Download

1 / 48

500 likes | 860 Views

Chapter 27 The Phillips Curve and Expectations Theory. Key Concepts Summary Practice Quiz Internet Exercises. ©2002 South-Western College Publishing. What is the Phillips Curve?. A curve showing an inverse relationship between the inflation rate and the unemployment rate.

E N D

Chapter 27The Phillips Curve and Expectations Theory • Key Concepts • Summary • Practice Quiz • Internet Exercises ©2002 South-Western College Publishing

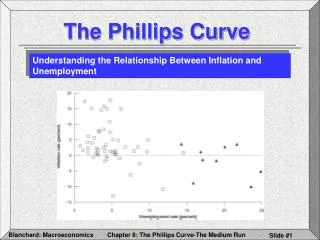

What is the Phillips Curve? A curve showing an inverse relationship between the inflation rate and the unemployment rate

Increase in Aggregate Demand AS 116 Price Level D 112 C AD4 108 B AD3 104 A full employment 100 AD2 AD1 Real GDP 5.8 6.0 6.2 6.4 6.6 6.8

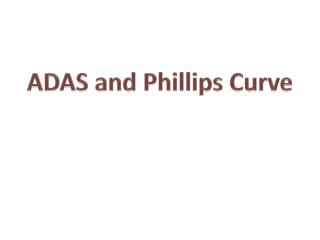

Movement along the Phillips Curve 16% D Phillips Curve 12% C 8% B Inflation Rate 4% A 0 Unemployment Rate 2% 4% 6% 8% 10% 12%

What is the conclusion of the Phillips Curve? The opportunity cost of more employment is more inflation and vice versa

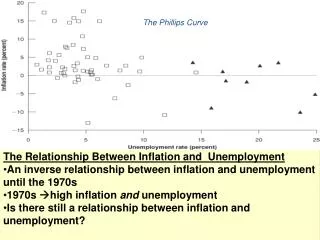

The Phillips Curve U.S., 1960’s 7% 6% 69 Inflation Rate 5% 4% 68 67 3% 60 64 66 2% 63 61 65 1% 62 Unemployment Rate 1% 2% 3% 5% 6% 7% 4%

The Phillips Curve U.S., 1970 - 1998 14% 80 13% 12% 79 11% 74 81 10% 75 9% 8% 78 Inflation Rate 7% 77 82 73 6% 76 90 70 84 5% 71 89 4% 88 85 87 83 72 3% 97 92 96 94 2% 86 98 1% 10% 1% 6% 9% 7% 8% 2% 3% 4% 5% Unemployment Rate

What does the long-run Phillips curve look like according to the Natural Rate Hypothesis? It is a vertical line at the natural rate of unemployment

The Short-run and Long-run Phillips Curves Long-run 15% G Inflation Rate F 12% Short-run Phillips curves D E 9% PC3 B C 6% PC2 natural rate A PC1 4% Unemployment Rate 10% 6% 8% 2% 4%

Short-run Adaptive Expectations Theory Unemployment rate rises Inflation rate rises, real wages fall, and profits rise Aggregate demand increases

Long-run Adaptive Expectations Theory Unemployment rate is restored to full employment Inflation rate is constant at higher rate, workers’ nominal wage rate rises, and profits fall

Inflation rate rises on vertical line at full employment Rational Expectations Theory Inflation rate rises and nominal wages adjust quickly equal to inflation rate Aggregate demand increases

What two versions of Expectations Theory explain the Natural Rate Model? Adaptive expectations Rational expectations

What is the Adaptive Expectations Theory? People believe the best indicator of the future is recent information

What is the conclusion of the Adaptive Theory? Expansionary monetary and fiscal policies to reduce unemployment are useless in the long-run

Why are monetary and fiscal polices useless in the long-run? After a short-run reduction in unemployment, the economy will self-correct to the natural rate of unemployment, but at a higher inflation rate

What is the Rational Expectations Theory? People will use all available information to predict the future, including future monetary and fiscal policies

What conclusion rational expectations? Systematic and predictable macroeconomic policies can be negated when businesses and workers anticipate the effects of these policies

According to the Rational Expectations Theory, can macroeconomic policies make things worse? People acting on their expectations of expansionary monetary and fiscal policies that are predictable can cause inflation

What happens if macroeconomic policies are not predictable? The economy’s self-correction mechanism will restore the economy to full employment

What is the best way to lower inflation? Preannounced, stable policies to achieve a low and constant money supply growth and a balanced federal budget

How can a distinction be made between the two theories? By analyzing the aggregate demand and supply model

