Download

1 / 91

910 likes | 1.07k Views

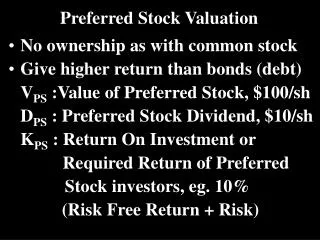

7- 1 Chapter 7 Preferred Stock. 7- 2 Preferred like debt and sometimes like equity. Dividend Rate Cumulative or not Participating Liquidation Preference Include accrued dividends? Voting Board Seat Special Events Conversion. 7- 3

E N D

7-1 Chapter 7 Preferred Stock

7-2 • Preferred like debt and sometimes like equity. • Dividend • Rate • Cumulative or not • Participating • Liquidation Preference • Include accrued dividends? • Voting • Board Seat • Special Events • Conversion

7-3 • Corporate Debt is a creature of contract. • What is Preferred Stock?

RMBCA § 7.21(a) - Voting Entitlement of Shares 7-4 • (a) Except as provided in subsections (b) and (c) or unless the articles of incorporation provide otherwise, each outstanding share, regardless of class, is entitled to one vote on each matter voted on at a shareholders’ meeting. Only shares are entitled to vote. • Del. § 212(a) Voting Rights of Stockholders: Proxies; Limitations • (a) Unless otherwise provided in the certificate of incorporation and subject to the provisions of section 213 of this title, each stockholder shall be entitled to one vote for each share of capital stock held by such stockholder. If the certificate of incorporation provides for more or less than one vote for any share on any matter, every reference in this chapter to a majority or other proportion of the stock shall refer to such majority or other proportion of the votes of such stock.

RMBCA § 6.01. Authorized Shares 7-5 • (b) The articles of incorporation must authorize: • (1) One or more classes or series of shares that together have unlimited voting rights; and • (2) One or more classes or series of shares (which may be the same class or classes as those with voting rights) that together are entitled to receive the net assets of the corporation upon dissolution. • (c) The articles of incorporation may authorize one or more classes or series of shares that: • (1) Have special, conditional, or limited voting rights, or no right to vote, except to the extent prohibited by this Act; • (2) Are redeemable or convertible as specified in the articles of incorporation: • (i) At the option of the corporation, the shareholder, or another person or upon the occurrence of a specified event; • (ii) For cash, indebtedness, securities, or other property; and • (iii) At prices and amounts specified, or determined in accordance with a formula; • (3) Entitle the holders to distributions calculated in any manner, including dividends that may be cumulative, noncumulative, or partially cumulative; or • (4) Have preference over any other class or series of shares with respect to distributions, including distributions upon the dissolution of the corporation.

Del. § 151(a). Classes and Series of Stock; Rights, etc. 7-6 • (a) Every corporationmay issue 1 or more classes of stock or 1 or more series of stock within any classthereof, . . . and which classes or seriesmay have such voting powers,full or limited, or no voting powers,and such designations, preferencesand relative, participating, optionalor other special rights, and qualifications, limitations or restrictions thereof,as shall be stated and expressed in the certificate of incorporation or of any amendment thereto, or in the resolution or resolutions providing for the issue of such stock adopted by the board of directorspursuant to authority expressly vested in it by the provisions of its certificate of incorporation. Any of the voting powers, designations, preferences, rights and qualifications, limitations or restrictions of any such class or series of stock may be made dependent upon facts ascertainable outside the certificate of incorporation or of any amendment thereto, or outside the resolution or resolutions providing for the issue of such stock …. provided that the manner in which such facts shall operate upon the voting powers, designations, preferences, rights and qualifications, limitations or restrictions of such class or series of stock is clearly and expressly set forth in the certificate of incorporation or in the resolution or resolutions providing for the issue of such stock adopted by the board of directors. * * *

