011 • Use Form 5405 Page 2, Part IV as shown on the next page • Sale of home is out-of-scope

PENALTY ON EARLY WITHDRAWAL FROM RETIREMENT PLANS • Early Withdrawal From Qualified Retirement Plans Results in 10% Penalty (Code 1 in Box 7 of 1099-R) • If Exception Applies, Penalty Can Be Eliminated/Reduced on Form 5329, Part 1 • Record Amount of Exception and Related Code on Line 2 of Form 5329

COMMON EXCEPTIONS TO PENALTY FOR EARLY DISTRIBUTIONS • For Higher Education Expenses • Due to Total and Permanent Disability • For Unreimbursed Medical Expenses In Excess of 7.5% of AGI • To Unemployed Persons for Health Insurance Premiums • For Purchase of First Home - Up to $10,000 of Penalty • Error on 1099-R

2011 SPECIAL TOPICS - TRAINED VOLUNTEERS ONLY • Form 1099-Q, Qualified Education Distributions • Form 8606, Non-Deductible IRA Contributions/Distributions • Form 5405, Repayment of 2008 1st Time Homebuyers Credit • Form 5329 Part 1, Elimination of 10% Penalty On Early Withdrawal From Retirement Plans • Lump Sum Social Security payments • Part Year NJ Resident Tax Return • Foreclosure on Principal Residence and Cancellation of Debt (COD) - Must Pass Special IRS Test • Health Savings Accounts (HSA) – Must Pass Special IRS Test