Download

1 / 16

170 likes | 413 Views

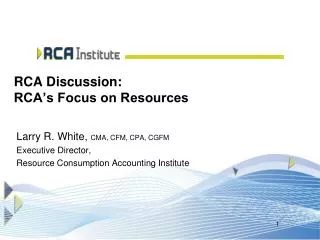

RCA Discussion: RCA’s Focus on Consumption. Larry R. White, CMA, CFM, CPA, CGFM Executive Director Resource Consumption Accounting Institute. Simple Process. Another Resource Pool (s) Or Final Product/Service. Resource Pool. Proportional. OUTPUT. Fixed. Organizational Element

E N D

RCA Discussion: RCA’s Focus on Consumption Larry R. White, CMA, CFM, CPA, CGFM Executive Director Resource Consumption Accounting Institute

Simple Process Another Resource Pool (s) Or Final Product/Service Resource Pool Proportional OUTPUT Fixed Organizational Element (Support or Production) Material/Commodity Labor Equipment Operating Budget Material Services (Reflecting Resources Applied) Resource Quantities Drive Monetary Quantities 2

More Realistic Resource Flows Resource Pool A Final Output 1 Resource Pool E Resource Pool B Final Output 2 Resource Pool F Final Output 3 Resource Pool C Resource Pool G Final Output 4 Resource Pool D Resource Pool H

What Characteristics of Consumption? • Proportional Relationship with Output • Output Increases, Resource is busier • Fixed Relationship with Output • Output Increases, Resource is still necessary but activity level relatively unchanged. • No Relationship with Output • The Resource use has no relationship with an output. • Excess Capacity • Don’t allocate. Apply to a responsibility/results level that is responsible for capacity decisions.

Traditional Approach Variability Product A Product B Service 1 Service 2 Service 3 Variable Cost $’s Change in Total $’s Due to a Change in Total Volume Fixed Cost Total Volume RCA Institute All Rights Reserved

Proportional Inputs Proportional Inputs Inputs & their $’s Inputs & their $’s Fixed Inputs Fixed Inputs Product A Product B An Output An Output Service 2 Service 3 Service 1 Proportional Inputs Proportional Inputs Proportional Inputs Inputs & their $’s Inputs & their $’s Inputs & their $’s Fixed Inputs Fixed Inputs Fixed Inputs An Output An Output An Output RCA Approach -Responsiveness RCA Institute All Rights Reserved

Example Bldg Space Bldg Space Inspections - Clean Output: Inspector Labor Hrs SQFT IT Support IT Support Inspections – Fines & Penalty # WS Fire Inspection Resource Pool # Cars # Miles Motor Pool Motor Pool Re-Inspections - Clean HR Events Re-Inspections – Fines & Penalty HR & Pay HR & Pay # PO’s # Man hrs Procurement Hearings/Court Appearances FD Internal Affairs

Example Product/Services Inspections Bldg Space Fire Inspectors Investigations Fire Investigators IT Support Readiness Motor Pool Fire Stations Idle/Excess Capacity HR & Pay Training Center Procurement Fire Safety Mission Internal Affairs Idle/Excess Capacity Fire Chief/Staff Results Segment

Consumption Relationships • Quantity Consumption with Values Qty & $'s • Resource Interrelationships - Activities Consumed by the Resources that the Services are Provided for Cost Object • Activities Consumed by a Cost Objects Activity 2 Qty & $'s Activity 1 Activity 4 Facilities Procurement Qty & $'s Qty & $'s Qty & $'s Qty & $'s Qty & $'s Qty & $'s Qty & $'s Utilities Human Resources Plant Maintenance © RCA Institute 2010

Capacity Analysis and Management Process Analysis and Management RCA Resource view Advantages Process view Advantages ABC GPK Activity-Focused Capacity-Focused Resource Consumption Accounting • RCA Inherits Core Principles from German Cost Management (GPK) • GPK is a Well Developed Standard Costing System • Principles Applied in Practice since the Late 1940’s • Principles Implemented by 3,000+ Companies • RCA Integrates • Activity-based Costing and Throughput Concepts • RCA Creates an Integrated Economic Model of Operations for Decision Making • Enterprise Optimization • Principle Based • Superior Marginal Analytics

www.RCAInstitute.org lwhite@rcainstitute.org 757 288 6082

S: Ancillary Production Equipment S: Plant Engineering and Maintenance S: Administration Human Resources & Accounting RP: Chiller (Hours) Capacity: 50,000 Output Qty: 50,000 RP: PlantMaintenance (Maint. Labor) Capacity: 30,000 Output Qty: 30,000 RP: Dryer (Hours) Capacity: 100 Output Qty: 100 Legend S-Support P- Production Perform Accounting Perform Admin Department P: Extrusion Line S: Quality Assurance Resource Pool Abbreviated RP QA Testing RP: QA Labor (Labor hours) Capacity: 14,000 Output Qty: 14,000 Activity RP: Extrusion Labor (Labor hours) Capacity; 32,000 Output Qty: 30,000 RP: Extrusion Machine1 (Machine hours) Capacity; 17,520 Output Qty: 10,000 Product Returns Perform HR Manufacturing Costs Product Support Cost Budgeted Products RP: Admin Labor (Labor hours) Capacity: 17,000 Output Qty: 17,000 Common Fixed Costs Product P & L’s RCA Storyboard

Resource Consumption Accounting Pillar 1: Focus on Resources & their Consumption • Understand your Resources & Their Consumption….Understand Cost • Provides a Framework for Capacity Management Pillar 2: Quantity Structure for Resource Consumption • Operational Quantities Drive Costs • Model the Operation & Use of Resources….then Apply Cost • Enables Resource Capacity Management • Demonstrates Causality of Value Chain Relationships Pillar 3: Recognizing the Inherent and Changing Nature of Costs • Resource Pools Start with an Inherent Cost Structure • As Resources are Consumed, the Nature of their Costs Change • Costs that are Initially Proportional by Nature can Change from Proportional to Fixed Based on Consumption Patterns • Allows Value Chain Modeling of Resource Cost Responsiveness

Connects Operations & Finance Operational View Financial View Resource/Resource Pools Intermediate Outputs Processes/Value Streams Products/Services Real Time Action Oriented Internally Focused FR Time Report Oriented Externally Focused