Del. § 151(g) 7-7 • (g) When any corporation desires to issue any shares of stock of any class or of any series of any class of which the powers, designations, preferences and relative, participating, optional or other rights, if any, or the qualifications, limitations or restrictions thereof, if any, shall not have been set forth in the certificate of incorporation . . . but shall be provided for in a resolution or resolutions adopted by the board of directors pursuant to authority expressly vested in it by the certificate of incorporation . . ., a certificate of designations setting forth a copy of such resolution or resolutions and the number of shares of stock of such class or series as to which the resolution or resolutions apply shall be executed, acknowledged, filed and shall become effective, in accordance with § 103 of this title. * * * A certificate which (1) states that no shares of the class or series have been issued, (2) sets forth a copy of the resolution or resolutions and (3) if the designation of the class or series is being changed, indicates the original designation and the new designation, shall be executed, acknowledged and filed and shall become effective, in accordance with § 103 of this title.When any certificate filed under this subsection becomes effective, it shall have the effect of amending the certificate of incorporation; . . . .

Model Act, § 6.02 7-8 • (a) If the articles of incorporation so provide, the board of directors is authorized, without shareholder approval, to: • (1) classify any unissued shares into one or more classes or into one or more series within a class, * * * • (b) If the board of directors acts pursuant to subsection (a), it must determine the terms, including the preferences, rights and limitations, to the same extent permitted under section 6.01of: • (1) any class of shares before the issuance of any shares of that class, or • (2) any series within a class before the issuance of any shares of that series. • (c) Before issuing any shares of a class or series created under this section, the corporation must deliver to the secretary of state for filing articles of amendment setting forth the terms determined under subsection (a).

Del. § 104. Certificate of incorporation; definition7-9 • The term "certificate of incorporation," as used in this chapter, unless the context requires otherwise, includes not only the original certificate of incorporation filed to create a corporation but also allother certificates, agreements of merger or consolidation, plans of reorganization, or other instruments, howsoever designated, which arefiled pursuant to §§102, 133-136,151, 241-243, 245, 251-258, 263-264, 303, or any other section of this title, and which have the effect of amending or supplementing in some respect a corporation's original certificate of incorporation. • § 245. Restated certificate of incorporation • (a) A corporation may, whenever desired, integrate into a single instrument all of the provisions of its certificate of incorporation which are then in effect and operative as a result of there having theretofore been filed with the Secretary of State 1 or more certificates or other instruments pursuant to any of the sections referred to in § 104 of this title, . . . by adopting a restated certificate of incorporation. • (b) If the restated certificate of incorporation merely restates and integrates but does not further amend the certificate of incorporation, as theretofore amended or supplemented by any instrument that was filed pursuant to any of the sections mentioned in § 104 of this title, it may be adopted by the board of directors without a vote of the stockholders, . . . .

7-10 Constantin Cases • The Third Circuit decision holds that the dividends were mandatory if earned, while the New Jersey decision makes payment contingent on a declaration, using as authority a board resolution.

RMBCA § 6.40 Distributions to Shareholders 7-11 • (a) A board of directors may authorize and the corporation may make distributions to its shareholders subject to restriction by the articles of incorporation and the [solvency] limitation in subsection (c). • Del. § 170. Dividends; Payment; Wasting Asset Corporations • (a) The directors of every corporation, subject to any restrictions contained in the certificate of incorporation, may declare and pay dividends upon the shares of its capital stock … either (1) out of its surplus, as defined and computed in accordance with sections 154 and 244 of this title, or (2) in case there shall be no such surplus, out of its net profits for the fiscal year in which the dividend is declared and/or the preceding fiscal year.

L. L. Constantin & Co. Preferred Terms7-12 • “The holders of the preferred stock shall be entitled to receive, and the Company shall be bound to pay thereon, but only out of the net profits of the Company, a fixed yearly dividend of Fifty Cents (50 cents) per share, payable semi-annually.”

L. L. Constantin & Co. Preferred Terms7-13 1. How would a court be likely to decide the dispute over Constantin’s dividend obligations under RMBCA §§6.40 and 8.01(b)?

