Download

1 / 28

280 likes | 449 Views

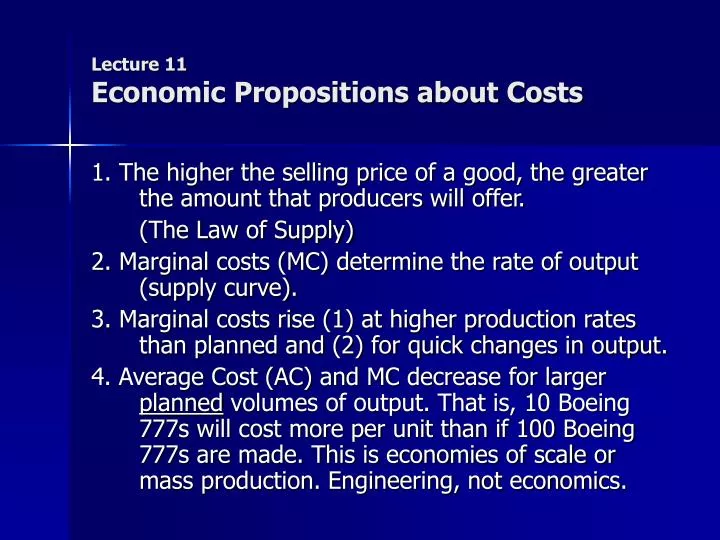

Lecture 11 Economic Propositions about Costs. 1. The higher the selling price of a good, the greater the amount that producers will offer. (The Law of Supply) 2. Marginal costs (MC) determine the rate of output (supply curve).

E N D

Lecture 11Economic Propositions about Costs 1. The higher the selling price of a good, the greater the amount that producers will offer. (The Law of Supply) 2. Marginal costs (MC) determine the rate of output (supply curve). 3. Marginal costs rise (1) at higher production rates than planned and (2) for quick changes in output. 4. Average Cost (AC) and MC decrease for larger planned volumes of output. That is, 10 Boeing 777s will cost more per unit than if 100 Boeing 777s are made. This is economies of scale or mass production. Engineering, not economics.

More economic propositions on costs 5. Money prices are measures of costs because the buyer must pay at least the value of the resources to their current owners—opportunity costs. All costs are opportunity costs. 7. Implicit costs exist even if no accounting expenditure is recorded for a good or service. 8. Cost and revenue should be calculated in terms of present value.

Present Value Example • You can buy a membership in the Executive Room at airports from an airline for $125 per year or $300 now for a 3 year membership. You know you will use it all three years. • Should you buy the 3 year membership?

It Depends • It depends on the interest (discount) rate. If the interest rate is 5%, buy the 3 year membership: PV = $125 + $125/1.05 + $125/(1.05)(1.05) $357.43 = $125 + $119.05 + $113.38 vs. $300 now (savings is $57.43 not $75) What if interest rate is 20%?

Discount or Interest Rates • Discount rates always exist whether we calculate them or not. • Money today is always more valuable than a promise of money in the future. • Paying tomorrow is preferred to paying today. • This is the time value of money that represents its opportunity cost.

Simple Example of Underestimation of Cost A software company has total revenue of 1,000,000 RMB. Total expenses of 850,000 RMB. Owner pays herself 100,000 RMB. Accounting profit: 50,000 RMB. But, the owner could earn 200,000 RMB if working for another software company. The opportunity cost of her labor is 200,000, not 100,000. Real cost of labor is 200,000, not 100,000, so firm lost 50,000 RMB. Is she crazy to work for herself?

Example of Cost Considerations Suppose you buy a truck for a business for 40,000. What is the cost today of acquiring this asset? Consider your alternatives and your plans for the vehicle right after purchase. The decision to buy the truck involves avoidable costs—by not buying the truck, you avoid costs. You buy the truck, the next day you decide it is a mistake and want to sell it. The value is now 37,000, so the cost is 3,000. That cost is “sunk cost.” It cannot be recovered and is unavoidable at this point to the decision made to keep or sell.

Possession Costs Next: You plan to keep the truck for two years. If you do not use it (just hold it), the value falls to 25,000 by then (from its current value of 37,000). But 25,000 in two years is not the same as the value today — it must be discounted to current value. If the discount rate is 10% per year then 25,000 x .826 = 20,650 present value. 37,000 - 20,650 = 16,350 depreciation (the anticipated decline in value of an asset)

Other possession costs If you hold the truck, at the beginning of each year you must pay license and insurance of 2,000 each year at the start of the year. So you pay 2,000 now. The beginning of next year you pay 2,000: covert that to present value .909 x 2,000 = 1,818 for two year total of 3,818. Add that to the holding cost to get two year holding total 3,818 + 16,350 = 20,168

Operating costs Suppose you use the truck 20,000 miles a year for each of two years. What costs? Depreciation increases, since the expected value of the truck after two years will be 22,000 (not 25,000) due to the mileage. Present value of 3,000 added depreciation (x .826) = 2,487 (Note that these may be called incremental or variable costs)

Operating Costs Suppose the out-of-pocket expenses for fuel, oil, repairs, and tires equals 5,000 the end of year one, 5,000 x .909 = 4,545; the present value if the bills are paid at the end of the year. And 7,000 in year two, paid at the end of year two: 7,000 x .826 = 5,782 For a two year present value total of 10,327. Add to that extra depreciation, 2,487 for a two year operating cost of 12,814.

