Download

1 / 20

200 likes | 212 Views

Analyzing beneficiary trends in Medicare plan selection, premiums, deductibles, and gap coverage in 2007-2008. Highlighting improvements for 2008 and the power of Part D performance metrics.

E N D

2007 Enrollment by Benefit Type • Beneficiaries are selecting alternative design plan types. Data as of Jan07 Analysis excludes FBDE & LIS

2007 Enrollment by Deductible Category • Beneficiaries are selecting plans with no deductible. Data as of Jan07 Analysis excludes FBDE & LIS

2007 Enrollment by Premium Category • Beneficiaries are selecting plans with low or no premiums Data as of Jan07 Analysis excludes FBDE & LIS

2007 Enrollment by Gap Coverage • Coverage in the gap is not a significant factor in plan selection. Data as of Jan07 Analysis excludes FBDE & LIS

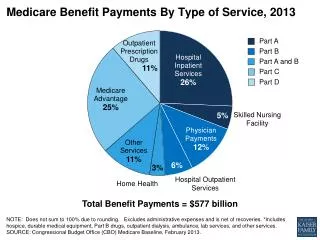

2008 Costs Continue to be Lower than Expected • Fewer Part D plans offerings in 2008 than 2007 • Plan offerings within a sponsor have more meaningful differences • Overall, premiums will be stable for many beneficiaries but slightly higher for some • 2008 standard average premium is $25 for basic coverage • Slow growth in Rx drug costs • Increased generic use • Effective plan negotiation • Competition

Beneficiaries Continue to Have Multiple Low Cost PDP Choices • More than 90% of beneficiaries in stand-alone PDPs will have access to a plan in 2008 with premiums lower than they paid in 2007. • In every state, beneficiaries will have access to at least one PDP with premiums of less than $20, and a choice of at least 5 plans with premiums of less that $25 a month. • Beneficiaries in all states have access to a PDP with no drug deductible for a premium of less than $26 per month. • Beneficiaries in all states have access to PDP plans with coverage in the gap for generic drugs for under $50 a month.

Beneficiaries Have Even Lower Cost MA-PD Choices • There are more MA-PD health plan offerings in 2008 than in 2007. • MA-PD premiums will average $11 lower than premiums for PDPs in 2008 (vs. $7 lower in 2007). • Over 90% of people with Medicare will have access to a MA-PD for a $0 premium and with a $0 drug deductible.

Highlighted Improvements for 2008 • Benefit and Formulary Reviews • Enhanced specificity in PBP software • Negotiation of meaningful differences & outliers • Systems Improvements • LIS data exchanged among CMS, States and SSA • Ability to correct data in CMS systems • “4Rx” data mandatory on plan-generated enrollments • Automation of plan TrOOP balance transfer processes • Performance Metrics • Additional measures developed • Increased transparency through integration with Drug Plan Finder

More Robust Formulary Reviews • Prevent discrimination against beneficiaries by age, disease, or setting (e.g. long-term care) • Utilize reasonable benchmarks to check that drug lists are robust • Review tiering and utilization management strategies • Identify potential outliers at each review step for further CMS investigation and obtain reasonable clinical justification when outliers appear to create access problems • Ensure minimum transition coverage policies

2007 vs. 2008 Formularies (PDP) Note: Adjusted for drugs comparable on both the 2007 and 2008 Medicare Formulary Reference Files.

2007 vs. 2008 Formularies (PDP) Note: Data limited to plans offered both in 2006 and 2007. Excludes employer sponsored plans. Formulary data from 2006 as of 4/20/2006, and 2007 as of 7/5/2006.

The Power of Part D Performance Metrics • Establishes performance benchmarks: • CMS’ long-term goal is to establish performance benchmarks based on historical experience with Part D • Once benchmarks are established, CMS will work with plans to improve performance • If high performance in an area becomes standard for all plans then a measure may be retired • CMS will have composite scores for monitoring purposes beginning Nov. 15, 2007. • Creates a feedback loop

Example: Monitoring of Drug Pricing • CMS has a current performance metric to measure drug price changes. • The average drug increase in the CPI (Feb. –Aug. 2006) was 5%. • 13% of PDP drug prices exceeded the CPI increase. • Plans were given a high rating if they had a lower percentage (<22%) exceeding the CPI. • Plans were given a low rating if they had a higher percentage (>33%) exceeding the CPI. • 7 PDPs and 34 MA-PDs received low ratings (1 or 2 stars).

LIS-Eligible Beneficiaries and Reassignment • CMS re-assigns LIS eligible beneficiaries who are enrolled in plans that will no longer have a premium within a $1.00 of LIS premium subsidy benchmark • Also to those whose plans are leaving Medicare program • No major problems in 2007 • For 2008, 1 in 6 dual eligible beneficiaries may switch to a new plan to avoid a premium increase

LIS Outreach to Those Who Will Face a Change in 2008 • Re-assignment Notices (blue) provide information on: • Moving to the new plan • Staying in the current plan • Selecting a different plan • New “Chooser” Notices (tan) provide information on: • Premium responsibility for 2008 • Zero premium plans available • Evaluating plan options

LIS Outreach to Those Who Haven’t Applied for Extra Help “The Community is Coming Together” • LIS national kick-off and partner meetings • Data-sharing for targeting outreach • New materials – “Photo novellas” • Stronger partnerships • Community outreach