Download

1 / 107

1.09k likes | 1.32k Views

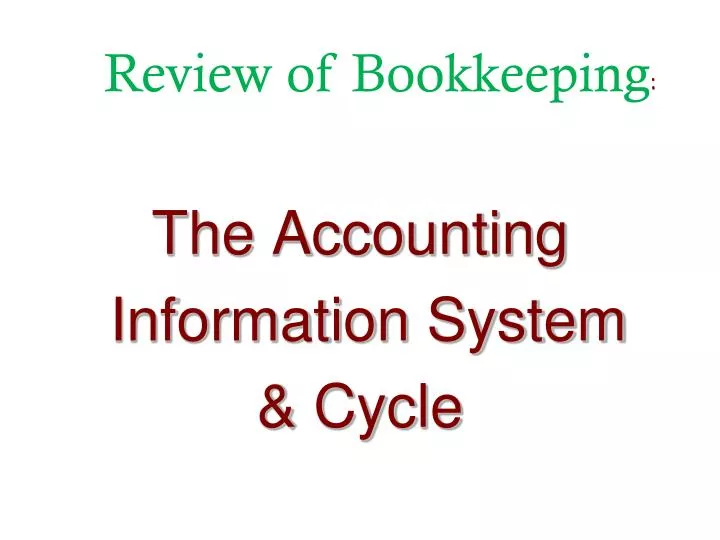

The Accounting Information System & Cycle. Review of Bookkeeping :. The Accounting Cycle. Transactions. 9. Reversing entries. 1. Journalization. 8. Post-closing trial balance. 2. Posting. 7. Closing entries. 3. Trial balance. 6. Financial Statements. Work Sheet. 4. Adjustments.

E N D

The Accounting Information System & Cycle Review of Bookkeeping:

The Accounting Cycle Transactions 9. Reversing entries 1. Journalization 8. Post-closing trial balance 2. Posting 7. Closing entries 3. Trial balance 6. Financial Statements Work Sheet 4. Adjustments 5. Adjusted trial balance

Transactions Question:Are the following events recorded in the accounting records? Discuss product design with potential customer. Purchased a computer. Event Pay rent. Is the financial position (assets, liabilities, or stockholders’ equity) of the company changed? Criterion Record/ Don’t Record

Accounting Transactions Transaction Analysis The process of identifying the specific effects of economic events on the accounting equation. Basic Accounting Equation Assets Liabilities Stockholders’ Equity + =

Accounting Transactions Transaction Analysis

Transactions: Tabular Format Illustration:1.On October 1, cash of $10,000 is invested in Sierra Corporation by investors in exchange for $10,000 of common stock. 1. +10,000 +10,000

Accounting Transactions 2. On October 1, Sierra borrowed $5,000 from Castle Bank by signing a 3-month, 12%, $5,000 note payable. 1. +10,000 +10,000 2. +5,000 +5,000

Accounting Transactions 3. On October 2, Sierra purchased office equipment by paying $5,000 cash to Superior Equipment Sales Co. 1. +10,000 +10,000 2. +5,000 +5,000 3. -5,000 +5,000

Accounting Transactions 4. On October 2, Sierra received a $1,200 cash advance from R. Knox, a client. 1. +10,000 +10,000 2. +5,000 +5,000 3. -5,000 +5,000 4. +1,200 +1,200

Accounting Transactions 5. On October 3, Sierra received $10,000 in cash from Copa Company for advertising services performed. 1. +10,000 +10,000 2. +5,000 +5,000 3. -5,000 +5,000 4. +1,200 +1,200 5. +10,000 +10,000

Accounting Transactions 6. On October 3, Sierra Corporation paid its office rent for the month of October in cash, $900. 1. +10,000 +10,000 2. +5,000 +5,000 3. -5,000 +5,000 4. +1,200 +1,200 5. +10,000 +10,000 6. -900 -900