RMBCA § 6.40 7-14 • (a) A board of directors may authorize and the corporation may make distributions to its shareholders subject to restriction by the articles of incorporation and the limitation in subsection (c). • (b) If the board of directors does not fix the record date for determining shareholders entitled to a distribution (other than one involving a purchase, redemption, or other reacquisition of the corporation's shares), it is the date the board of directors authorizes the distribution. • (c) No distribution may be made if, after giving it effect: • (1) The corporation would not be able to pay its debts as they become due in the usual course of business; or • (2) The corporation's total assets would be less than the sum of its total liabilities plus (unless the articles of incorporation permit otherwise) the amount that would be needed, if the corporation were to be dissolved at the time of the distribution, to satisfy the preferential rights upon dissolution of shareholders whose preferential rights are superior to those receiving the distribution.***

Directors’ Authority 7-15 • RMBCA §8.01. Requirement for and Duties of Board of Directors • “(b) All corporate powers shall be exercised by or under the authority of, and the business and affairs of the corporation managed by or under the direction of, its board of directors, subject to any limitation set for in the articles of incorporation or in an agreement authorized under section 7.32.” • *

Constantin 7-16 2. How would the Delaware courts be likely to decide this question under Del. Gen. Corp. L. §§ 141 and 170?

Directors’ Authority 7-17 • Del. § 141: • (a) The business and affairs of every corporation organized under this chapter shall be managed by or under the direction of a board of directors, except as may be otherwise provided in this chapter or in its certificate of incorporation. * *

Directors’ Authority 7-18 • Del. GCL § 170(a) provides: • (a) The directors of every corporation, subject to any restrictions contained in its certificate of incorporation, may declare and pay dividends upon the shares of its capital stock, or to its members if the corporation is a nonstock corporation, either (1) out of its surplus, as defined in and computed in accordance with §§ 154 and 244 of this title, or (2) in case there shall be no such surplus, out of its net profits for the fiscal year in which the dividend is declared and/or the preceding fiscal year. If the capital of the corporation, computed in accordance with §§ 154 and 244 of this title, shall have been diminished by depreciation in the value of its property, or by losses, or otherwise, to an amount less than the aggregate amount of the capital represented by the issued and outstanding stock of all classes having a preference upon the distribution of assets, the directors of such corporation shall not declare and pay out of such net profits any dividends upon any shares of any classes of its capital stock until the deficiency in the amount of capital represented by the issued and outstanding stock of all classes having a preference upon the distribution of assets shall have been repaired. Nothing in this subsection shall invalidate or otherwise affect a note, debenture or other obligation of the corporation paid by it as a dividend on shares of its stock, or any payment made thereon, if at the time such note, debenture or obligation was delivered by the corporation, the corporation had either surplus or net profits as provided in clause (1) or (2) of this subsection from which the dividend could lawfully have been paid.

Constantin 7-19 3. Why would a company commit to a preferred stock with a dividend that was mandatory if earned? Why not issue corporate bonds instead?

Constantin 7-20 3. Why would a company commit to a preferred stock with a dividend that was mandatory if earned? Why not issue corporate bonds instead? • The tax treatment might explain it. A corporate holder might prefer dividends to interest. • Preferred stock can be given voting rights, while debt only gets negative covenants.

Constantin 7-21 4.Assuming that there is an ambiguity in the Constantin language governing dividends on the preferred stock, would the following provisions resolve that ambiguity?

Alternative Dividend Language 7-22 • “The holders of first preferred shares will be entitled to receive semiannually or quarterly all net earnings of the corporation determined and declared as dividends in each fiscal year up to but not exceeding ___ percent per annum on all outstanding first preferred shares before any dividend will be set apart or paid upon any other shares of the company.” • “Dividends upon the Series B Preferred Stock shall be paid out of funds legally available therefore, annually beginning on August 1, 2001, at the rate per annum of $.27 per share (annually the "Mandatory Dividend") and collectively the "Mandatory Dividends"). In addition, commencing on August 1, 2001, the holders of Series B Preferred Stock shall be entitled to receive, out of funds legally available therefore, additional annual dividends at the rate per annum of $.27 per share (the “Elective Dividend" and collectively the "Elective Dividends"), when, as and if declared by the Board of Directors. Elective and Mandatory Dividends (the "Series B Accruing Dividends") shall accrue from day to day, whether or not earned or declared, and shall be cumulative, from August 1, 2001.”

