Download

1 / 38

380 likes | 560 Views

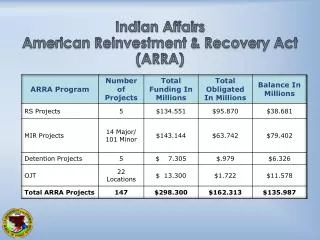

American Recovery & Reinvestment Act (ARRA) May 15, 2009 1:30 p.m. http://www.isbe.net/arra/default.htm. School Business Services DEB VESPA Division Administrator (217-785-8779) dvespa@isbe.net. Historic, one-time investment to stimulate economy & improve education

E N D

American Recovery & Reinvestment Act (ARRA) May 15, 2009 1:30 p.m.http://www.isbe.net/arra/default.htm

School Business Services DEB VESPA Division Administrator (217-785-8779) dvespa@isbe.net

Historic, one-time investment to stimulate economy & improve education Effective with the second General State Aid payment in April 2009, ARRA funds were distributed to school districts

Definitions ARRA – “American Recovery and Reinvestment Act of 2009” SFSF Program – State Fiscal Stabilization Fund Program (ARRA General State Aid) ARRA – Title I Funds ARRA – IDEA Funds ARRA Capital Projects: Qualified School Construction Bonds (QSCB) Qualified Zone Academy Bonds (QZAB) Build America Bonds (BAB)

Payment of ARRA GSA Funds ISBE will be using SFSF funds to pay the final GSA payments in FY 2009 It is anticipated that the SFSF funds will be utilized to pay for approximately five GSA payments in FY 2010 All districts should have submitted an application and assurance statement for the ARRA-GSA funds by April 17, 2009 Districts will be required to report on the estimated number of jobs saved and/or created by SFSF funds. Guidance will be forthcoming Districts will be required to track and report on expenditures paid with ARRA funds

Application and Assurance Statement Districts are to administer and use the SFSF program funds in accordance with all applicable statutes, regulations, and applications Recipients cannot use SFSF funds for: Payment of maintenance costs; Stadiums or other facilities used for athletic contests, exhibitions or other events for which admission is charged to the general public; Purchase or upgrade of vehicles; Improvements of stand-alone facilities whose purpose is not the education of children – such as central office administrative buildings; Financial assistance to students to attend private elementary or secondary schools unless the funds are used to provide special education and related services to children with disabilities as authorized by the IDEA Act; School modernization, renovation, or repair that is inconsistent with State Law.

Emergency Accounting Rules Because of the tracking necessary for ARRA federal funds, emergency accounting rules were necessary to: Designate ARRA revenue districts receive Document ARRA expenditures paid via each type of ARRA revenue source

ISBE Emergency Rules Accounting Requirements for ARRA Revenues and Expenditures Emergency Rules and Regulations have been posted for accounting requirements and are located at: http://www.isbe.net/rules/archive/pdfs/23IAC100EmergAmnd_Code.pdf

New Rules are available here for viewing Rules can also be found at www.isbe.net, click on “rules”

ISBE Emergency Rules ARRA GSA funds received should have a revenue account/source code of 4850 and may be deposited into any fund except Working Cash Other NEW ARRA revenue account codes: 4851 – 4855 Title I Low Income; Neglect, Private; Delinquent, Private; School Improvement (Part A); School Improvement (Part G) 4856 – 4857 IDEA Part B, Preschool; IDEA Part B, Flow-Through 10

ISBE Emergency Rules Other NEW ARRA revenue account codes (cont.): 4860 – 4861 Title IID, Technology-Formula; Title IID, Technology-Competitive 4862 – McKinney-Vento Homeless Education 4863 – Child Nutrition Equipment Assistance 4864 – 4865 Impact Aid Formula Grants and Impact Aid Competitive Grants 4866 – 4869 QZAB Tax Credits, QSCB Credits, BAB Tax Credits, and BAB Interest Reimbursement 4870 – 4880 Designated for other ARRA revenues and must be specified These can be located in Table C of the Emergency Rules 11

ISBE Emergency Rules • ARRA Expenditures must reflect Fund, Function, Object, and now a NEW fourth dimension -- revenue account code FundFunctionObjectRevenue Source Code XX XXXX XXX XXXX 01 1100 100 4850