Accounting Transactions 7. On October 4, Sierra paid $600 for a one-year insurance policy that will expire next year on September 30. 1. +10,000 +10,000 2. +5,000 +5,000 3. -5,000 +5,000 4. +1,200 +1,200 5. +10,000 +10,000 6. -900 -900 7. -600 +600

Accounting Transactions 8. On October 5, Sierra purchased a three-month supply of advertising materials on account from Aero Supply for $2,500. 1. +10,000 +10,000 2. +5,000 +5,000 3. -5,000 +5,000 4. +1,200 +1,200 5. +10,000 +10,000 6. -900 -900 7. -600 +600 8. +2,500 +2,500

Accounting Transactions 9. Hired employees: nothing to enter. 1. +10,000 +10,000 2. +5,000 +5,000 3. -5,000 +5,000 4. +1,200 +1,200 5. +10,000 +10,000 6. -900 -900 7. -600 +600 8. +2,500 +2,500

Accounting Transactions 10. On October 20, Sierra paid a $500 dividend. 1. +10,000 +10,000 2. +5,000 +5,000 3. -5,000 +5,000 4. +1,200 +1,200 5. +10,000 +10,000 6. -900 -900 7. -600 +600 8. +2,500 +2,500 10. -500 -500

Accounting Transactions 11. Employees have worked two weeks, earning $4,000 in salaries, which were paid on October 26. 1. +10,000 +10,000 2. +5,000 +5,000 3. -5,000 +5,000 4. +1,200 +1,200 5. +10,000 +10,000 6. -900 -900 7. -600 +600 8. +2,500 +2,500 10. -500 -500 11. -4,000 -4,000

Bookkeeping: The Account • Record of increases and decreases in a specific asset, liability, equity, revenue, or expense item. • Debit = “Left” • Credit = “Right” Account An Account can be illustrated in a T-Account form.

Debit and Credit Procedures • Double-entry accounting system • Each transaction must affect two or more accounts to keep the basic accounting equation in balance. • Recording done by debiting at least one account and crediting another. • DEBITSmust equalCREDITS.

Debit and Credit Procedures If Debits are greater than Credits, the account will have a debit balance. Transaction #1 $10,000 $3,000 Transaction #2 Transaction #3 8,000 Balance $15,000

Debit and Credit Procedures If Credits are greater than Debits, the account will have a credit balance. Transaction #1 $10,000 $3,000 Transaction #2 8,000 Transaction #3 Balance $1,000

Dr./Cr. Procedures for Assets and Liabilities • Assets - Debits should exceed credits. • Liabilities – Credits should exceed debits. • The normal balance is on the increase side. SO 3 Define debits and credits and explain their use in recording business transactions.

Dr./Cr. Procedures for Stockholders’ Equity • Owner’s investments and revenues increase stockholder’s equity (credit). • Dividends and expenses decrease stockholder’s equity (debit). SO 3 Define debits and credits and explain their use in recording business transactions.

Dr./Cr. Procedures for Revenue and Expense • The purpose of earning revenues is to benefit the stockholders. • The effect of debits and credits on revenue accounts is the same as their effect on stockholders’ equity. • Expenses have the opposite effect: expenses decrease stockholders’ equity. SO 3 Define debits and credits and explain their use in recording business transactions.

Debits and Credits Summary Normal Balance Debit Normal Balance Credit SO 3 Define debits and credits and explain their use in recording business transactions.

Debits and Credits Summary Balance Sheet Income Statement - + Asset Liability Equity Revenue Expense = = Debit Credit SO 3 Define debits and credits and explain their use in recording business transactions.

Stockholders’ Equity Relationships Illustration 3-15 SO 3 Define debits and credits and explain their use in recording business transactions.

Summary of Debit/Credit Rules Relationship among the assets, liabilities and stockholders’ equity of a business: Illustration 3-16 Basic Equation Assets = Liabilities + Stockholders’ Equity Expanded Basic Equation The equation must be in balance after every transaction. For every Debitthere must be a Credit. SO 3 Define debits and credits and explain their use in recording business transactions.

