Download

1 / 10

100 likes | 175 Views

Explore strategies for managing refinancing conundrums and declining fundamentals in the commercial real estate market due to forced deleveraging. Analyze the impact on property values, cap rates, and rents, and discover opportunities for recapitalization through equity issuance.

E N D

Urban Land Institute – Fall 2010 Deleveraging and Recapitalization of Commercial Real Estate November 4, 2009

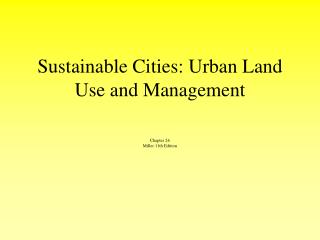

$450 $397.0 $400 $353.6 $213.4b Shortfall $322.8 $350 $290.0 $300 $106.4b Shortfall $139.2b Shortfall $170.0b Shortfall $250 $ billions $200 $150 $100 Cumulative Shortfalls 2009-2012: $629 billion $50 $0 2009E 2010E 2011E 2012E Best Case Originations1 Banks Insurance Co's CMBS Total* High Volume of Near Term Debt Maturities • Refinancing poses significant challenges due to more strict underwriting standards and declining fundamentals. • The CMBS market remains closed and few alternatives have emerged to replicate its peak origination volume. • Limited credit availability will cause refinancing shortfalls. 1 Origination projections based on the average 4-year historical gross originations from all non-CMBS lenders (excludes HUD/Gov’t). * CMBS total includes both fixed and floating rate loans to first maturity. Source: Wachovia, Commercial Mortgage Alert

Cumulative 2004-08: $122 billion Aggressive Underwriting Standards of the Past Pose Significant Challenges Loans in Special Servicing as % of CMBS Outstanding CMBS Loan Maturities by Vintage Source: Wachovia Securities Source: Realpoint

The Need to Deleverage May Force Sales and Recapitalizations Refinancing Conundrum Declining Fundamentals • The forced deleveraging of commercial real estate will cause current owners to recapitalize their investment or force sales. • Pricing down 35–50% from peak valuations. • Cap rates have increased 200-300 bps (+/-). • Rents have declined 25% (+/-). Original Equity: $20MM (gone) Debt Written Off: $15MM Swap Breakage Cost: ? Additional Equity to Refinance at 60% of Today’s Value: $26MM

Rebound of RMZ Helping REITs Recapitalize Real Estate Equity Issuance Volume by Offering Type1 MS PRICE Index (RMZ) 2007 - 2009 • REITS have raised approx. $23.8 billion of public equity capital YTD.

Public vs. Private Valuation Arbitrage • With the increase in REIT prices over the past several months an arbitrage between public and private valuations has developed. • Especially for companies in the upper quartile, implied cap rates based on current trading prices are significantly below the estimated private cap rates. • REITs are building substantial currency to take advantage of upcoming opportunities. Average: 8.5% Average: 7.8% Average: 8.5% Average: 7.5% Average: 9.3% Average: 8.0% Public valuations are becoming compelling relative to private valuations based on current implied cap rates Source: Green Street Advisors.

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 Real Estate Equity Capital Markets Remain Attractive for Issuers REIT Forward FFO Multiples Real Estate Funds Flows Source: Dealogic and FactSet. Market data as of 10/28/09. Green Street Advisors. 1 Chart excludes mortgage REITs, gaming deals, and index-add transactions.

The REIT Unsecured Market has Reopened • After gapping significantly during a long period of uncertainty and heightened risk, spreads have tightened and the market has opened for quality public names with strong liquidity positions. DRE 19s, 8.375% Yield HPT 14s, 8.125% Yield CLI 19s, 7.875% Yield PLD 14s, 7.75% Yield BDN 15s, 7.625% Yield DRE 15s, 7.50% Yield KIM 19s, 6.897% Yield AVB 20s, 6.119% Yield Yield curve based on Modified Adjusted Duration of 4.7 years AVB 17s, 5.717% Yield Such drastic tightening into attractive financing levels is unprecedented in the last five years Source: Barclays Capital Live, Bloomberg.

Cheap Pricey Rising Cap Rates for Core Assets? Unlevered Return Expectations on Real Estate vs Baa Rates Return Premium on Real Estate Unlevered IRR Expectations Minus Baa Rate As of 10/13/09

Limited US Sales Volume 40-50% of Post 9/11 & Post Dot Com Bust Volume • Transaction data suggests cap rates have risen but tight credit, the general unwillingness of owners to recognize loss of value, and an amend and extend approach by existing lenders has lead to limited transactions. • However, as maturities mount, owners will be forced to sell. • Given access to capital, REITs are well positioned to take advantage of the distress. • Public markets will play a key role in digging out of this mess. • The vast majority of transactions will be sales out of special servicers and banks. • Focus is now on interim defaults vs. maturity defaults. • Peak defaults will likely be in 2010, which should result in an increase in transactions. Source: Real Capital Analytics.