ISBE Emergency Rules All funds must be expended in accordance to their respective purposes as authorized by the relevant federal law, regulation, and guidance In order to comply with the federal regulations, each district receiving funds under ARRA shall include in its annual financial report (AFR) a detailed schedule of its receipts and expenditures for each revenue source received Districts will need their auditors to audit the detailed schedule of receipts and expenditures Districts may now be required to have an A-133 Single Audit conducted. They should inquire with their auditor if this will be necessary for the audit of their Fiscal Year 2009 and if their auditor meets the necessary criteria to conduct A-133 audits 13

ISBE Emergency Rules A-133 Audit is required if: District expends $500,000 or more in total federal funds for a fiscal year This also includes the last five payments of the districts’ GSA as these are now considered federal funds ISBE is anticipating approximately 200 additional districts will now be required to have an A-133 audit Districts should be checking with their auditors to determine if they will need an A-133 audit and if their auditors qualify to conduct such an audit 14

Accumulated Interest Since the ARRA GSA payments are considered federal funds, ISBE is asking for guidance as to whether these funds can accumulate interest. Until this guidance is received, it is recommended that districts reflect ARRA GSA revenues were used to pay for allowable expenditures and reflect local revenue as invested. 15

ISBE Emergency Rules Fiscal Year 2009 Issues Districts may be required to amend their budgets Budgets – To Amend or Not?? If a district is expending ARRA funds in FY 2009 and these expenditures are not budgeted in the current budget, a budget amendment will be necessary If a district is expending ARRA funds in FY 2009 and the total expenditures in any fund is more than their current budget, a budget amendment will be necessary If a district is expending just ARRA GSA, most probably the expenditures are already budgeted, the total expenditures in any fund will not increase and a budget amendment will not be necessary If a district is expending ARRA Title I, ARRA IDEA, etc. most probably the expenditures are not budget, the total expenditures will increase and a budget amendment will be necessary – this includes flow-through funds from a special education cooperative 16

ISBE Emergency Rules For Fiscal Years 2010 and 2011 For FY 2010 and 2011 Budgets Districts will be required to document expenditures with fund, function, object, and revenue account code for ARRA expenditures within their detailed ledger reports ISBE budget is not expected to change as ISBE does not collect expenditures to the fourth dimension – “revenue account code” For FY 2010 and 2011 AFR The 2010 and 2011 AFR will include the ARRA schedule of receipts and expenditures to document revenue and expenditures of ARRA funds The schedule is part of the district’s audit An A-133 Single Audit may be necessary 17

ISBE Emergency Rules For Fiscal Year 2012 For FY 2012 Budget Districts will be required to document expenditures with fund, function, object, and revenue account code for ARRA expenditures within their detailed ledger reports as ARRA Funds can be obligated and expended through September 2011. ISBE budget is not expected to change as ISBE does not collect expenditures to the fourth dimension – “revenue account code” For FY 2012 AFR The 2012 AFR will include the ARRA schedule of receipts and expenditures to document revenue and expenditures of ARRA funds The schedule is part of the district’s audit An A-133 Single Audit may be necessary 18

Bond Options • Qualified Zone Academy Bonds (QZAB) • Were first authorized in 1997 by amendment of the Internal Revenue Code of 1986. The governing language explicitly designates ‘state education agencies’ as the authority to allocate the individual state volume caps. • Each calendar year, beginning with 1998 the national volume cap (the amount of bonds that can be so designated nationally for QZAB purposes) was $400 million and allocated among the states based upon poverty counts. With the ARRA, the national volume cap was increased to $1.4 billion for each of calendar years 2009 and 2010. To qualify for an allocation by the state education agency (ISBE in the case of ILL) there are curriculum design requirements, eligibility requirements, and a private business contribution requirement. The bonds issued can be used for repairs, renovations, curriculum development, or teacher training relative to a ‘Zone Academy’, but cannot be used for new construction.

