Download

1 / 16

160 likes | 248 Views

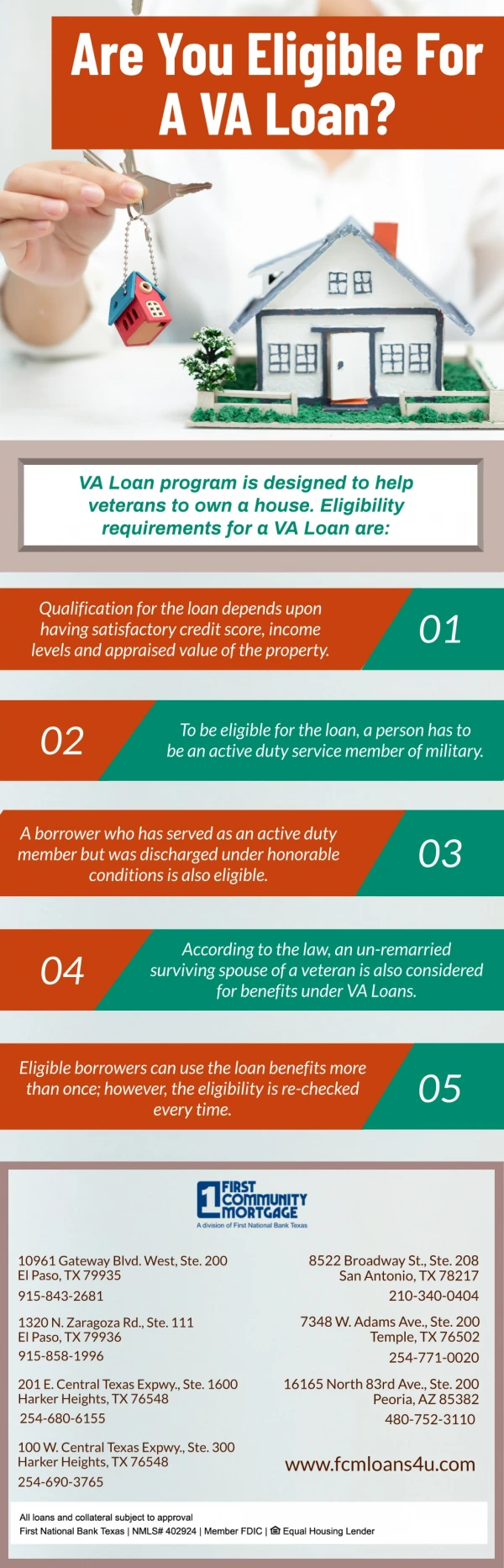

Eligible Loan Purposes. Purchase or Construct a Home. Loan may include simultaneous purchase of the land on which the residence is or will be situated Loans for construction of a residence on land already owned by the veteran

E N D

Purchase or Construct a Home • Loan may include simultaneous purchase of the land on which the residence is or will be situated • Loans for construction of a residence on land already owned by the veteran • Property may consist of up to four family units (See Chapter 7.1 of the VA Lenders Handbook for joint loan exceptions.)

Interest Rate Reduction Refinance • To refinance an existing VA-guaranteed loan • Must lower interest rate and principal and interest payment • See Chapter 6, section 1 for guidelines and exceptions.

Cash-Out/Regular Refinance • Pay off any lien against the property • VA, FHA, Conventional • Tax lien, judgment, etc. • Pay other consumer debt • Obtain cash

Repair, Alter or Improve Residence • To repair, alter or improve a home owned by the veteran and occupied as a home or • May be made in conjunction with the purchase of a property. • Alterations and repairs must be those ordinarily found on similar properties of comparable value in the community. • Reference: Chapter 7, section 4

Repair, Alter or Improve Residence (Continued) • Value consideration • The cost of improvements to structures may be added into the loan amount for the purchase of improved property to the extent that their value supports the loan amount. • Appraisal would be ordered “as repaired”. • Plans and specs would need to be provided to the appraiser.

Energy Efficient Mortgage • Energy efficient items may be added to any loan type • Purchase • Interest Rate Reduction Refinance • Cash-Out (Regular) Refinance • Guidelines and list (not all inclusive) of improvements in Chapter 7, section 3 of the VA Lenders Handbook.

Condominium • The program may be used to purchase a one-family residential unit in a condominium housing development approved by VA. • Reciprocity with HUD approvals in most cases • Reference: Chapter 16-A.02

Cooperative Dwellings • VA is authorized to guaranty loans made to veterans for the purchase of stock or membership in co-op housing corporations to enable veterans to occupy as their primary residence. • Reference: VA Circular 26-08-6

Farm Residences • VA does not make “farm loans”. However, veterans may purchase a farm on which there is a farm residence. • Value based on acreage using similar comparables with adjustments for differences in site size. • The farmland is appraised at its residential value. • Chapter 11, section 12g, discusses this issue.

Ineligible Loan Purposes • Purchase of unimproved land, • Purchase or construction of dwelling for investment purposes, • Purchase of combined residential and business property unless • Property is primarily residential • There is not more than one business unit and • Non –residential area is less than 25% of the total floor area.

Ineligible Loan Purposes(Continued) • Purchase of more than one separate residential unit or lot unless the veteran will occupy one unit and there is evidence that the residential units: • are unavailable separately, • have a common owner, • have been treated as one unit in the past, • assessed as one unit, or • partition is not practical.

Ineligible Loan Purposes(Continued) • Cash to the veteran* • Only permissible for certain refinancing loans as follows: • Interest Rate Reduction Refinance • In the event of change of payoff, computational error, etc. • Up to $500 • Cash-out refinance *Ernest money can be refunded to the veteran on a no down payment loan.

Reference: • Chapter 3, section 2, of the VA Lenders Handbook. • www.warms.vba.va.gov/pam26_7.html

If you have questions, contact your nearest Regional Loan Center. Contact information may be found at www.homeloans.va.gov/rlcweb.htm.