Download

1 / 28

411 likes | 946 Views

Regulation of Microfinance Institutions in India. Agenda. Microfinance sector - overview Analysis of the existing regulatory regime Global experience regulating Microfinance Institutions Assessment of pending regulatory recommendations Malegam Committee Recommendations

E N D

Agenda • Microfinance sector - overview • Analysis of the existing regulatory regime • Global experience regulating Microfinance Institutions • Assessment of pending regulatory recommendations • Malegam Committee Recommendations • Microfinance Financial Sector Bill 2010 • MFI response to new RBI Regulation

Microfinance Sector • Two models – Self Help Group (SHG) model and Microfinance Institution (MFI) model • Microfinance Institutions (MFIs) serve 27 million clients and have 183 billion crore loans outstanding in India • Services have been geographically disproportionate • Services have expanded greatly in the Southern region, though services are limited in the Northern and Western regions • Poorest districts still generally do not have services • Lack of product diversity

Andhra Pradesh Crisis, 2010 • Clients and politicians accuse microfinance institutions of coercive collection practices, usurious interest rates, and use of selling practices that result in over-indebtedness • Microfinance clients stopped repaying loans in late 2010 in Andhra Pradesh (AP) • AP state government issued an ordinance that severely limits the operations of MFIs • Microfinance institutions all over India have had trouble accessing adequate financing as a result • RBI enlisted the Malegam Committee to generate regulatory recommendations to address issues of the sector

Agenda • Microfinance sector - overview • Analysis of the existing regulatory regime • Global experience regulating Microfinance Institutions • Assessment of pending regulatory recommendations • Malegam Committee Recommendations • Microfinance Financial Sector Bill 2010 • MFI response to new RBI Regulation

Existing Regulatory Structure Legal forms of MFIs For-profit MFIs account for over 80% of total client outreach of all the MFIs

Existing Regulation • NBFCs (for-profit) • Regulation primarily prudential, not specific to microfinance • Can collect deposits if achieve investment grade rating (no MFI has accomplished this) • Other Microfinance institutions • No regulation beyond registration, which is often done at state level • State regulation • There is little clarity regarding central vs. state jurisdiction • Some MFIs are subject to state laws such as Moneylending Act • A few states have passed ordinances restricting some microfinance practices

Existing Regulation • Priority Sector Lending • Microfinance institutions qualify for priority sector funds • Funding Restrictions • NBFCs cannot access External Commercial Borrowing • Minimum Equity investment is US $500,000 which can only account for 51% of company

Existing RegulationOpportunities for Improvement • Lack of clarity on state and central jurisdiction • No consumer protection regulation • No regulation for credit reference services and information sharing • Unduly restrictive standards for deposit collection • Restrictions in accessing funding from various sources • Overall lack of monitoring and supervision

Agenda • Microfinance sector - overview • Analysis of the existing regulatory regime • Global experience regulating Microfinance Institutions • Assessment of pending regulatory recommendations • Malegam Committee Recommendations • Microfinance Financial Sector Bill 2010 • MFI response to new RBI Regulation

Minimum Capital Requirements • Used to control number of qualifying institutions • Can change over time, and within country • Bolivia increases requirement as penetration develops and existing institutions mature • Pakistan minimum capital requirement changes depending on district and province of operation • No uniform standard amount

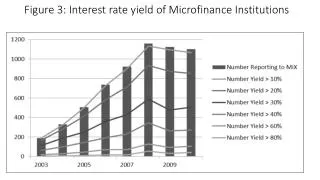

Interest Rate Caps • Some countries implement interest rate caps aiming to protect the poor from usurious charges • Interest rate caps often reduce financial services for lower-income and rural clients, increase MFI solvency risk, and encourage less transparency

Consumer Protection • Consumer protection requirements vary greatly across the globe, coming most often in the form of legislation or institution self-regulation • Documentation requirements • Plain-language, documentation in the local language, describe recourse rights and processes, annual interest rate using a standard formula, all applicable fees, computation methods, required insurance • Facilitate customer complaint procedures (Example: Peru) • Financial regulatory authority mandated procedure for receiving, responding, and resolving customer complaints • 99% of 400,000 customer complaints were handled by financial regulatory authority • Implement financial literacy education programs • On-site and off-site monitoring • As a result, customer complaints are down 32% since 2004

Agenda • Microfinance sector - overview • Analysis of the existing regulatory regime • Global experience regulating Microfinance Institutions • Assessment of pending regulatory recommendations • Malegam Committee Recommendations • Microfinance Financial Sector Bill 2010 • MFI response to new RBI Regulation

Malegam Committee Recommendations Overview • Original report released in January 2011 • The recommendations address many of the major issues of the sector: • Identifying microfinance institutions and qualification for priority sector lending • Consumer over-indebtedness • Credit Pricing • Product Restrictions • Documentation • In May 2011 RBI “broadly accepted” the report, and specified priority sector lending qualification

Passed Malegam Regulation • Minimum 85% of loan portfolio: • Is disbursed to a rural household with annual income not exceeding Rs 60,000 or an urban household with annual income not exceeding Rs 1,20,000 • Does not exceed Rs 35,000 for the first cycle and Rs 50,000 for subsequent cycles • Does not result in greater than Rs 50,000 total indebtedness for the borrower household • Has a tenure not less than 24 months for loan amount in excess of Rs 15,000 without prepayment penalty • Is extended without collateral • Is repayable by weekly, fortnightly, or monthly installments at the choice of the borrower

Passed Malegam Regulation • MFIs must adhere a margin cap of 12 percent and an interest rate cap of 26 percent to qualify for priority sector lending • Only three components are to be included in pricing of loans, (a) a processing fee not exceeding 1% of the gross loan amount, (b) the interest charge and (c) the insurance premium. • A borrower is not required to be a member of a SHG/JLG to receive a loan • There should not be any penalty for delayed payment • No Security Deposit/ Margin are to be taken. • 75% of loans are for income generation

Micro Financial Sector Bill 2011 • Designation of RBI as the sole regulator for all microfinance institutions, • Power to regulate interest rate caps, margin caps, and prudential norms • All microfinance institutions must register with RBI • Formation of a Micro Finance Development Council, which will advise the central government on a variety of issues relating to microfinance • Formation of State Advisory Councils to oversee microfinance at the state level • Creation of Micro Finance Development Fund for investment, training, capacity building, and other expenditures as determined by RBI

Agenda • Microfinance sector - overview • Analysis of the existing regulatory regime • Global experience regulating Microfinance Institutions • Assessment of pending regulatory recommendations • Malegam Committee Recommendations • Microfinance Financial Sector Bill 2010 • MFI response to new RBI Regulation

CMF Survey • CMF interviewed 32 MFIs in Andhra Pradesh in Summer 2011 • Survey included MFIs which represent a variety of lending models, sizes, and legal forms • Overall, MFIs reacted positively to new regulation