Download

1 / 11

110 likes | 322 Views

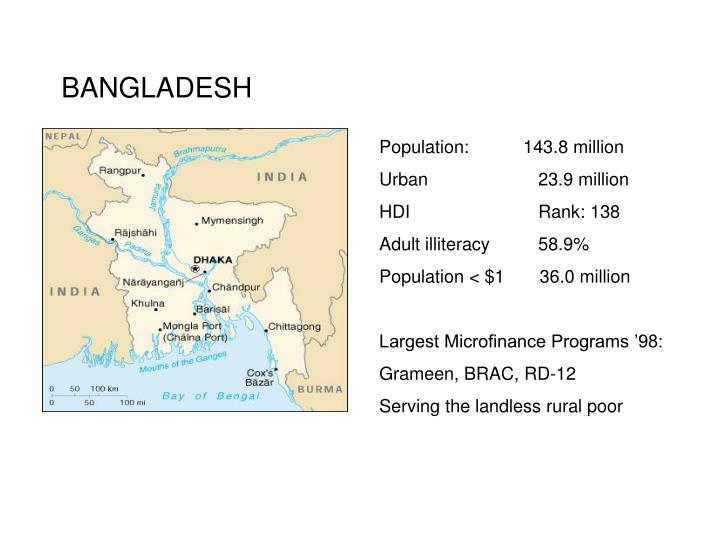

BANGLADESH. Population: 143.8 million Urban 23.9 million HDI Rank: 138 Adult illiteracy 58.9% Population < $1 36.0 million Largest Microfinance Programs ’98: Grameen, BRAC, RD-12 Serving the landless rural poor . Pitt and Khandker (1998).

E N D

BANGLADESH Population: 143.8 million Urban 23.9 million HDI Rank: 138 Adult illiteracy 58.9% Population < $1 36.0 million Largest Microfinance Programs ’98: Grameen, BRAC, RD-12 Serving the landless rural poor

Pitt and Khandker (1998) • Attempt to measure the impact of microfinance participation, by gender on: - boys’ and girls’ schooling - household expenditures (consumption) - accumulation on non – land assets - women’s and men’s labor supply

Cross – Section Data: • 1,798 households in 87 villages were surveyed in 1992 • 905 households were under a microfinance program← treatment • 893 households were not ← control Results: Relative to credit provided to men, credit provided to women: (a) ↑Schooling (both boys and girls) (b) ↑Household expenditures (consumption) (c) ↑Non-land assets held by women (d) ↓Labor supply of men and women

Problem: • How to address the biases? Find an IV: a variable that explains levels of credit received but has no direct relationship with the outcomes of interest In this case: Schooling, Household Expenditures, Non Land Assets, Labor supply “An eligibility rule: only “functionally landless” households (with < ½ of land) can have access to microfinance” The fact that there ineligible households (260) within villages with programs → there is another “control” group which helps to alleviate the bias

An improved estimation strategy • Compare: • Treatment with ineligible households living in the same village • Ineligible with “would be” eligible → households with access to microfinance are doing better than their ineligible neighbors relative to the difference in outcomes between functionally landless households in control villages versus their ineligible neighbors

Yij = Xij α + Vj β+ Eij γ + (Tij• Eij) δ’ + ηij, (8.5) Disappointing results w/r to impact on household consumption But: Microfinance helps to diversify income streams so that consumption is less variable across seasons Also: Landholdings may not be “exogenous” On the other hand Successful borrowers were buying land → may explain why no impact on household consumption ☺ Moreover, debate over ineligible households that participated (25%). But Pitt-Khandker (1999) acknowledged the problem, made robustness checks and show that their results change very little ☺

Note that: Yij = Xij α + Vj β+ Eij γ + Cij δ” + ηij, (8.6) Where: δ” captures credit “access” Now, by expanding the set of instruments to Xij•Tij• Eij → there are as many instruments as there are X (education….) → δ” takes advantage of variation of how much credit households receive

Now, when comparing groups of men with groups of women Pitt-Khandker (1998) most cited result: For every 100 taka lent to a woman consumption ↑ 18 taka For every 100 taka lent to a man consumption ↑11 taka Now, another round of data was collected in 1998 – 1999 And Khandker (2003) to see the trends

20 per cent poverty decline both participants and nonparticipants Pessimists: decline would have happened even without microfinance Optimists: impact of microfinance has had positive spillovers to nonparticipants

Khandker’s (2003) econometric estimates show that: • Microfinance contributed to roughly ½ of the 20 percentage points decline in poverty • For every 100 taka lent to a woman consumption ↑8 taka Ideally, another round of data collection should help Problem: microfinance in Bangladesh has spread far and wide → No more control groups!!! Have a great weekend and good luck on the midterm☺ → Next Class: DR, Chap 8 and the article by Coate