Download

1 / 38

380 likes | 506 Views

Stages of Economic Policy in Latin America. Colonialism Export-led primary product extraction Prebisch and Import Substitution Industrialization: 1930s-1960s Economic Growth, Oil Shocks, & Debt Accumulation 1960s-1970s

E N D

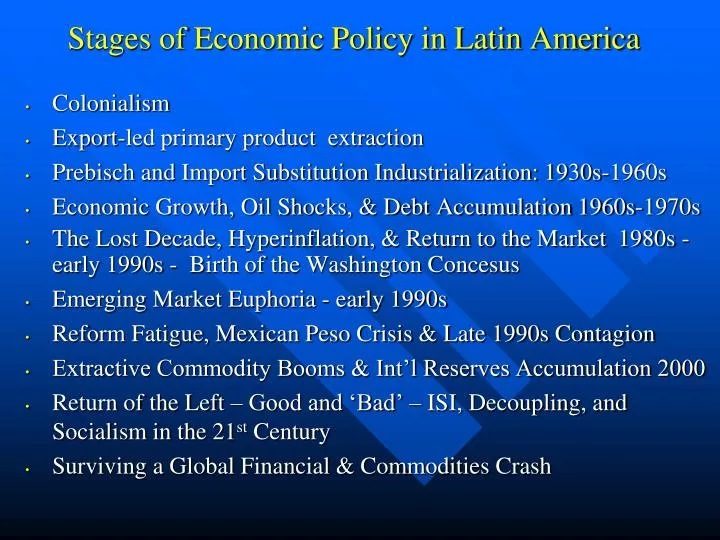

Stages of Economic Policy in Latin America • Colonialism • Export-led primary product extraction • Prebisch and Import Substitution Industrialization: 1930s-1960s • Economic Growth, Oil Shocks, & Debt Accumulation 1960s-1970s • The Lost Decade, Hyperinflation, & Return to the Market 1980s - early 1990s - Birth of the Washington Concesus • Emerging Market Euphoria - early 1990s • Reform Fatigue, Mexican Peso Crisis & Late 1990s Contagion • Extractive Commodity Booms & Int’l Reserves Accumulation 2000 • Return of the Left – Good and ‘Bad’ – ISI, Decoupling, and Socialism in the 21st Century • Surviving a Global Financial & Commodities Crash

Pre-1900s: Colonial Legacy Why Political Economy? • Strategic Unilateralism • Historical View - Bartolome de las Casas • Changing Exploiters: • Spain • Portugal • United Kingdom • United States • Hope and Memory • The popular press • The Military and the Market – The Southern Cone

Phase I: Trade Volatility, Trade Crises Latin America’s Secular Decline in the Terms of Trade Chronic Balance of Trade Deficits Import Constrained Growth 1930s Depression and “Inward Development”

Prebisch Hypothesis • Supply Side and Demand Side formulations-- Unequal exchange in the dynamic relations of trade between the Center and Periphery • Latin America’s Early Appraisal of Free Trade and the Market

Profits from these productivity increases are not realized in the Periphery, but are, instead, transferred to the Center nations in the form of falling prices for imported Peripheral inputs. Producing a corresponding reduction in the Terms of Trade for the Periphery...

Prebisch Hypothesis • Demand Side -- “Elasticities Pessimism” Center: Manufactured product exports with high income elasticity of demand Periphery: Primary materials, low value added, extractive exports with low income elasticity of demand

Policy Regime - Import Substitution Industrialization: 1930s-1960s • Restrict manufactured imports to reverse trade imbalance • Promote domestic high value added industrial production to substitute foreign imports • Decades of Policy Consensus for State Led Development Initiatives

Peripheral Growth and Debt Dependency:A Model • X*p = mc * Y*c (Peripheral Export Growth) • M*p = mp * Y*p (Peripheral Import Growth) • X* = M*(Balanced Trade Condition) • mc * Y*c = mp * Y*p • mp > mc implies (Elasticities Pessimism) • Y*c > Y*p (Dependent Growth) • Y*p > Y*c if and only if X* < M* (Peripheral Growth with Trade Deficits & Debt Accumulation)

From Dependent Trade to Debt-Led Growth • Growth with balanced trade was necessarily dependent growth • For Peripheral growth rates to outpace the Center required continuous recourse to debt accumulation • Popular insurgency and the Cuban Revolution shifted capital inflows from FDI to portfolio and ‘hot money’ investments

Phase II: Oil shocks & Debt Accumulation 1960s-1970s • ISI Policies fostered rapid economic growth • Manufacturing growth confined to Brazil, Mexico, and Argentina • Growth came at the expense of large debt overhang • World oil price escalation increased Latin debt accumulation as petrodollars were recycled to finance battered current accounts