Guttman v. Illinois Central Railroad Co.7-24 • A preferred shareholder sued to stop the payment of 1950 dividends to the common stock, without payment of arrearages on preferred. • Trial Court apparently denied relief. Affirmed. • Charter provision:

Illinois Central Dividend Provision 7-25 • Dividends at 7% “out of the surplus or net profits of the Company, in each fiscal year...as shall be determined by the Board of Directors..... No dividends shall be paid, ... on the common... in any fiscal year, unless the full dividend on the preferred stock for such year shall have been paid or provided for.”

Guttman 7-27 • No dividends were paid 1932-1948. • In 1937-1948 the company annually had sufficient profits to pay preferred dividends. • But the board took a cautious position and didn’t pay any dividends. • Can the Board declare and pay a dividend on the common in 1950, after declaring a dividend on the preferred for 1950, without paying arrearages? Yes.

Guttman 7-28 1. What justifies passing preferred non-cumulative dividends when the company has sufficient profits to declare and pay them?

Guttman 7-29 1. What justifies passing preferred non-cumulative dividends when the company has sufficient profits to declare and pay them? • A justifiable application of profits to capital improvements or other uses. • This is the business judgment rule.

Guttman 7-30 2. Is there any limit on the kinds of investments of profits a company can make when it passes on preferred dividends?

Guttman 7-31 2. Is there any limit on the kinds of investments of profits a company can make when it passes on preferred dividends? • No. The court declines to distinguish between kinds of capital outlays the board can make. It uses the example of a purchase of land that turns out not to be needed. When it sells the land, it does not owe back dividends.

Guttman 7-32 3. Does this mean the board has complete discretion about paying preferred non-cumulative dividends, as long as it acts in good faith?

Guttman 7-33 3. Does this mean the board has complete discretion about paying preferred non-cumulative dividends, as long as it acts in good faith? • Yes. This is really the Business Judgment Rule.

Guttman 7-34 4. Why doesn’t the court exercise its equitable powers to provide some rights to passed dividends, when past profits are available?

Guttman 7-35 4. Because a contract is a contract is a contract. Preferred shareholders are not wards of the judiciary, “like sailors or idiots or infants.” • Because of the position of preferred shareholders when dividends are non-cumulative, most contracts provide some protection for preferred. • Typically this is the right to elect directors, if preferred doesn’t normally have that right. • NYSE Listed Company Manual, §703.05D requires giving preferred the power to elect at least 2 directors if 6 quarterly dividends are passed. • This is common practice, after missing 4 to 6 quarterly dividends.

FNX 7-36 4. As converted voting with the common and some special class votes.

Guttman 7-37 5. Does the statement of the board’s discretion to omit dividends on preferred stock differ in any significant way from the rule for common stock that you can discern?

Guttman 7-38 5. Yes, in one sense. • Citing Wabash Ry. Co. v. Barclay, the court held that once non-cumulative dividends had passed, the board had no discretion to pay any more than the current year’s dividend. • With common stock, the board can pay as large or small a dividend as it chooses. • In another sense, there is little difference between common and preferred. So long as the board has uses for the funds. • The court rejected a proposed rule that would only have allowed the board to pass preferred dividends if it had investments in tangible property.

Guttman 7-39 6. Recall the rules of interpretation for corporate bonds set forth in Metropolitan Life Insurance Company v. RJR Nabisco, Inc., 716 F. Supp. 1504 (S.D.N.Y. 1989) in Chapter Six, Part 3.A. Does this opinion suggest rules governing interpretation of preferred stock contracts are closer to those of corporate debt or common stock? Does any rationale suggest itself for such an approach?