Adaptive Expectations Theory LRAS E3 SRAS1 110 Price Level E2 105 AD2 E1 100 natural rate AD1 Real GDP 5.0 5.5 6.5 7.0 7.5 6.0

Rational Expectations Theory LRAS SRAS2 E3 SRAS1 110 Price Level 105 AD2 E1 100 natural rate AD1 Real GDP 5.0 5.5 6.5 7.0 7.5 6.0

What is an alternative way to fight inflation? Use incomes policies

What areincomes policies? Federal government policies designed to affect the real incomes of workers by controlling nominal wages and prices

What are examples of incomes policies? • Jawboning • Wage and price guidelines • Wage and price controls

What is jawboning? Oratory intended to pressure unions and businesses to reduce wage and price increases

What are wage and price guidelines? Voluntary standards set by the government for “permissible” wage and price increases

What are wage and price controls? Legal restrictions on wage and price increases. Violations can result in fines and imprisonment

Monetarism Monetarists see the cause of inflation as “too much money chasing too few goods,” based on the quantity of money theory (MV = PQ). To cure inflation, they would cut the money supply and force the Fed to stick to a fixed money supply growth rate. In the short run, the unemployment rate will rise, but in the long-run, it self-corrects to the natural rate.

Keynesianism Keynesians believe in using contractionary fiscal and monetary policies to cool an overheated economy. To decrease aggregate demand, they advocate that the government use tax hikes and/or spending cuts. The Fed should reduce the money supply and cause the rate of interest to rise. The opportunity cost of reducing inflation is greater unemployment.

Supply-Side Economics Supply-siders view the cause of inflation as “not enough goods.” Their approach is to increase aggregate supply by cuts in marginal tax rates. Government regulations, and import barriers. The effect provides incentives to work, invest, and expand production capacity. Thus, both the inflation rate and the unemployment rate fall.

New Classical School The theory of rational expectations asserts that the public must be convinced that policy-makers will stick to restrictive and persistent fiscal and monetary policies. If policy-makers have credibility, the inflation rate will be anticipated and quickly fall without a rise in unemployment.

Key Concepts • What is the Phillips Curve? • What is the conclusion of the Phillips Curve? • What two versions of Expectations Theory explain the Natural Rate Model? • What is the Adaptive Expectations Theory? • What is the Rational Expectations Theory?

Key Concepts cont. • How can a distinction be made between the two theories? • What are incomes policies? • What are examples of incomes policies? • What is jawboning? • What are wage and price guidelines? • What are wage and price controls?

The Phillips curve shows a stable inverse relationship between the inflation rate and the unemployment rate. If policy-makers reduce inflation, unemployment increases, and vice versa. During the 1960s, the curve closely fitted inflation and unemployment rates in the United States. Since 1970, the Phillips curve has not conformed to the stable inflation-unemployment trade-off pattern of the 1960s .

The natural rate hypothesis argues that the economy self-corrects to the natural rate of unemployment. Over time, changes in the rate of inflation are fully anticipated, and prices and wages rise or fall proportionately. As a result, the long-run Phillips curve is a vertical line at the natural rate of unemployment. Thus, Keynesian demand-management policies ultimately cause only higher or lower inflation, and the natural rate of unemployment remains unchanged.

Adaptive expectations theory is the proposition that people base their forecasts on recent past information, rather than future information. Once the government causes the inflation rate to rise or fall, people adapt their inflationary expectations to the current inflation rate. The result is a short-run Phillips curve that intersects the vertical long-run Phillips curve. Over time, the economy self-corrects to the natural rate of unemployment.

The political business cycle is a business cycle is created by the incentive for politicians to manipulate the economy to get re-elected. Using expansionary policies, officeholders can stimulate the economy before the election. Unemployment falls, and the price level rises. After the election, the strategy is to contract the economy to fight inflation and unemployment rises.

Rational expectations theory argues that it is naïve to believe that people change their inflationary expectations based only on the current inflation rate. Rational expectationists belong to the new classical school.

The rational expectation theory is based on people’s expectations. For example, if government policies are predictable, people immediately anticipate higher or lower inflation. Workers quickly change their nominal wages as businesses change prices. Consequently, inflation worsens or improves, and unemployment remains unchanged at the natural rate. Thus, there is no short-run Phillips curve, and the long-run Phillips curve is vertical

Incomes policies are a variety of federal government programs aimed at directly controlling wages and prices. Incomes policies include jawboning, wage-price guidelines, and wage-price controls. Over time, incomes policies tend to be ineffective.

Wage and price controls are legal restrictions on wages and prices. Most economists do not favor wage and price controls in peacetime. Such controls are expensive to administer, destroy efficiency, and intrude on economic freedom.