Download

1 / 24

240 likes | 394 Views

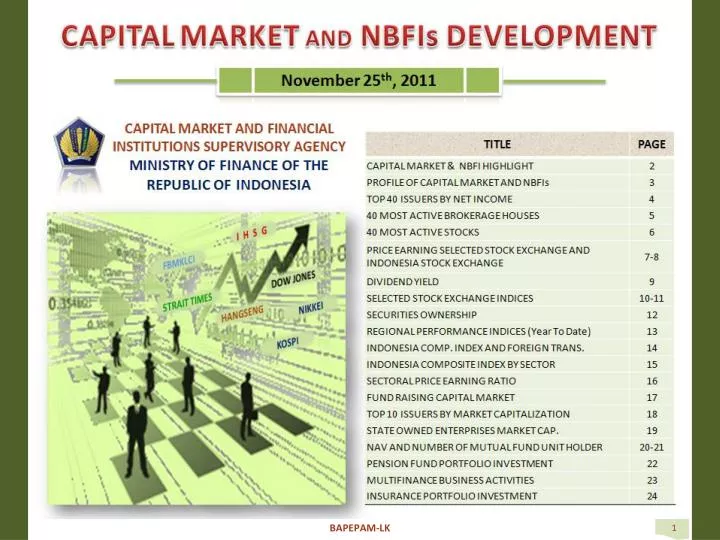

CAPITAL MARKET AND NBFI HIGHLIGHT End of December 2008 – November 25 th ,2011. *) audited * * ) Per July 2 0 1 1 unaudited. Source: Bapepam-LK, Bloomberg, IDX, E-Monitoring.

E N D

CAPITAL MARKET AND NBFI HIGHLIGHT End of December 2008 – November 25th ,2011 *) audited **) Per July2011 unaudited Source: Bapepam-LK, Bloomberg, IDX, E-Monitoring • Indikatorutamapasar modal danlembagakeuanganbukan bank yang menunjukkanperkembangan IHSG, kapitalisasipasar, rasiokapitalisasipasarterhadap GDP, obligasi (korporatdanpemerintah) yang beredar, aktivabersihreksadana, jumlahperusahaan yang menerbitkansahamdanobligasi, aktivabersihdanapensiun, kegiatanpembiayaan, dan total nilaiasetasuransi. BAPEPAM-LK

Profile of Indonesian Capital Markets and NBFIs November 25th ,2011 • Capital Markets (November 25th 2011): • 434 listed companies at Indonesia Stock Exchange with market capitalization reached Rp 3,348.75 trillion (52.14% of GDP 2010) • In 2010, 188 corporate bond issuers with total value of issuance at Rp215.13 trillion (3.35% of GDP 2010) – In 2011, there is 29 corporate bond issuance (Rp30.663 trillion) and 1 corporate bond issuance (USD 80 million) • 99 Inv Mgrs and 647 Mutual Funds with NAV of Rp162.83 trillion (2.54% of GDP 2010) • 147 Securities Firms • Average Daily Trading Value at IDX is Rp5.10 trillion/day • 141 Insurance Companies (Q1-2011/Unaudited): • Assets = Rp399.69 trillion (6.22% of GDP 2010) • Investment = Rp356.32 trillion (5.55% of GDP 2010) • 272 Pension Funds (2010): • Net Assets = Rp130.48trillion (2.03% of GDP 2010) • Investment = Rp125.72 trillion (1.96% of GDP 2010) • 194 Multifinance Companies (July 2011/Unaudited): • Total asset = Rp266.46 trillion (4.15% of GDP 2010) • Financing Activity = Rp217.54 trillion (3.39% of GDP 2010) Source: Bapepam-LK, Notes: GDP 2010 = Rp.6422 triliun • Profil jumlah emiten, manajer investasi, dan perusahaan efek per 25 Nopember2011; perusahaan asuransi per triwulan I-2011, dana pensiun per 2010, dan perusahaan pembiayaan per Juli 2011. BAPEPAM-LK

Source: Stockwatch BAPEPAM-LK

Source: Stockwatch BAPEPAM-LK

PRICE EARNING RATIO SELECTED STOCK EXCHANGE January 1st ,2008 - November 25th,2011 (Daily) Source: Bloomberg • Perbandingan gerakan rasio harga dengan earning (kali),beberapa bursa diluar negeri, dari 1 Januari 2008 sampai 25 Nopember 2011. BAPEPAM-LK

INDEX AND PRICE EARNING RATIO INDONESIA STOCK EXCHANGE January 2010 - November 25th, 2011 (Daily) Composite Index: 3,637.19 Average PER: 11.13 Source: Indonesia Stock Exchange • Perbandingan gerakan Indeks dan rasio harga dengan earning, Bursa Efek Indonesia, dari bulan Januari 2010 sampai 25 Nopember 2011 (Harian). BAPEPAM-LK

DIVIDEND YIELD SELECTED STOCK EXCHANGE January 1st, 2008 - November 25th, 2011 (Daily) Source: Bloomberg • Perbandingangerakan dividend yield, antara bursa efek Indonesia (JCI) denganbeberapa bursadiluarnegeri, dari 1 Januari 2008 sampai25 Nopember 2011 (dalamprosentase). BAPEPAM-LK

