Download

1 / 22

220 likes | 428 Views

Beberapa Pengertian Pasal 1 ayat (2) UU No. 13 Th 1985. PP No. 24 Tahun 2000. Dokumen Yg Dikenakan Bea Meterai Rp.3000,-. Dokumen yg Dikenakan Tarif Bea Meterai Rp. 6.000 ,-. Bukan Objek Bea Meterai Pasal 4 UU No. 13 Th 1985. Dokumen yg tidak terutang Bea Meterai.

E N D

Beberapa Pengertian Pasal 1 ayat (2) UU No. 13 Th 1985

PP No. 24 Tahun 2000 Dokumen Yg Dikenakan Bea Meterai Rp.3000,-

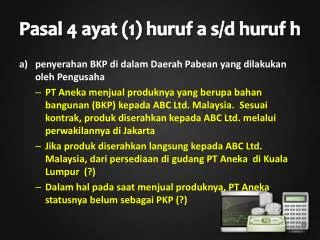

Bukan Objek Bea Meterai Pasal 4 UU No. 13 Th 1985

Dokumen yg tidak terutang Bea Meterai • Surat yg memuat jumlah uang yg mempunyai harga • nominal s/d Rp. 250.000,- b. Surat berharga seperti Wesel, Promes, Aksep yang mempunyai harga nominal s/d Rp. 250.000,-