Guttman 7-40 • The court emphasizes the contract language, suggesting that the preferred’s rights are largely, if not exclusively, contractual. • Note the statement that the court is “interpreting a contract into which uncoerced men entered.” - page 463. • “...it may not be inappropriate to paraphrase a modern poet and to say that ‘a contract is a contract is a contract.’” - page 463. • The fact that it may be a bad contract doesn’t empower the court to revise it. - page 464.

Guttman 7-41 • The court doesn’t discuss any rationale for its result, but there are several possible reasons. • (1) Imposing a rule that is fact intensive – that depends on the particular type of “worthy” investments made by the board – would reduce certainty for investors. • (2) Most preferred stock is held by corporate & institutional investors today, because of the dividends received tax deduction, and they, like Metropolitan Life, are able to look out for themselves.

Guttman 7-42 • Straight preferred is very risky. Board can pass dividends for years than pay the stated dividend and a massive common dividend which has been storing up.

New Jersey’s Dividend Credit Rule 7-43 • Doctrinal rationale:“Non-cumulative” only means that if there are no earnings in a year, the opportunity for a preferred dividend for that year is lost. - Dohme v. Pacific Coast Co., 5 N.J.Super. 477, 68 A.2d 490 (1949). • When directors fail to declare a dividend in a year in which there are profits, shareholders have an “inchoate right” to a dividend from those profits, before dividends are declared on the common. Id. • Policy rationale:“There seems to be little doubt that equitable factors did play a significant part in the development of New Jersey’s doctrine.” - Sanders v. Cuba Railroad Co., 21 N.J. 78, 120 A.2d 849, 852 (1956). • If the common stockholders can pass on preferred dividends for a few years “without any dividend credit consequences, then the preferred stockholders will be substantially at the mercy of others who will be under temptation to act in their own self-interest.”

New Jersey’s Dividend Credit Rule 7-44 • No other jurisdictions have followed this rule!!!

Hay v. Hay –Preference Clause 7-45 • “(a) The holders of the preferred stock shall be entitled to receive, when and as declared by the Board of Trustees of this Corporation, cumulative dividends thereon . . . At the rate of six (6%) per annun and no more,payable out of the surplus profitsof this Corporation annually … before any dividend shall be paid or set apart for the common stock . . . .” • “(d) In the event of any liquidation, dissolution or winding up of the Corporation the holders of the preferred stock shall be entitled to be paid in full the par value thereof,and all accrued unpaid dividends thereonbefore any sum shall be paid to or any assets distributed among the holders of the common stock, but after payment to the holders of the preferred stock of the amounts payable to them as hereinbefore provided, the remaining assets and funds of the Corporation shall be paid to and distributed among the holders of the common stock.”

Hay v. Hay –Preference Clause 7-46 • The company never declared and preferred dividends and never had any surplus from which dividends could have been paid. • Question: Is the preferred entitled to payment of passed dividends? Yes.

Hay v. Hay 7-47 1. The dissenting judge stated that “the capital stock or assets of The Big Bend Land Company belong to the common stockholders.” What does he mean by this?

Hay v. Hay 7-48 • The dissenting judge stated that “the capital stock or assets of The Big Bend Land Company belong to the common stockholders.” What does he mean by this? • It’s hard to know. Corporations are nexuses of contractual relationships, in Jensen & Meckling’s language. • In dissent, Judge Grady seems to be working with a default model that starts with common stockholders, who then cede certain rights to other claimants, which are to be interpreted strictly against them.

Hay v. Hay 7-49 2. The dissenting judge also stated that if there were profits and “dividends were made, but were not paid to the stockholder ... he would have a preference right over common stockholders later to have them paid to him. Such dividends would be the property of the corporation, and when ultimately paid would not be as dividends, but as corporate funds.” What does he mean by this?

Hay v. Hay 7-50 2. First, he misstates the legal status of the preferred shareholder once a dividend is paid. They becomes creditors. • He seems to compound the error when he says the dividend is the “property of the corporation,” when the preferred shareholder is a creditor.