Download

1 / 9

90 likes | 333 Views

BAB 6 Kertas Kerja. Pengertian. Working Paper is auditor’s record of: Information or evidences obtained Procedures applied Test performed Conclusion reached. Tujuan. Kell & Boynton (2000): Principal support for auditor report Evidence that examination was made in accordance with GAAP

E N D

Pengertian Working Paper is auditor’s record of: • Information or evidences obtained • Procedures applied • Test performed • Conclusion reached

Tujuan Kell & Boynton (2000): • Principal support for auditor report • Evidence that examination was made in accordance with GAAP • Means for coordinating and supervising the examination

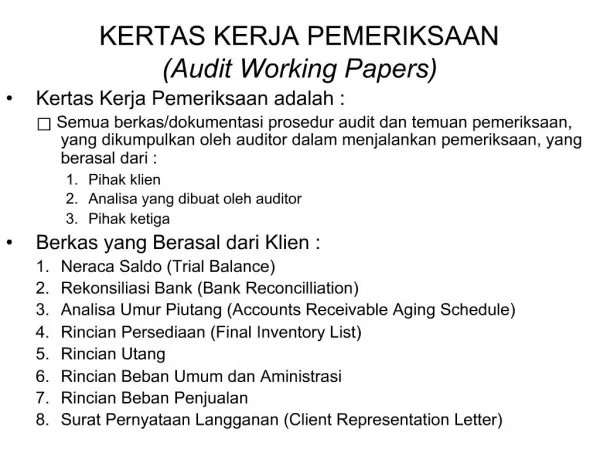

Penggolongan KK • Neraca saldo • Schedule utama (grouping sheet) • Jurnal Penyesuaian dan reklasifikasi • Supporting schedule • Analisis • Rekonsiliasi • Ikhtisar hasil prosedur audit • Dokumen dari pihak luar

Pengarsipan • Arsip permanen • Data historis • Referensi untuk hal-hal yang kontinyu dan berulang • Mengurangi pekerjaan audit • Data bagi audit yang akan datang

Pedoman Pembuatan • Bertujuan • Hanya satu muka • Judul • Berindek • Pernyataan semua prosedur yang dipakai • Kesimpulan (komentar auditor)

Tanda Audit • V (kanan angka dari suatu jurnal) • \I\ (di bawah penjumlahan vertikal ataupun horisontal) • VV (di samping suatu jumlah dalam rekening buku besar) • ^ • = (di bawah jumlah total suatu kolom penjumlahan) • 0 (disamping nilai suatu cek dalam cek regis) • O (di samping nilai suatu cek yang masih beredar) • $ • /- (di samping angka pada tembusan bukti setoran bank) • ? (di samping kanan suatu angka atau komentar)

Pemberian Indek • Metode I (nomor urut pada KK utama, sub nomor pada KK pendukung) • Metode II (alfabet untuk KK utama, angka untuk KK pendukung) • Metode III (double huruf pada semua skedul bukan keuangan, unit ratusan untuk skedul keuangan diikuti huruf untuk pendukungnya) • Metode IV (nomor urut sesuai penyajian dalam LK)

Kepemilikan KK • Milik auditor • Dijaga kerahasiaanya • Disimpan not less than 10 years