Stylized Facts • Latin America’s Current Account Deficits (%GDP) 1972 2.2% 1982 5.5% • Latin America’s Growth Rate 1960s - 70s 7-10% • Latin America’s Ratio of Foreign Debt to GDP 1975 19% 1982 46%

Debt Overhang & Increased Interest Rate Sensitivity of Region’s External Balance • Vulnerability to external shocks: 1980s Reagan-Volker anti-inflation policy -- instant financial insolvency CA - KA - OR +

Reagan-Volker Interest Rate Hikes turn US capital markets into a financial “black hole”

Phase III: The Lost Decade, Hyperinflation, & Return to the Market 1980s - early 1990s • Current Account (development deficits) no longer financed by Capital inflows • Loans come due, debt service burden balloons • IMF calls for austerity to generate CA surpluses to generate foreign exchange to repay debt • Fiscal Deficits deepen to beyond 12% of GDP to finance local currency spending • Historically pathological hyperinflation ensues -- a follow-on from the debt crisis

The Loans Come Due • From 1982-85 Net Capital Outflows from Latin America to DCs averaged 6% of Regional GDP - $34 Billion/ Year • Transfer Achieved by Contraction of Region’s Economy -- 6% of GDP Annually • Upper Classes Incurred the Debt. Lower Classes Paid it Off • Private, Corporate LT Loans – Profits from Operations Privatized while Losses from Failures ‘Socialized’ into Mounting Government Deficits • The ‘Lost Decade’ of the 1980s was an Engineered Contraction to Produce Trade Surplus to Service International Debt Obligations

Underlying Fiscal Imbalance Y ‘la Maquinita’

Consolidation of the Washington Consensus • Orthodox vs Heterodox Stabilization Efforts in the Mid-1980s • Failed Heterodox programs in Peru, Argentina, and Brazil push policy consensus • Capital Surges and Emerging Market Euphoria (Early 1990s)

Phase IV: The Peso Crisis, Global Financial Volatility, and Reform Fatigue • Anatomy of a Currency Crisis and Global Contagion CA - 8%/GDP KA + 8%/GDP OR fixed exchange rate CA - KA - OR + fixed exchange rate -- International Reserves Drain

Political Economy -- Hot Money & Bad Political Assumptions Peso Crisis in Detail

Lessons of the Peso Crisis for Latin America • 1) The current account is a key variable that should not get “out of line”. • the current account deficit should rarely exceed 3% of GDP in the long run. • 2) The composition of capital inflows-short-term portfolio versus long-term direct investment funds-is extremely important. • Short term portfolio flows are very sensitive to short-term changes in interest rates and other political and macroeconomic variables. FDI is less volatile and does not respond to short-term speculative factors.

IMF and Crisis Adjustment in Latin America • IMF Kill or Cure?International Lender of Last Resort or Arm of Int'l Finance Capital? Absorption Approach to Financial Programming X - M = Y - (C +I+G) X - M = (S - I) + (T - G) (net private savings, government surplus) IMF Conditionality: Debt Service or Economic Development?

Contagion and Banking Liberalization • Nash, “Bankers are just like the rest of us, only richer”... • IMF: 131 of member 181 nations experienced banking crises in a five year period whose resolution cost > 5% of GDP

Prebisch Revisited • Final Note: • The composition of exports for Latin America is still dominated by low value added primary product production… • Commodity Composition of Trade: US & S. America • Commodity Composition of Trade: US & Central America

But energy and commodities pricesrise with Asian industrial demand • Rising Terms of Trade, Balance of Payments Surplus accumulation in Latin America

Popular struggles to assert control over the state and energy assets command dollar reserve surpluses for redistributive social policy agendas. • The Pirates of the Caribbean - extend to Pirates of the Andes -Bolivia, Ecuador…

The “Good Left” and “Bad Left” --models of a Left Agenda in Latin America • The IMF irrelevant as windfall dollar surpluses payoff old debt • Latin America projects new axes of accumulation: South-South, and South-East collaboration in a multipolar world. • Banco de Sur • Seis Horas

Lessons of the Peso Crisis for Latin America • 3) Productivity gains are a fundamentally important element in the way in which the overall external sector develops. • 4) There is an inherent danger in using fixed exchange rates as a stabilization device. • Experience has shown that they tend to generate real exchange rate overvaluation and loss in external competitiveness.

Lessons of the Peso Crisis for Latin America • 5) The structure of Government debt is extremely important • short-term debt represents a true danger under free capital mobility.