Bond Options • Qualified School Construction Bonds (QSCB) • QSCB is a new designation for bonds authorized for the first time through the ARRA. The national volume caps are $11 billion for each of 2009 and 2010. The legislation is an amendment to the Internal Revenue Code of 1986. Unlike QZAB’s, virtually any school district or joint agreement is eligible to apply and receive an allocation from the ‘State’. • After receiving an allocation of the state’s volume cap, an issuing district designating a bond issue or part of a bond issue as QSCB’s would make principal payments on the bonds, but the bond holders would receive federal income tax credits in lieu of interest payments. The proceeds of such bonds can be used for new construction as well as repairs, renovations, etc.

Bond Options • Build America Bonds (BAB) • Build America Bonds (BAB’s) are also tax credit bonds, but they are taxable bonds rather than tax-exempt bonds, and they are not subject to a national or state volume cap. Any school district or joint agreement issuing bonds for construction type purposes can choose to designate the issue or part of the issue as BAB’s. There are then two options. One option involves paying taxable interest equal to 65% of the interest due to the bond holders and filing paperwork with the IRS such that the bond holder is eligible to claim the remaining 35% of the interest due as a tax credit. Under the other option, the district would pay the full amount of interest due on the bonds and then file a form with the IRS to receive a reimbursement check from the IRS equal to 35% of the interest paid.

Bond Options Specific guidance on these bond programs is available from the IRS at the following web address: http://www.irs.gov/newsroom/article/0,,id=206044,00.html Applications are being developed, watch Superintendent’s Weekly Message and ISBE website at:http://www.isbe.net/construction/html/qzab.htm

Funding & Disbursement Services LARRY SMITH Principal Consultant (217-782-5256) ismith@isbe.net

ARRA funds may lead to additional audit requirements • A-133 audits are required for entities with Federal • expenditures of $500,000 or more from all sources • (direct and indirect) • ARRA funds are Federal and must be included in • determining if entity meets $500,000 threshold • Many districts/joint agreements previously exempt • may now be required to have an A-133 audit • http://www.isbe.net/funding/pdf/potential_A133_audits.pdf

AUDITOR REQUIREMENTS – GOVERNMENT AUDITING STANDARDS Auditors performing school district audits and A-133 audits must meet requirements under Government Auditing Standards: Meet appropriate state licensing requirements Are independent from personal, external and organizational impairments Have a record of responsible work Have received a positive external quality control (peer) review within the last three years Submit the peer review report and acceptance letter to ISBE Have adequate qualifications, including experience with the type of entity being audited Have completed required continuing professional education Have not been suspended or debarred from performing government audits Have not been the object of any disciplinary action during the past three years http://www.isbe.net/funding/pdf/audit_qualifications.pdf

ARRA Funds – Auditor Requirements - Peer Review Each audit organization should have an appropriate internal quality control system in place and undergo an external quality control review (peer review). Government Auditing Standards requires any CPA firm that performs governmental audits to have a quality control review once every three years by an organization not affiliated with their firm.

ARRA Funds - Requirements for Auditors • CPA firms that perform school district audits must be qualified under Government Auditing Standards per ISBE rules; if the firm is qualified under Government Auditing Standards, it should be qualified to do an A-133 audit • A-133 audits submitted using a non-qualified auditor may be rejected by ISBE • Additional information on A-133 audits and requirements for CPA firms performing A-133 audits is available at: • http://www.isbe.net/funding/html/a133.htm http://www.isbe.net/funding/pdf/audit_qualifications.pdf

How much Federal aid did we receive?http://www.isbe.net/funding/pdf/FRISfederalconfweb.pdf

SEFA – List Subrecipients of ARRA Funds Of the Federal Awards received by XXXX, the following grant amounts were provided to subrecipients:

Funding and Disbursement Serviceshttp://www.isbe.net/funding/default.htm (217) 782-5256

ISBE continues to get guidance from the USDE. Please watch our website at http://www.isbe.net/arra/default.htmand the Superintendent’s Weekly Message for updated guidelines on ARRA funds. We will be passing this guidance on to you as we received it.

ARRA Resources ISBE ARRA Webpage: http://www.isbe.net/arra/default.htm Illinois ARRA Webpage: http://www.illinois.gov/recovery/ ED ARRA webpage: http://www.ed.gov/policy/gen/leg/recovery/index.html

At www.isbe.net, click here to receive more information on ARRA Funds At www.isbe.net, click here to review the Superintendent’s Weekly Messages and archived messages