SELECTED STOCK EXCHANGE INDICES January 1st, 2008 – November 25th, 2011 JCI end down 58.840 point or 1,59% at 3,637.19 as foreign funds continue to reduce their local exposure amid worries that the European debt situation may take a turn for the worse. Source: Bloomberg • Perbandingangerakan IHSG denganbeberapaindeks bursa diluarnegeridari 1 Januari 2008 sampai25 Nopember 2011 BAPEPAM-LK

PERFORMANCE SELECTED STOCK EXCHANGE INDICES January 4th, 2010 – November 25th, 2011 Source: Bloomberg • Perbandingan presentase perubahan (dari 4 Januari 2010 sampai 25 Nopember 2011),antara IHSG (JCI), dengan beberapa indeks bursa diluar negeri. BAPEPAM-LK

SECURITIES OWNERSHIP December 2004 – November 24th2011 • Komposisi kepemilikan antara pemodal dalam negeri dan pemodal luar negeri untuk saham, obligasi korporasi dan Obligasi Pemerintah dari Desember 2004 sampai 24 Nopember 2011. BAPEPAM-LK

Regional Performance IndicesDec. 2008; Dec. 2009, Dec. 2010; November 25th, 2011 Source: Bloomberg • Perbandingan nilai IHSG (JCI Indonesia) dengan beberapa indeks bursa di luar negeri pada Desember 2008, Desember 2009, Desember 2010 dan 25 Nopember 2011. BAPEPAM-LK

INDONESIA COMP. INDEX AND FOREIGN TRANSACTIONJanuary 2009 – November 25th, 2011 (Monthly) JCI Index : 3,637.19 Net Buy IDR : 529.510 (billion) Source: Bloomberg • Perbandingan antara gerakan IHSG dengan nilai transaksi jual dan beli pemodal asing, di bursa efek Indonesia, dari Januari 2009 sampai 25 Nopember 2011 (Bulanan). BAPEPAM-LK

INDONESIA COMPOSITE INDEX BY SECTOR December 31st 2010 – November 25th, 2011 (Year to date) Source: Bloomberg • Komposisi dari IHSG per sektor dalam prosentase, dari Desember 2010 sampai 25 Nopember 2011. BAPEPAM-LK

SECTORAL PRICE EARNING RATIO (Times) Dec. 31st , 2008; November 25th, 2011 Source: Bloomberg *) as of June 14th 2010 • Rasio harga dan earning berdasarkan sektor, dari 31 Desember 2008 sampai 25 Nopember 2011. BAPEPAM-LK

FUND RAISING FROM CAPITAL MARKET 2007 - 2011 Source: Bapepam-LK and DMO • Perkembanganjumlahperusahaansertanilaidana yang diperoleh, melaluipenawaranumumsaham, penawaranterbatassaham, obligasikorporat, danobligasipemerintah, pada 2007,2008, 2009, 2010 dan • 25 Nopember 2011. (Lampiran Num. of Issuers, hal. 25 dan 26) BAPEPAM-LK

TOP 10 ISSUERS BY MARKET CAPITALIZATION November 25th, 2011 Source: Bloomberg • Daftar 10 perusahaan terbesar di bursa efek Indonesia berdasarkan nilai kapitalisasi pasar(dalam triliun rupiah) pada 25 Nopember 2011. BAPEPAM-LK

STATE OWNED ENTERPRISES MARKET CAPITALIZATION November 25th, 2011 Source: Bloomberg • Daftar 18 BUMN berdasarkan nilai kapitalisasi pasar terbesar (dalam triliun rupiah) di Bursa EfekIndonesia pada 25 Nopember 2011. BAPEPAM-LK

NAV OF MUTUAL FUND 2004 -November 24th ,2011 Source: E-monitoring Reksa Dana • Perkembangannilaiaktivabersihreksadana (dalamtriliun rupiah) berdasarkanjenisnya, dari 2004 sampai • 24 Nopember2011. (data KebijakanInvestasiReksa Dana terlampirdihal. 28) BAPEPAM-LK

NUMBER OF MUTUAL FUND UNIT HOLDER 2004 – 2011 Source: E-monitoring Reksa Dana • Perkembangan jumlah pemegang unit reksadana berdasarkan kepemilikan dalam negeri dan kepemilikan • luar negeri, dari 2004 sampai Agustus 2011. BAPEPAM-LK

SUMMARY OF PENSION FUND NET ASSET (Trillion IDR) End of 2006– 2010 Source: BapepamLK * ) Deposito + Deposito on call + SertifikatDeposito ** ) Sukuk + Tabungan • Perkembangan jumlah dana pensiun (unit); nilai aktiva bersih (triliun rupiah) dari2006 sampai 2010. BAPEPAM-LK

SUMMARY OF MULTIFINANCE BALANCE SHEET (Trillion IDR) Period 2006 – July2011 Source: LBPP • Perkembangan jumlah perusahaan pembiayaan (unit); Neraca bulanan Perusahaan Pembiayaan (triliun rupiah) dari 2006 • sampai Juli2011. BAPEPAM-LK

SUMMARY OF INSURANCE ASSET 2006 – 1st Quarter 2011 (Trillion IDR) • Perkembangan jumlah perusahaan asuransi (unit); nilai aset, investasi dan non investasi (triliunrupiah), dari 2006 sampai triwulan I 2011. BAPEPAM-LK