Steps in the Recording Process Illustration 3-17 Transfer journal information to ledger accounts Analyze each transaction Enter transaction in a journal Business documents, such as a sales slip, a check, a bill, or a cash register tape, provide evidence of the transaction. SO 4 Identify the basic steps in the recording process.

The Journal • Book of original entry. • Transactions recorded in chronological order. • Contributions to the recording process: • Discloses the complete effects of a transaction. • Provides a chronological record of transactions. • Helps to prevent or locate errors because the debit and credit amounts can be easily compared.

The Journal Journalizing - Entering transaction data in the journal. Illustration: Presented below is information related to Sierra Corporation. Oct. 1 Sierra issued common stock in exchange for $10,000 cash. 1 Sierra borrowed $5,000 by signing a note. 2 Sierra purchased office equipment for $5,000. Instructions - Journalize these transactions. SO 4 Explain what a journal is and how it helps in the recording process.

Journalizing Oct. 1 Sierra issued common stock in exchange for $10,000 cash. General Journal Cash 10,000 Common stock 10,000 SO 4 Explain what a journal is and how it helps in the recording process.

Journalizing Oct. 1 Sierra borrowed $5,000 by signing a note. General Journal Cash 5,000 Notes payable 5,000 SO 4 Explain what a journal is and how it helps in the recording process.

Journalizing Oct. 2 Sierra purchased office equipment for $5,000. General Journal Office equipment 5,000 Cash 5,000 SO 4 Explain what a journal is and how it helps in the recording process.

The Ledger Ledger contains the entire group of accounts maintained by a company. Illustration 3-19 SO 6 Explain what a ledger is and how it helps in the recording process.

Chart of Accounts Accounts arranged in sequence in which they are presented in the financial statements. SO 6 Explain what a ledger is and how it helps in the recording process.

Posting Posting – the process of transferring amounts from the journal to the ledger accounts. General Journal J1 101 General Ledger Oct. 1 Owner investment J1 10,000 10,000 SO 7 Explain what posting is and how it helps in the recording process.

The Recording Process Illustrated Illustration 3-21 Follow these steps: 1. Determine what type of account is involved. 2. Determine what items increased or decreased and by how much. 3. Translate the increases and decreases into debits and credits. SO 7 Explain what posting is and how it helps in the recording process.

The Recording Process Illustrated Illustration 3-22 Follow these steps: 1. Determine what type of account is involved. 2. Determine what items increased or decreased and by how much. 3. Translate the increases and decreases into debits and credits. SO 7 Explain what posting is and how it helps in the recording process.

The Recording Process Illustrated Illustration 3-23 Follow these steps: 1. Determine what type of account is involved. 2. Determine what items increased or decreased and by how much. 3. Translate the increases and decreases into debits and credits. SO 7 Explain what posting is and how it helps in the recording process.

The Recording Process Illustrated Additional Transactions Illustration 3-24 SO 7 Explain what posting is and how it helps in the recording process.

The Recording Process Illustrated Additional Transactions Illustration 3-25 SO 7 Explain what posting is and how it helps in the recording process.

The Recording Process Illustrated Additional Transactions Illustration 3-26 SO 7 Explain what posting is and how it helps in the recording process.

The Recording Process Illustrated , Additional Transactions Illustration 3-27 SO 7 Explain what posting is and how it helps in the recording process.

The Recording Process Illustrated Additional Transactions Illustration 3-28 SO 7 Explain what posting is and how it helps in the recording process.

The Recording Process Illustrated Additional Transactions Illustration 3-29 SO 7 Explain what posting is and how it helps in the recording process.

The Recording Process Illustrated Additional Transactions Illustration 3-30 SO 7 Explain what posting is and how it helps in the recording process.

The Recording Process Illustrated Additional Transactions Illustration 3-31 SO 7 Explain what posting is and how it helps in the recording process.

Summary Illustration of Journalizing Illustration 3-32 SO 7 Explain what posting is and how it helps in the recording process.

Summary Illustration of Journalizing Illustration 3-32 SO 7 Explain what posting is and how it helps in the recording process.