Download

1 / 27

280 likes | 419 Views

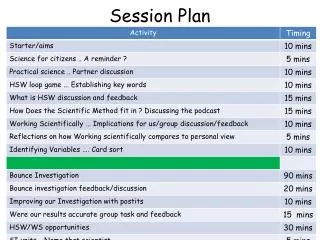

Session Plan. Chapter Twelve: REITs as investment alternative QQD of REITs REIT Valuation Techniques The Send-Off. Origins of REITs. Massachusetts Trust (19 th Century until 1935) Filled void for corporations owning RE No federal tax, & no distributions tax for shareholders!!

E N D

Session Plan • Chapter Twelve: • REITs as investment alternative • QQD of REITs • REIT Valuation Techniques • The Send-Off

Origins of REITs • Massachusetts Trust (19th Century until 1935) • Filled void for corporations owning RE • No federal tax, & no distributions tax for shareholders!! • Investment Company Act of 1940 • Closed end mutual funds lobbied for equal treatment until tax law was amended in 1960 • External management structure was required until 1986

Real Estate Investment Trusts (REITs) • First established in US in 1960 • 1971 Australia, 1985 Turkey, Canada 1993, Singapore 1999, Japan 2000, Hong Kong & France 2003, Germany in 2007 • US Minimum Requirements • 100 shareholders • 75% of value of REIT assets in RE, cash, or gov’t securities • 95% of gross income from dividends, interest, rents, or gains from sale of REIT assets • Shareholder distributions at least 90% of REIT taxable income annually • Additional European Requirements • Leverage is limited (50% in Germany, France, Spain; 20% for most Austrian REITs, a coverage ratio of 1.25x EBIT/Int in UK) • Limits for size of any one property (15% in G-REIT, 40% in UK) • EU REIT Strategies: Core/nuclear (low risk), Core-Plus/Value Added (medium risk) and Opportunity (high risk)

REIT Organizational Structures • UPREIT: Umbrella Partnership REIT • Established in 1992 to allow existing RE operating companies to bring property already owned under umbrella of REIT w/o capital gains tax • REIT owns controlling interest in limited partnership that owns the real estate • Owners of limited partnership can convert operating units into REIT shares, vote, & receive dividends

REIT Organizational Structures • Down REIT: • Formed after REIT goes public • Can own numerous partnerships at the same time • Down REIT owns property directly in REIT, but holds some properties in partnership with others • No tax liability until partnership units are converted into stock or sold

REIT Incentive Issues • UPREIT: • Management could be reluctant to sell if they own operating units rather than REIT shares • Subject to tax when sold • Down REIT: • If management does not own operating units, could become “trigger happy” with sales given the lack of tax consequences from sale

REIT Taxation • Shareholders pay taxes on dividends received via form 1099 • 721 Exchange: Like Kind Exchange for REITs • Limited Partners of Up and Down REITs can exchange partnership units for interests in other RE via like kind exchange • Must be investment grade property • Investors receive operating units rather than property • Up and Down REITs have advantages for tax sensitive sellers

Types of REITS • Mortgage REITs • Heyday in 1970s • Equity REITs • Most common form today • Hybrid REITs • Invest in both mortgages and equity • Mutual Fund REITs • Common for personal investors

Mutual Fund REITs • First mutual fund in Netherlands in 1774 • Modern mutual funds began in US in 1924 • Was truly “mutual” as it was organized, operated, & managed by its own trustees • Alpha Fund: shareholders own funds which own management company • Omega Fund: Mgmt company shareholders own mgmt company which controls mutual fund owned by mutual fund shareholders • Mgmt company shareholder interests are introduced • Higher costs typically given competing goals of shareholder wealth creation & profit for external mgmt company

REIT Historical Performance As you can see, mortgage REITs are historically more volatile than equity REITs

“Portfolio Mix” Strategy • Investors can review annual reports of REIT mutual funds to obtain information for how they allocate their investment dollars. It looks like REIT 1 has more confidence in the office market but much less in retail than does REIT 2

“Quantity” Strategy • This strategy involves maximizing the gross potential income by keeping overall portfolio vacancy rates as low as possible.

“Quality” Strategy • Another portfolio diversification strategy is to concentrate on properties that have high quality, nationally known companies as tenants. See any problem companies here?

“Durability” Strategy • Let’s see how REIT 1 looks in terms of the durability of the lease income. For Retail: low percentage of portfolio but long leases.

“Geographic Dispersion” Strategy • REITs (or wealthy investors) have the ability to reduce local market risk via diversification. • Below is how REIT 1 is diversified in this way...

“Geographic Dispersion” Strategy Continued • Another method of viewing this type of portfolio risk smoothing is by Metropolitan Statistical Area (MSA):

REIT & The QQD Framework • Quantity Strategy • Strong dividends, maximize GPI, growth orientation purchased at discount • Focus strategy: less diversified • Diversified: higher expenses • Quality Strategy • Nationally known tenants, NNN REITs, Blue Chip REITs • Durability Strategy • Tenant rollover risk, length of leases, geographic dispersion

REIT & The QQD Framework • Lease Rollover Risk • Attempt to diversify via the duration of the income stream on associated properties. • Also based on the lack of a high concentration on any particular tenant for the total revenue • Business Risk • Attempt to diversify via the region or type of property in an effort to reduce concentration on one area or property type

REIT Valuation Techniques • Gordon Dividend Growth Model • Funds from Operations (FFO) Multiple • Net Asset Value (NAV)

Gordon Dividend Growth Model • Utilizes future dividend per share expected next year to calculate stock price as the present value of expected future dividends • Constant dividend growth is assumed • Begin with DCF based on projected revenue and expenses to estimate FFO for an assumed holding period • Add in reversion to obtain PV of firm • Divide by # of outstanding shares to obtain D1 V = D1 (k-g) $50.00 = $3.00 (0.10-0.04)

FFO Multiple • Similar to the Price to Earnings Ratio • FFO: Net income (GAAP) excluding gains or losses from sales of property or debt restructuring adding back RE depreciation • Value = FFO/share * FFO Multiple • Multiple: Historical multiple for REIT or peer group • Only as good as the comparables!!

Net Asset Value (NAV) • Value = Aggregate Stabilized NOI Blended Cap Rate • Blended cap rate is difficult for diversified assets • Rather: Find value of specific properties and divide by property specific cap rates to obtain value of portfolio • Once find value, subtract out debt to obtain NAV • Shares quoted in terms of Net Asset Value (NAV) • Holding Period Return= NAVnow –NAVprior + Divholding period NAVprior

REIT Valuation Issues • Different classifications of recurring expenses for FFO • Tenant Improvements, Leasing Commissions • If categorize as expense, subtract from FFO • If categorize as capital improvement, amortized on balance sheet • Adjusted FFO (AFFO) • Adjusts FFO for expenses, while capitalized, which do not enhance property value • Eliminates straight lining of rents • FASB 13: Free rent or increases must be equalized (straight-lined) over term of lease

REIT Internationalization • International RE Investment is becoming more of an area of study • Historically International RE Investment focused on Blue Chip properties in well known cities • RE Investment becoming more frequent in Emerging Markets • RE Investment in Developing Countries typically centers around Tier I cities • REITs have been embraced by Islamic Finance given the verifiable nature of the assets included in the investment pool • The initial requirement for external management still exists in many countries…

The End? • “One repays a teacher badly if one always remains a pupil…” • Thus Spoke Zarathustra, On the Gift Giving Virtue, pg. 78 • Go forth and invest in Real Estate!! Friedrich Nietzsche