Download

1 / 24

240 likes | 445 Views

Experiments in individual choice behavior. Devoted to test the predictions of the different theories of rational behavior Often, experiments that start as tests, move to become investigations of unpredicted regularities Often, these regularities are tested as robust phenomena

E N D

Experiments in individual choice behavior Devoted to test the predictions of the different theories of rational behavior Often, experiments that start as tests, move to become investigations of unpredicted regularities Often, these regularities are tested as robust phenomena Often these robust phenomena are described by a new theory of individual choice And often, this new theory is submitted to new experimental test to verify its generality.

Therefore, this literature give us a chance to look at the interaction between THEORY and EXPERIMENT

It also helps us to identify the systematic irrational biases in human behavior • and help us devise the instruments and the institutional rules to, perhaps, compensate for them: LIBERTARIAN PATERNALISM Thaler and Sunstein, AER May 2003

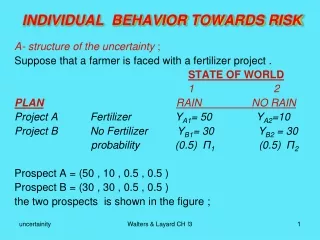

(systematic) anomalies • Invariance axiom. Individual preferences for two objects should not change depending on the “frame” in which objects are described. Question 1: A (72%) B (28%) Question 6: C (22%) D (78%) In (1) the implicit reference point is that the disease would kill 600 persons. In (6) the reference point is that nobody will die from the disease. Depending on the reference point what you choose is a gain or a loss. Could that make all the difference?

Check Questions (3) and (9): Question (3): A (20%) B (80%) Question (9): A (92%) B (8%) Individuals appear to display risk aversion for gains and risk preference for losses

Individuals show problems with compound presentations that can be decomposed in different ways Check Questions 2, 7 and 5. Question 2: A (78%) B (22%) Question 7: A (74%) B (26%) Question 5: H (42%) I (58%) Individuals ignore the first part of the game which is shared by 7A and 7B. It violates the principle (in vN-M expected utility) that the choice among alternatives is based solely on the probabilities of the end results. You change the way the probabilities are presented, and individuals change their decisions.

So individual decisions can be modified by changing the way probabilities are presented. Now we’ll see that they can also be modified by changing the way results are presented. Check Questions (3) and (11). Question (3): A (16%) B (84%) Question (11): A (69%) B (31%) It appears that what individuals care about when making a decision is not their final wealth, but the changes in their wealth.

Dominance axiom: If A is at least as preferred to B in all dimensions but strictly preferred to B in at least one dimension, then A is preferred to B. Check Questions (4) and (11) Question (4): E (0%) F (100%) Question (11a): A (84%) B (16%) Question (11b): C (13%) D (87%) Since the decision is simultaneous, it appears that individuals prefer A&D (73%) over B&C(3%). But, in fact, the combination A+D=E is clearly dominated by B+C=F in (4): A+D=E: .25(240) +.75(240) + .75(-1000) B+C=F: .25(1000) + .25(-750) + .75(-750)

Question 13: Betsy’s question. • Any ranking of probabilities shuld satisfy the conjunction rule: P(A)>=P(A&B). • But people evaluate the probability of events by the degree to which these events are representative of a relevant model. • Because the representativeness of an event can be increased by specificity, a compound target can be judged more probable than one of its components

Question 14: Taxicab court case • ¿Do people use the Bayes rule to judge conditional probabilities? • P(X/M) = P(M/X)P(X) divided by P(M) • The modal answer to the question is 80%. Confusion between P(identify white/white) = .8 with the P(white/identify white) = .41, because it reflects the small base rate P(white) = .15. [(.8)(.15)/(.8)(.15) + (.2)(.85)]

These answers gave rise to new concepts: • Status quo bias (prob de mort) • Willingness to pay/willingness to accept • Rationality is contextual (cards) • Valuations are contextual (bar) But, do we have an intuition of what being rational means? (auction)

The evidence demonstrates that human behavior deviates in systematic ways from the idealized behavior attributed to expected utility maximizers, in particular, and to “rational economic man” in general. • Therefore, either you: • Stick to your guns • Or, postulate a new theory to account for the observed behavior

What accounts then for economists’ reluctance to depart from the rational model, despite considerable contradictory evidence?

1. All theories are approximations. That’s what makes it difficult to “falsify” theories in economics. In Physics a single person levitating would be sufficient to falsify the law of universal gravitation. This is what makes us economists so envious of physicists. they can usually settle their problems by experiment: we seem to live with ours. Of course, our problems are more interesting. • 2. The question is what is the best approximation for the problem at hand?Of course, ad hoc approximations that can only be applied to a narrow event are of little interest. The theories should be intended to explain a class of events. Risk neutral economic man (max E(V)) was not dropped because of St Petersburg paradox, but because it could not explain the insurance market or the futures market. • 3. The best approximation is the theory that says everything is possible. it never fails. But does it help us?We need to introduce some restrictions in the theory for it to help us organize the data and make predictions. There is then a trade off. • 4. Rational models of individual choice seem to make good predictions in markets. • a. Markets need little rationality • b. Markets discipline people: people learn by operating in markets and preferences in market settings are not labile. (Myagkov & Plott AER Dec. 97).

Prospect theoryKahneman and Tversky, 1979 and Tversky and Kahneman, 1992 • Choices are compared not on the basis of vN-M expected utility, Si piU(xi). They are compared according to SipiV(xi-r), where p is a "weighting function" that scales the probabilities, which has the shape of an inverted S function, and where V(x-r) has a diminishing marginal sensitivity to the deviations with respect to a reference point r, such that it is concave for gains (risk aversion) and convex for losses (risk preference), and a higher slope for losses than for gains (loss aversion).

“What happens when the signs of the outcomes are reversed so that gains are replaced by losses?” (Kahneman and Tversky, 1979, p. 268), and answered, “… the preference between negative prospects is the mirror image of the preference between positive prospects. Thus the reflection of prospects around 0 reverses the preference order. We label this pattern the reflection effect.”

Man, the decision maker • Risk-neutral economics man. Never buys insurance, and would be willing to pay any finite amount to participate in St. Petersburg paradox, if only he could be convinced that the ressources exist to pay off any possible winnings.

Man, the decision maker • Expected-utility maximizing man. Buys insurance, ignores sunk costs and is immune to framing effects.

Man, the decision maker • Almost-rational man. In particular, Prospect-theory man. He has malleable reference points and probability perceptions, but still has preferences

Man, the decision maker • Psychological man (Tversky 1996). Does not have preferences. Has mental processes. Different frames and contexts, and different choice procedures elicit different processes. So he may sometimes exhibit preference reversals because choosing and pricing ellicit different mental procedures. • Psychologist’s question: What accounts for [economist’s] “reluctance to abandon the [rational model], despite considerable contrary evidence?”.

Man, the decision maker • Neurobiological man. Doesn’t even have a fixed collection of mental processes, in the sense of the psychological man. He has biological and chemical processes which influence his behavior. Different blood chemistry leads to different mental processes;e.g., depending on the level of lithium (or Valiu, or Prozac, or Cocaine...) in his blood, he makes different decisions on both routine matters and matters of great consequence –even life and death.An understanding of how chemistry interacts with mental processes has proved to be very useful, for instance in treating depression. • Neurobiologist’s question: What accounts for [psychologist’s] “reluctance to abandon the [psychological] model, despite considerable contrary evidence?”