Total Cost of Using Truck • The expected cost of the decision to own and use the truck for two years is: Acquisition cost: 3,000 Possession costs: 20,168 Operating costs: 12,814 Total present value of cost of obtaining the truck and using it: 35,982

Suppose Things Change? • The best plans can be upset by changes in technology. • What was “state of the art” becomes obsolete. • Obsolescence is an unanticipated development that reduces the value of existing assets.

Obsolescence and Cost • A machine costs £100,000 • It is expected to help produce 10,000 units of output before it is depreciated to nothing. If so, then there is a fixed cost of £10 per unit spread over the units. • Assume other costs (labor and supplies) are £20 per unit. • Output costs £30 per unit.

Obsolescence and Cost… • Now a new and better machine comes on the market. It costs £100,000 also. It is expected to produce 10,000 units before it is out of service. A fixed cost of £10 per unit. • However, it needs only £15 worth of labor and supplies • Cost per unit output is £25, not £30. • What is the value of the old machine?

Considerations • The old machine falls in value due to unexpected obsolescence. Even if old machine has never been used, the new machine causes the present value of the old machine to fall by £50,000 in value. • The old machine can be used so long as the price of output is above £20, so variable costs are covered. If price below £20, stop production.

Effects of Obsolescence Old Machine:New Machine: Fixed Cost £10 Fixed Cost £10 Variable Cost £20 Variable Cost £15 Total cost: £30/unit Total cost: £25/unit Market price for output £27. What do we do? Market price for output £22. What do we do? Market price for output £18. What do we do? Market price for output £13. What do we do?

Small (Marginal) Changes in Cost Add Up • Most managerial decisions involve cost changes at the margin—small changes that can have big impacts. • Starbucks, studying worker time in production, noticed that employees had to dig twice into ice machines to get sufficient ice for large drinks. The developed a new ice scoop that requires one scoop for any size drink. Time savings of 14 seconds for large drinks. • Working on such margins for 5 years reduced average waiting time from 3.5 minutes to 3 minutes per customer.

Small Changes Can Mean Higher Profits • Over five years, such improvements in productivity at Starbucks (shorter waiting time for customers, so more sales) meant store sales up an average of $200,000. • Wendy’s developed a double-sided grill that cuts cooking time for a hamburger patty from 5 minutes to 1.5 minutes. • Caribou Coffee uses “floater” workers who are not assigned to one task but help direct others to where need is greatest and jumps in to help where help is needed. Added cost of one worker less than added revenue from faster productivity (more sales).

Opportunity Costs • “Few firms make a profit.” Peter Drucker Why? Most focus on accounting costs, failing to consider opportunity costs, so constantly overestimate profits.

Opportunity Cost: A Real World Issue • Why has there been a push to “just in time inventory” in production? • Even if debt collection from customers is certain to happen, why is sooner better than later? • If a firm is profitable, how do you account for the value of the money used to buy machinery (assets)?

Example: John Deere • Tough competition in heavy equipment market. • New CEO focused on reducing all costs: • Sold and leased excess plant space (capitalized an undervalued asset) • Reduced end of year unsold combines from 1,600 in 2000 to 200 in 2005 (value of unsold inventory reduced $1/3 billion—opportunity cost of cash)

How one firm accounts for opportunity cost: • Gillette requires each division to count the opportunity cost of cash tied up in different parts of the operation. • Example: one division showed accounting revenues of $1,069 million and costs of $1,001 million, for an accounting profit of $68 million. • Division was required to count the opportunity cost of cash, which changed the results. Previously, the division had less incentive to consider the value of cash used or idled.

Measuring Opportunity Cost • The rule is that 12% interest is charged by the parent company to each division for idle cash: • Average inventory in stock: 242 days • Average time for debt collection, 105 days • Cash tied up in equipment Opportunity cost of this: $119 million. Now: $68 million accounting profit minus $119 cost of cash yields $51 million loss. Managers told to reform or division would be liquidated.

Reducing Opportunity Cost within the Firm • Steps taken to reduce those costs: • Outsource debt collection to specialist firm. Average debt collection time reduced from 105 to 41 days over 5 years. • Average inventory time cut from 242 to 198 days over five years. • New applications for existing production machinery devised to increase revenue from equipment (also new revenue source). Net result: These opportunity costs cut $35 million. The division treated cash as a free good from the parent company.

Accounting Costs Lead Managers Over the Cliff Accounting numbers are very important management tools. But they can never account for all opportunity costs. Managers must see these within their own organization. Sometimes managers focus on accounting numbers only and drive the firm into bankruptcy.

Impact of One Change in Accounting Cost Rules FASB (U.S.) and International Accounting Standards Board intend to change the rule for long-term leases. It will mean about $1 trillion in “new” costs being recognized on the books. Long-term leases (like pension obligations) are often hidden. Some retailers do not own stores, they have long leases. Example: Whole Foods reported $639 million in long-term liabilities for 2006. Include lease obligations and that rises to $4.8 billion, reducing return on assets from 7.2% to 3.7% and increasing debt/equity ratio from 38% to 169%.

Summary: Costs • The economic way of thinking about costs is not the same as accounting costs or the common way people think of costs. • This helps us consider opportunity costs —what does it cost us to command resources for some purpose — so we can contrast it to our next best understood alternative.