Download

1 / 18

190 likes | 354 Views

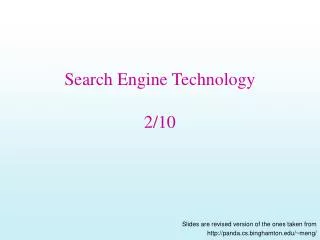

New Information Technology Paradigms and Korean IT Competitiveness…. KITA Q3 Seminar September 12th ,2006 Sheraton Cerritos Hotel. Jong-Hoon Lee Chief Executive Officer iPark Silicon Valley jhlee@iparksv.com. $35. $30. BILLIONS OF DOLLARS. $25. $20. $15. $10. $5. $0.

E N D

New Information Technology Paradigms and Korean IT Competitiveness… KITA Q3 Seminar September 12th ,2006 Sheraton Cerritos Hotel Jong-Hoon Lee Chief Executive Officer iPark Silicon Valley jhlee@iparksv.com KITA Q306 Seminar

$35 $30 BILLIONS OF DOLLARS $25 $20 $15 $10 $5 $0 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 Silicon Valley is the Center of VC Investment TOTAL VENTURE CAPITAL FINANCING IN SILICON VALLEY FIRMS KITA Q306 Seminar

What’s going on IT Market Battle Field? • Economic indicators: a “mixed bag” -- positive but still cautious about high tech & impact of interest rate hikes, high oil price and War on terror in 2006 - North American IT spending grew 5.4% in 2005 reaching $892B - Silicon Valley 150 record 2004 profits of $31.4B (up 170%) and sales of $336B (up 14%) - VC’s are optimistic and are beginning to invest again. 117 IPOs in 2005 quintupled the 23 IPOs in 2004. Mobility, Web 2.0 and recently Video are hot areas - Signs of slow “Jobless recovery”. The trends of “Outsourcing IT” to China & India. The job market for IT specialists will shrink 40% by 2010 • Convergence between computing devices and appliance will be in full swing: - Personal utility: cell phone + PDA + MP3 + digital camera; - Home Digital Appliance : wireless networking + appliance/security controller + remote access) - Video streaming and broadcast appearing in increasing number of devices - The Consumer Market becoming a larger part of IT industry • Telecom industry is stagnant, but major consolidation/M&As is going on: - Cable & Phone co’s fighting for control of the home: phone, broadband & TV packages - Smart phone/Digital Camera markets are growing fast but still waiting for killer applications - Broadband & VOIP gaining market momentum. Fixed-line carriers face pressure from VoIP • The margins for electronic commodity products are thinner than ever forcing large resellers to restructure to stay afloat. Major challenges ahead from Chinese Manufacturers along with the impact of the weak dollar in 2005 KITA Q306 Seminar

Silicon Valley has been a driving force of IT revolution for the last 50 years KITA Q306 Seminar

Silicon Valley led IT evolution with disrupting technologies..Can it continue the same trend in 2000’s and beyond? The Valley garners a third of all U.S. venture capital funding, according to the National Venture Capital Association (NVCA). 4000 IT companies with IT related revenue about $200B KITA Q306 Seminar

Traditional Paradigms of Silicon ValleyBefore Dot-com burst (1960-2000) • Huge focus on R&D: 8-20% of total revenue • Hi-technology, Hi-technology – Epicenter of disrupting technologies • Disrupting Technologies: Semiconductor, Microprocessor, PC, Software, Internet… • Core Competitive advantage of America: Genius Scientists/Architect level engineers vs Mfg/Design Engineers • High Profit margin • Lead the world with breakthrough IT products • Product Concept – Proof – Design – Mfg – Worldwide distribution all by Silicon Valley • Soft-landing to the higher industry value chain: • Collapse of manufacturing – 90’s • Soft landing to high paying engineering job: Software, Network $100K+ • Lack of hi-tech engineers – Foreign engineering talents. IC = India, China KITA Q306 Seminar

New IT Paradigm: Beyond 2000The Impact of Internet and Globalization is Changing Silicon Valley Future Convergence, Globalization Past Silicon Valley=Tech Innovation ◈ Silicon Valley is the epicenter of disruptive technologies (Semiconductor, CPUs, PC, S/W …) . Technology Centric . Long R&D Cycle . Big R&D investment, 8-20% of Rev ◈ Digital Convergence is the new trend Mobile phone, Digital TV, Ubi-network .Biz model Centric – Google, Dell, MS.. .Speed becomes more critical . Barrier to entry is relatively low ◈ Major revenues from enterprise-driven products: . Mainframe, PC, Unix Servers.. ◈ Consumer Electronics Centric ◈ SV Leads the world with Technology leadership . Concept- Engineering –Mfg - Marketing ◈ Asia come with trendy products faster . Mobile, Contents, Conumer Electronics . Korea, Asia become major test bed ◈ Selective outsourcing – Offshore R&D ◈ Focus on core technologies/integration ◈ Foreign born work force majority in SV ◈ Manufacturing moved away ◈High-paying engineering jobs ► The next Gold Rush will be in Digital Convergence ►Asia will be a major driving force KITA Q306 Seminar

What does this Paradigm Shift mean to Korean IT Industry?Korea wants to be a center of innovation in Digital Convergence Huge Opportunities Ahead • Korean Business culture is a perfect match for the “new world” - Speed, Risk-taking, Ongoing product enhancement • Korea is best positioned to develop Digital convergence products - Excellent Industry positioning, RND & Production facilities - Optimum test-bed for new technologies (users & infrastructure) • Conglomerates like Samsung, LG will continue its dominance in the short run • New Internet culture, Tech-Savvy consumers … And Major Challenges • Worldwide competitors in commodity products • China: Technology, manufacturing, India: Software, Labor … • How to move to a higher country value chain? • Need innovative core technologies to stay ahead of commoditization • How to foster the development of SMEs • Most lack international sales experience • Often RND driven instead of market driven KITA Q306 Seminar

Next Steps for Korean IT Industry:Key questions that need to addressed • What’s the Next Business Model for Korea? - 60-70’s: Labor Intensive Industry, 80-90’s: Heavy Industry, 2000’s: ???? • Long-term IT Strategies * How to create Core Technologies? - Issue ofEducation Infrastructure, Biz Culture - DMB/Wibro can be a first test case for Korea’s new challenges • Short to Mid-term IT strategies * China Strategy - MFG take over by China - How to create high-paying job in Korea? - How to differentiate with commodity based Chinese products? New Cash Cow industry -- IT 8-3-9…. * How to boost small to medium-size IT companies? KITA Q306 Seminar

’05 Worldwide IT Exports By Korea 2005 Worldwide IT Export $78B 2004 Worldwide IT Export $74B KITA Q306 Seminar

Next Gen. Wireless/Mobile Devices Intelligent Home Network Appliance servers, Post PC IT SoC Consumer Electronics Embedded S/W Games Online Mobile Network US MARKET Opportunities Digital Contents Vertical Solution S/W D/T Utility S/W Linux based packaged S/W Packaged S/W System Integration iPark SV Sweet Spot (Current)Mfg/Commodity Takeover by China: Seek higher value chain - Build up key success factors for Enterprise solutions, Software&Middleware in ubiquitous network - Maximize Korean IT core competence, better ROI, quicker results, and New Growth Engines • e-Gov solutions • POS solutions • Education solutions • Latin American market KITA Q306 Seminar

Key Issues to address - Korean IT Companies (1)Small to medium size typical ventures companies iPark deals with • Enthusiasm for key Technologies/Product Features • Product/Technology Centric Approach vs Customer Value/Demand • Vs Taiwanese ventureswho have root in Silicon Valley • Lack Marketing expertise with CEOs mostly R&D background • Common Issues of US Marketing Approaches: • Vague Product Positioning • Lack of Competitive Analysis • No Brand recognition • Unclear target segment • Little or No understanding of US Channel Structure • Entry Price, Market driven pricing • Psychological & Cultural Barrier for US market • Only a Few ready for US entry • Stage of company maturity (no full span of products) • Financial support (Mktg, Channel Dev, Post-support ) • Experience of Mgmt team (i.e., CEO) • Almost no ideas on next steps… KITA Q306 Seminar

Key Issues to address - Korean IT Companies (2) Why They failed? Every Step Can Be A CHASM Unless Obstacles are Removed Revenue growth Set up MKTG & Sales operations Target the right market segments Penetrate proper channels Close deals • Localization • Packaging • Local Operation & Offices • Local Staffing • Support Infrastructure • Value Chain Understanding • Competitive Analysis • Identifying penetration segment • Differentiators • Product Positioning • Market driven Pricing • Introductory PR • Trade Shows • Incentive Schedule • Tactical Channel Plan • Setting up Sales Team • Channel Networking • Promotion • Training of Support Team • HQ Support for Deals • Incentive Management Most Korean IT companies failed to cross the chasm in the US. KITA Q306 Seminar

Singapore What is iPark? iPark is a non-profit organization designed to promote Korea’s best IT products London Tokyo Beijing Boston Silicon Valley Osaka Shanghai KITA Q306 Seminar

$1 Billion New iPark Business Model Transition to the Next Phase (2006-2010) iParkSV Revenues Goal: $1 Billion in US Revenues by 2010 SV150 VCs Strategic Partnerships R&D Center IT 8-3-9 IR Market Intelligence MIC Strategic Initiatives Industry Marketing – Korea Country Marketing Tier I Shared Service Model Nasdaq, M&A, Funding, Tech Partners (Phase II: 2004 and beyond) Marketing &Promotion Incubation 30 Tenant Companies Client Satisfaction Basic Client Marketing, Referral Services (Phase I Focus: 2000-2003) Operations KITA Q306 Seminar

Recent Highlights GIO Forum Opened a doorway to U.S. and global IPO opportunities • NASDAQ listings • 2 iPark Silicon Valley client companies • Pixelplus: CMOS imaging sensors solution • Leadis: Small panel display enhancement solution International Cooperation DMB/WiBro MOU between Alberta Canada and iPark Silicon Valley Telecom Service Providers Investment Forum Connect IT Korea to top U.S. telecommunications service providers and venture capital firms VC Circle Connect IT Korea to top 50 U.S. venture capital firms Awards High Tech Businessmen of the Year - KACC International Business Development – Gartner International Partnership – IT Channel Vision Best Software Product – Retail Vision Best Product – Retail Vision AMD R&D center in Korea Induced and steered AMD R&D center establishment in Korea KITA Q306 Seminar

Target Industry Segments Consumer Electronics Digital, LCD TVs MP3 DVRs PC Accessories Cameras PDA, GPS Broadband/Networking VoIP Home Networking Network Equipment Wireless Mobile Set Top Box 8-3-9 E/S DC BcN VoIP IPv6 Home Networking IT SoC RFID NextGen PC Digital TV NG Mobile WiBro DMB Telematics Service Robot Digital Content IT SoC (Semiconductors) Mobile Multimedia Other Open Source Embedded Software SI Latin America Application Software Security Web Editing PC Suite Embedded S/W Packaged S/W Digital Contents System Integration 2004 2005 -2006 2007-2008 KITA Q306 Seminar

Mission – iPark Silicon Valley “Our mission is to establish and promote thriving partnerships between U.S. IT channels & Korean IT client companies, and provide an effective gateway for Korean IT companies to successfully penetrate the United States marketplace.” KITA Q306 Seminar